Forecast

Household consumption could be hard hit in the energy crisis

The alternative scenario in the Bank of Finland’s forecast for the Finnish economy examines risks surrounding the Bank’s December 2022 baseline forecast which, should they materialise, could lead economic growth to be weaker than projected. The scenario estimates the possible impacts on the Finnish economy if Russia’s war in Ukraine drags on and if the availability of energy weakens further and economic uncertainty increases. Compared to the baseline forecast, a further deepening of the crisis would prolong the economic recession in Finland and maintain price pressures in 2023 at a higher level than projected. With higher inflation and a higher increase in interest rates than in the baseline forecast, private consumption would be notably weakened. The high level of household indebtedness may deepen the recession, particularly if the financial margin of indebted households is small.

Ukraine war and energy crisis could prolong the recession

The alternative scenario describes a situation where growth is weaker than in the baseline forecast.1 It assumes that the war in Ukraine drags on and maintains uncertainty in the economy. In addition to the continuation of the war, geopolitical tensions remain high and disruptions in the international value chain continue. The assumption is made that banks’ funding costs will grow as a result of the heightened uncertainty and weaker economic situation (Table 1).

The scenario assumes that there will be a shortfall in energy availability in the euro area as gas imports from Russia dry up completely. This will lead not only to high energy prices but also to cuts in industrial production in the euro area this winter and next winter, as the scenario assumes that winters will be cold. The weakness of the euro area economy, caused by the production problems, will erode Finland’s export demand. It is also assumed in the scenario that due to the cold weather, there will be electricity shortages this winter in Finland, too, which will cause disruptions in production. The scenario assumes that Russia’s extra-EU oil exports will also decrease in the short term. The world market price of crude oil will rise to a clearly higher level than in the baseline forecast (Table 1).

| 2022f | 2023f | 2024f | 2025f | ||

|---|---|---|---|---|---|

| Export markets (annual growth, %) | Baseline forecast | 5.6 | 1.7 | 3.1 | 3.3 |

| Alternative scenario | 5.6 | -0.3 | 0.7 | 4.0 | |

| Competitors’ export prices (annual growth, %) | Baseline forecast | 16.9 | 3.7 | 2.1 | 2.0 |

| Alternative scenario | 16.9 | 7.5 | 1.2 | 0.7 | |

| Crude oil (USD/barrel) | Baseline forecast | 104.6 | 86.4 | 79.7 | 76.0 |

| Alternative scenario | 104.6 | 122.5 | 92.0 | 76.8 | |

| Interest rate on corporate loans (%) | Baseline forecast | 1.6 | 3.4 | 3.9 | 4.0 |

| Alternative scenario | 1.6 | 3.7 | 4.6 | 4.7 | |

| Baseline forecast: Bank of Finland December 2022 forecast trajectory. | |||||

| f = forecast. | |||||

| Sources: ECB and Bank of Finland. | |||||

| 2022f | 2023f | 2024f | 2025f | ||

|---|---|---|---|---|---|

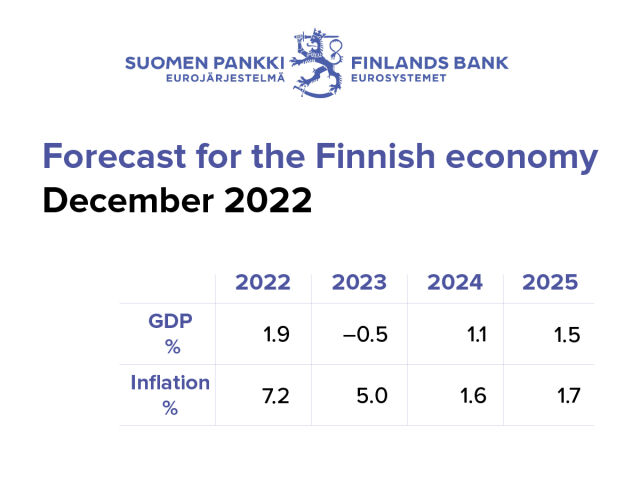

| Gross domestic product, annual growth (%) | Baseline forecast | 1.9 | -0.5 | 1.1 | 1.5 |

| Scenario, phase 1 (Aino 2.0) | 1.9 | -1.6 | -0.8 | 1.9 | |

| Scenario, phase 2 (Aino 3.0) | 1.9 | -3.6 | -1.5 | 4.1 | |

| Private consumption, annual growth (%) | Baseline forecast | 2.4 | -1.3 | 0.4 | 1.1 |

| Scenario, phase 1 (Aino 2.0) | 2.4 | -3.2 | -1.6 | 3.3 | |

| Scenario, phase 2 (Aino 3.0) | 2.4 | -4.2 | -2.0 | 6.6 | |

| Unemployment rate (%) | Baseline forecast | 73.7 | 73.6 | 73.8 | 74.1 |

| Scenario, phase 1 (Aino 2.0) | 73.7 | 72.7 | 70.8 | 71.4 | |

| Scenario, phase 2 (Aino 3.0) | 73.7 | 70.5 | 64.6 | 66.1 | |

| Inflation* (%) | Baseline forecast | 7.2 | 5.0 | 1.6 | 1.7 |

| Scenario, phase 1 (Aino 2.0) | 7.2 | 6.0 | 1.6 | 1.9 | |

| Scenario, phase 2 (Aino 3.0) | 7.2 | 9.4 | 1.5 | 1.6 | |

| Baseline forecast: Bank of Finland December 2022 forecast trajectory. | |||||

| * = Harmonised Index of Consumer Prices. | |||||

| f = forecast. | |||||

| Sources: Statistics Finland and Bank of Finland. | |||||

The alternative scenario is performed in two stages. In the first stage, we use the Bank of Finland’s Aino 2.0 model – also used for preparing the baseline forecast – to estimate the impact of the weaker scenario, described above, on economic growth, private consumption, the employment rate and inflation (phase 1).

In the second stage of the alternative scenario, the Aino 3.0 model is used to estimate the impacts of lower-than-expected economic growth on the situation of households in particular (phase 2). This model calculation enables assessment of the impacts of indebtedness on the ability of households to adjust to the decline in purchasing power and to rising interest rates prompted by high inflation, and the magnitude of the possible macroeconomic second-round effects. The Aino 2.0 model cannot be used for estimating these impacts, due to the structure of the model.2

In the first phase of the alternative scenario, the slowdown in economic growth is larger and more prolonged than in the baseline forecast (Chart 1, Table 2), and GDP in 2025 is still significantly lower than in the baseline scenario. Uncertainty is exacerbated by the continuation of the war and the deepening of the energy crisis, and this will weaken private consumption and investment compared to the baseline forecast. Economic growth will slow in 2023, and this will also be due to muted export demand, rising interest rates and higher prices.

Employment will weaken in the wake of the economic situation, and the labour market in 2025 will still be less strong than in the baseline forecast. The employment rate will, however, remain at over 70% in the first phase of the scenario, and will reach 71.4% in 2025 (Table 2).

As a result of the higher energy prices and production problems, price pressures will ease in the alternative scenario at a slower pace than in the baseline forecast, and inflation will be higher particularly in 2023 (Table 2). Towards the end of the forecast period, the decline in energy prices and demand will slow the rise in prices.

chart 1.GDP will suffer long-term from prolongation of the Ukraine war and escalation of the energy crisis

| 2022f | 2023f | 2024f | 2025f | ||

|---|---|---|---|---|---|

| Export markets (annual growth, %) | Baseline forecast | 5.6 | 1.7 | 3.1 | 3.3 |

| Alternative scenario | 5.6 | -0.3 | 0.7 | 4.0 | |

| Competitors’ export prices (annual growth, %) | Baseline forecast | 16.9 | 3.7 | 2.1 | 2.0 |

| Alternative scenario | 16.9 | 7.5 | 1.2 | 0.7 | |

| Crude oil (USD/barrel) | Baseline forecast | 104.6 | 86.4 | 79.7 | 76.0 |

| Alternative scenario | 104.6 | 122.5 | 92.0 | 76.8 | |

| Interest rate on corporate loans (%) | Baseline forecast | 1.6 | 3.4 | 3.9 | 4.0 |

| Alternative scenario | 1.6 | 3.7 | 4.6 | 4.7 | |

| Baseline forecast: Bank of Finland December 2022 forecast trajectory. | |||||

| f = forecast. | |||||

| Sources: ECB and Bank of Finland. | |||||

| 2022f | 2023f | 2024f | 2025f | ||

|---|---|---|---|---|---|

| Gross domestic product, annual growth (%) | Baseline forecast | 1.9 | -0.5 | 1.1 | 1.5 |

| Scenario, phase 1 (Aino 2.0) | 1.9 | -1.6 | -0.8 | 1.9 | |

| Scenario, phase 2 (Aino 3.0) | 1.9 | -3.6 | -1.5 | 4.1 | |

| Private consumption, annual growth (%) | Baseline forecast | 2.4 | -1.3 | 0.4 | 1.1 |

| Scenario, phase 1 (Aino 2.0) | 2.4 | -3.2 | -1.6 | 3.3 | |

| Scenario, phase 2 (Aino 3.0) | 2.4 | -4.2 | -2.0 | 6.6 | |

| Unemployment rate (%) | Baseline forecast | 73.7 | 73.6 | 73.8 | 74.1 |

| Scenario, phase 1 (Aino 2.0) | 73.7 | 72.7 | 70.8 | 71.4 | |

| Scenario, phase 2 (Aino 3.0) | 73.7 | 70.5 | 64.6 | 66.1 | |

| Inflation* (%) | Baseline forecast | 7.2 | 5.0 | 1.6 | 1.7 |

| Scenario, phase 1 (Aino 2.0) | 7.2 | 6.0 | 1.6 | 1.9 | |

| Scenario, phase 2 (Aino 3.0) | 7.2 | 9.4 | 1.5 | 1.6 | |

| Baseline forecast: Bank of Finland December 2022 forecast trajectory. | |||||

| * = Harmonised Index of Consumer Prices. | |||||

| f = forecast. | |||||

| Sources: Statistics Finland and Bank of Finland. | |||||

Household sector indebtedness may deepen the recession

In the first phase scenario calculation presented above, one of the underlying assumptions is that households are able to smooth their consumption over time by saving or by tapping into their savings if there is a change in their disposable income. They can also adjust their borrowing to finance their consumption. In reality, households may, however, have credit or liquidity constraints that prevent them from taking out a loan if their income suddenly decreases.3

The higher inflation, larger contraction in purchasing power and stronger rise in interest rates in the first phase of the alternative scenario will weaken the position of indebted, credit-constrained and liquidity-constrained households, in particular. These households will not necessarily be able to compensate for the rising cost of living by tapping into their savings or by borrowing as their real income shrinks and purchasing power diminishes as a result of the recession and high inflation.

Under the scenario assumptions, risk premia on loans will increase and financing conditions tighten because of the economic uncertainty. As a result, interest rates on housing loans, too, will rise, which will increase the loan-servicing costs of mortgage-indebted households and decrease the amount of income available for other consumption. At the same time, an economic recession and rise in interest rates will typically lower housing prices and thus the loan collateral values, which will further weaken households’ ability to borrow.

If, in a situation like this, a large amount of households have to decrease their consumption substantially due to liquidity and credit constraints, it could have significant macroeconomic second-round effects. The recession will be deeper and the recovery slower.

Next, we examine how the first phase calculations presented above change when we take into consideration that some households are indebted and will be subject to credit constraints. In the second phase of the scenario, we use the same assumptions as above about the greater-than-expected deterioration in Finland’s external environment (Table 1). In the model, 12% of all households are mortgage-indebted and their ability to borrow depends on the collateral value of the housing.4 Due to the credit constraints, they will have to cut their consumption drastically if their income decreases.

In this phase two scenario, private consumption will shrink by 2.9 percentage points more in 2023 and 2.4 percentage points more in 2024 than in the baseline forecast (Table 2, Chart 2). Compared to the first phase of the scenario, private consumption will shrink 1 percentage point more in 2023 and 0.4 percentage points more in 2024. This difference indicates the macroeconomic second-round effects resulting from household indebtedness and credit constraints. Following the rise in interest rates, households’ nominal housing loan-servicing costs will, in 2023, be some 7% higher than in the baseline forecast. In 2024, the growth in loan-servicing costs will turn onto a downward trend. They will, however, be nearly 9% larger towards the end of the forecast period than they were still in 2022, as interest rates will remain at a higher level.

chart 2.Households' credit constraints reinforce the contraction in private consumption

The demand for new housing loans will decrease as real incomes shrink and interest rates rise. At the same time, high inflation will erode the real value of the existing loan stock. The real stock of housing loans, adjusted for the rise in prices, will shrink in the immediate years ahead, and in 2025 will be 1.6% smaller than in the baseline forecast. The household sector’s housing debt relative to income will nevertheless increase during the forecast period compared to the situation in 2022, as disposable income will shrink more than the stock of housing loans. High inflation will not, therefore, ease the situation of mortgage-indebted households.

The strong decrease in households’ consumption demand will also weaken growth in GDP and in labour demand and wages. This will exacerbate the recession further (Chart 1). As a result of a deep recession, the employment rate will also decrease substantially. Economic growth in this scenario will, in 2023, be more than 3 percentage points lower than in the baseline forecast (Table 2). Growth in 2024 will be 2.6 percentage points lower than in the baseline forecast. Compared to the first phase of the alternative scenario, the economy will shrink 2 percentages more in 2023 and 0.7 percentage points more in 2024. This difference indicates again the amplifying effects of households’ credit constraints.

In 2025, the economy will start to recover as Finland’s external demand strengthens, inflation slows significantly and the rise in interest rates subsides. Private consumption and at the same time the entire economy will recover rapidly as the situation of indebted households, in particular, eases and their income improves. GDP growth will be 2.6 percentage points higher than in the baseline forecast.

The second phase of the alternative scenario outlined here describes a severe shock to the economy and a situation where indebted households face binding credit constraints. The strong contraction in private consumption demand produced by the model is due especially to indebted households having to adjust their consumption very markedly as a result of credit constraints, when their disposable income changes.

Based on data for Finland and earlier analysis, the financial margin of indebted households is, however, typically reasonable, and in reality a high proportion of households that are heavily indebted relative to income are able to dampen the impact of financial shocks on their own situation with the help of various buffers.5 The results of the second phase model scenario can thus be considered to represent the maximum extent of the macroeconomic second-round effects that could be caused by household sector indebtedness, whereas in the first phase scenario, these effects are fully disregarded.

Notes

-

The alternative scenario does not necessarily reflect the views of the European System of Central Banks. The scenario utilises the European Central Bank’s December 2022 downside scenario assumptions regarding developments in the external economic environment. ↑

-

In Aino 3.0, the household sector is modelled in more detail than in the Aino 2.0 model used in the production of the baseline forecast. By contrast, in the Aino 3.0 model, a proportion of households are assumed to be mortgage-indebted and their borrowing is constrained by the binding maximum loan-to-value ratio. The model can therefore be used for estimating the macroeconomic effects of household borrowing. ↑

-

Credit constraint refers to a situation in which a household is not granted the loan it has applied for, or is granted a smaller loan. Liquidity constraint, in turn, refers to a situation in which a household has only a small amount of liquid assets – for example cash or bank deposits in transaction accounts – that could provide a financial buffer for a rainy day. ↑

-

The proportion of credit-constrained households was estimated using the household-level data from Statistics Finland’s 2019 Household Finance and Consumption Survey and by applying the definition described by Kaplan et al. (2014). See Kaplan, G., Violante, G. L. and Weidner, J., 'The Wealthy Hand-to-Mouth', NBER Working Paper 20073, 4/2014. ↑

-

The financial situation and margin of heavily indebted households are analysed in more detail using data from the 2019 Household Finance and Consumption Survey in Mäki-Fränti, P. (2021), 'The financial situation of the highly indebted varies in Finland', Bank of Finland Bulletin, 25 November 2021 (in Finnish only). The analysis finds that large debts are held particularly by high-income and wealthy households that are well able to meet the loan-servicing costs. It also found that the financial margin of indebted households is good, on average, despite the high level of debt. ↑