Forecast

Finnish economy set to slide into recession

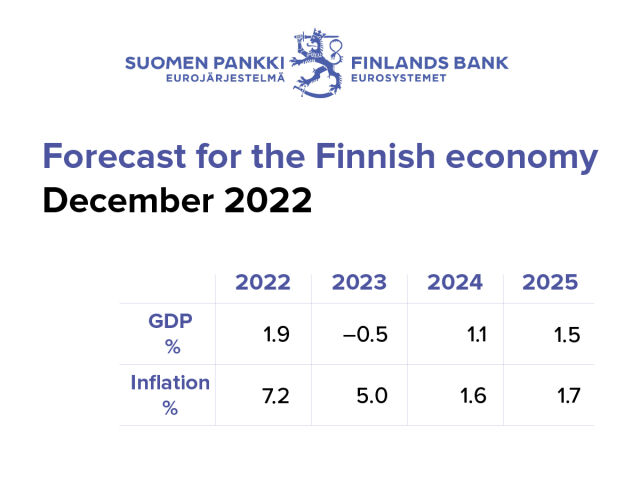

Growth in the Finnish economy for the full year 2022 will amount to 1.9%, following strong activity in the early part of the year. The high level of inflation has, however, eroded households’ purchasing power, and consumer confidence has slumped to a very low level. In 2023, the economy will slide into a mild recession and real GDP will contract by 0.5% in response to the energy crisis exacerbated by Russia’s war in Ukraine and the surge in the cost of living. The recession will, however, be fairly short-lived. Growth will rebound to 1.1% in 2024 as the headwinds to the economy subside. In 2025, Finnish real GDP will grow by 1.5%.

Russia’s war in Ukraine, the energy crisis, the surge in inflation and rise in interest rates as a consequence are weakening the global economy, with the war and the energy crisis weighing on growth in Europe, in particular. Finnish export growth is hampered by the marked decline in economic growth in Finland’s major export markets.

The stalling of Finland’s economic growth and the decline in companies’ employment expectations will also reverse the favourable situation on the labour market. Employment growth will slow, causing a temporary rise in the unemployment rate. At the same time, the labour shortages will ease somewhat in cyclically sensitive industries. Employment will nonetheless remain good, given the brief duration of the recession and the structural nature of the labour shortage in many sectors.

Inflation has increased further in 2022. Higher energy and raw material prices and protracted supply chain disruptions have led to a widespread rise in consumer prices. The rise in the inflation rate will be slowed by a decline in the prices of crude oil and raw materials, but high electricity costs will keep price pressures high especially during the coming winter months. Some of the price pressures will spill over to food, consumer goods and services prices after a time lag. Inflation will slow to 5% in 2023, following the easing of supply chain bottlenecks, the feed-through of monetary policy tightening to the economy and the weakening of domestic demand.

Private consumption will decrease in 2023 in response to the weak development of purchasing power. Nominal earnings growth has clearly fallen below the rate of inflation, and there is consequently an exceptional decline in real earnings this year. Due to the high level of inflation, the European Central Bank has raised its policy rates, which is depressing private consumption. However, some households are able to resort to savings accumulated during the COVID-19 pandemic. Disposable nominal income will improve because employment remains stable and earnings growth is positive. Purchasing power – and by extension private consumption – will gradually start to revive from next year onwards, as inflation slows down.

Deteriorating cyclical conditions, uncertainty about the economic outlook and higher financing costs will also start to show in private investment, which will contract in 2023. Housing construction will decline markedly. Households and residential property investors have little appetite to borrow. The launch of construction projects will also be slowed by the rapid rise in construction costs.

The public finances will remain in deficit. While the general government deficit-to-GDP ratio will still improve in 2022, from 2023 onwards public spending will grow faster than revenues, and the ratio will start to rise again. The public debt-to-GDP ratio will decline slightly in both 2022 and 2023 as, due to the general increase in prices, nominal GDP growth will be faster than growth in public spending. The debt ratio will begin rising again considerably from 2024 onwards and will reach almost 75% by the end of 2025.

The risks surrounding the forecast are on the downside. The outlook in Finland’s export markets continues to be uncertain due to the war in Ukraine. In Finland, if the period of high inflation is more protracted than foreseen, this may cut consumers' purchasing power and private consumption by more – and for longer – than projected, driving the economy into a deeper recession than expected.

| Percentage change on the previous year | ||||||

|---|---|---|---|---|---|---|

| 2020 | 2021 | 2022f | 2023f | 2024f | 2025f | |

| GDP | -2.2 | 3.0 | 1.9 | -0.5 | 1.1 | 1.5 |

| Private consumption | -4.0 | 3.7 | 2.4 | -1.3 | 0.4 | 1.1 |

| Public consumption | 0.3 | 2.9 | 2.7 | 0.7 | 0.6 | 0.5 |

| Fixed investment | -0.9 | 1.5 | 5.1 | -1.2 | 0.4 | 4.2 |

| Private fixed investment | -3.2 | 4.7 | 4.7 | -2.0 | -0.1 | 1.7 |

| Public fixed investment | 9.5 | -11.5 | 7.2 | 2.4 | 2.5 | 14.7 |

| Exports | -7.8 | 5.4 | 1.7 | 1.8 | 2.8 | 3.1 |

| Imports | -6.2 | 6.0 | 8.6 | -1.0 | 1.3 | 3.8 |

| Effect of demand components on growth | ||||||

| Domestic demand | -2.3 | 2.9 | 3.1 | -0.8 | 0.4 | 1.6 |

| Net exports | -0.7 | -0.2 | -2.7 | 1.3 | 0.7 | -0.3 |

| Changes in inventories and statistical error |

0.7 | 0.3 | 1.5 | -1.0 | 0.0 | 0.1 |

| Savings rate, households, % | 4.7 | 2.0 | -1.2 | 0.3 | 0.4 | 0.3 |

| Current account, % of GDP | 0.7 | 0.6 | -3.7 | -0.8 | 0.4 | -0.2 |

| 2020 | 2021 | 2022f | 2023f | 2024f | 2025f | |

|---|---|---|---|---|---|---|

| Labour market | ||||||

| Number of hours worked | -2.5 | 3.2 | 1.0 | -0.5 | 0.7 | 0.6 |

| Number of employed | -2.0 | 2.6 | 2.6 | -0.2 | 0.3 | 0.3 |

| Unemployment rate, % | 7.8 | 7.6 | 6.9 | 7.4 | 7.2 | 7.1 |

| Unit labour costs | 0.7 | 2.5 | 4.4 | 5.8 | 2.9 | 2.0 |

| Labour compensation per employee | 0.4 | 2.9 | 3.7 | 5.5 | 3.8 | 3.2 |

| Productivity | -0.2 | 0.4 | -0.7 | -0.3 | 0.9 | 1.1 |

| GDP, price index | 1.5 | 2.5 | 5.8 | 4.8 | 2.4 | 1.8 |

| Private consumption, price index | 0.5 | 1.7 | 5.5 | 5.1 | 1.8 | 1.9 |

| Harmonised index of consumer prices | 0.4 | 2.1 | 7.2 | 5.0 | 1.6 | 1.7 |

| Excl. Energy | 0.8 | 1.3 | 4.7 | 4.4 | 2.3 | 2.1 |

| Energy | -5.0 | 9.7 | 31.6 | 9.6 | -3.9 | -2.2 |

| General government, % of GDP | ||||||

| General government balance | -5.5 | -2.7 | -0.9 | -1.8 | -2.0 | -2.6 |

| General government gross debt (EDP) | 74.8 | 72.4 | 72.2 | 71.9 | 73.2 | 74.9 |

| f = forecast. | ||||||

| Sources: Bank of Finland and Statistics Finland. |

Operating environment: Assumptions and financial markets

Russia’s war in Ukraine, the energy crisis, the surge in inflation and rising interest rates are weakening the global economy. Growth in the global economy will continue, however, and even strengthen in the longer term. There is still great uncertainty about the future outlook, particularly as the war in Europe and the uncertain path of the energy crisis are clouding the economic outlook. This economic forecast by the Bank of Finland is based on data available on 30 November 2022.

Global economic growth will slacken

The global economy is losing momentum as the end of 2022 approaches, with growth abating especially in the advanced economies in response to heightened uncertainty, the energy crisis, the surge in inflation and rising market rates. Russia’s war in Ukraine is weighing on growth in the European economy, in particular.

World trade growth will slow markedly in 2023 (Table 2). At the same time, however, the supply chain disruptions in world trade will ease further, partly due to the decline in global demand. After the weak performance in the early part of the year, global trade is expected to pick up towards the end of 2023, and demand in Finland’s export markets is likely to rebound in 2024 and 2025 (Chart 1, Table 2). Although the global economy will strengthen as 2024 nears, considerable downside risks remain.

chart 1.Demand for Finland's exports will increase after subdued start to 2023

Higher energy prices will push up production and import prices worldwide, driving up inflation. In addition, the depreciation of the euro against the US dollar will raise the euro-denominated prices of imported goods. Energy prices are assumed to gradually fall, in line with market expectations (Table 2), while the prices of other raw materials will remain close to their current levels. The forecast is based on the assumption that oil imports from Russia will end but gas imports continue, and some of the lost Russian gas will be replaced from other sources.1

Economic growth will decline substantially in Finland’s main export markets, which will dampen the level of growth in Finnish exports and GDP. The growth outlook for both the euro area and the United States is weaker than earlier projected, while the Chinese economy is strained by problems in the real-estate markets and the continuation of the COVID-19 pandemic. The demand for Finland’s exports is also adversely affected by the decline in trade with Russia.

Euro area growth will fall back due to the energy crisis exacerbated by the war, and the euro area economy will slide into a mild recession around the turn of the year.2 Growth is being undermined not only by the energy crisis and high inflation but also by, for example, heightened uncertainty, tighter financing conditions and the cooling of the global economy. Furthermore, the favourable conditions for services sectors as a result of the fading concerns about the pandemic are starting to subside. In the longer term, economic growth will pick up as uncertainty dissipates, real wages improve and supply chain disruptions are eliminated.

Euro area inflation has broadened out and is projected to gradually moderate from 2023 onwards, coming down to a little over 2% in 2025. Inflation will slow in response to a fall in energy prices consistent with market expectations, the normalisation of ECB monetary policy and the easing of global bottlenecks. Euro area underlying inflation (excl. energy and food prices) is also projected to slow, but strong wage growth, among other things, will keep it a little above 2% still in 2025.

Rising interest rates are tightening financing conditions

In December 2022, the Governing Council of the European Central Bank (ECB) decided to raise interest rates by 50 basis points.3 The interest rate on the main refinancing operations will now be 2.50%, the rate on the marginal lending facility 2.75% and the rate on the deposit facility 2.00%. Interest rates will still have to rise significantly to reach levels that are sufficiently restrictive to ensure a timely return of inflation to the 2% medium-term target. The ECB Governing Council also decided that from March 2023 onwards the principal payments from maturing securities under the asset purchase programme (APP) will no longer be reinvested in full, i.e. the portfolio will be allowed to decline gradually.

Interest rates have risen rapidly in the second half of 2022. Following the increase in market rates, average interest rates on new mortgages and new corporate loans have also begun to rise sharply in Finland (Chart 2). Financial markets expect euro area short-term interest rates to climb to around 3% in 2023 (Table 2), and to fall slightly by 2024 as inflationary pressures moderate.

The findings of the euro area bank lending survey show that the credit standards and terms and conditions of respondent banks have not been widely tightened in Finland in 2022. The Business Tendency Survey released by the Confederation of Finnish Industries in October found that while the financial difficulties of companies have slightly increased in many industries, it is the insufficient level of demand, the shortage of skilled labour and material and capacity constraints that continue to pose a more significant obstacle to production or sales.

chart 2.Average interest rates on new loans are rising steeply

| Volume change year-on-year, % | |||||

|---|---|---|---|---|---|

| 2021 | 2022f | 2023f | 2024f | 2025f | |

| Euro area GDP | 5.2 | 3.4 | 0.5 | 1.9 | 1.8 |

| World GDP (excl. euro area) | 6.4 | 3.3 | 2.6 | 3.1 | 3.3 |

| World trade (excl. euro area)* | 12.6 | 5.6 | 1.9 | 3.3 | 3.3 |

| 2021 | 2022f | 2023f | 2024f | 2025f | |

| Finland’s export markets, % change** | 10.4 | 5.6 | 1.7 | 3.1 | 3.3 |

| Oil price, USD/barrel | 71.1 | 104.6 | 86.4 | 79.7 | 76.0 |

| Export prices of Finland’s competitors, EUR, % change | 9.9 | 16.9 | 2.9 | 0.8 | 0.9 |

| 3-month Euribor, % | -0.5 | 0.4 | 2.9 | 2.7 | 2.5 |

| Finland’s nominal effective exchange rate*** | 109.4 | 106.5 | 106.8 | 106.8 | 106.8 |

| USD value of one euro | 1.18 | 1.05 | 1.03 | 1.03 | 1.03 |

| * Calculated as the weighted average of imports. | |||||

| ** The growth in Finland’s export markets is the average of the import growth of the countries Finland exports to, weighted by their respective shares of Finland’s exports. | |||||

| *** Broad nominal effective exchange rate, 2015 = 100. The index rises as the exchange rate appreciates. | |||||

| f = forecast. | |||||

| Sources: Bank of Finland and Statistics Finland. |

Demand and the public finances

The Finnish economy is set to slide into recession in 2023 as a consequence of the energy crisis, which is exacerbated by the war in Ukraine, and the fast rise in living costs (Chart 3). A loss of momentum in economic growth is widespread across the economy. High inflation has eroded purchasing power, and consumer confidence has slumped to a very low level. Uncertainty is impacting private consumption and investment demand. Growth will nevertheless be underpinned by net exports, despite the weak trend in Finland’s export markets. The recession will be short-lived, however, and the economy will slowly start to grow again in 2024 as the energy crisis eases and uncertainty recedes. Finland’s public finances will show a deficit throughout the entire forecast period.

chart 3.The Finnish economy is set to slide into a mild recession

Weaker purchasing power will slow consumption growth

The improved employment rate and earnings growth have meant that household incomes have increased in 2022, but high inflation is eroding the growth in purchasing power (Chart 4). At the same time, consumer confidence has plummeted to a very low level. Private consumption is nevertheless being underpinned by services demand, which has picked up following the fading of pandemic concerns and lifting of restrictions.

chart 4.Households will have to resort temporarily to their savings

Earnings levels will increase faster in 2023 than this year, but inflation will continue to consume most of the rise in household income.

Purchasing power will no longer be boosted by employment levels, as the slowdown in economic growth will bring the favourable employment trend to a halt. Private consumption will remain under pressure from both weak income growth and general uncertainty in the economy until the economic outlook starts to brighten towards the end of the forecast period.

Owing to the weak trend in purchasing power, private consumption will begin to decline in 2023 (Chart 4). High inflation has resulted in the European Central Bank raising interest rates, which will slow down the private consumption even more. Many households will see more of their income being swallowed up by mortgage costs.4

The household savings rate began to increase during the pandemic, and more than EUR 6 billion was accumulated in additional savings in 2020 and 2021. The weak trend in purchasing power, however, has meant that in 2022 households have had to resort to their savings, and so the savings rate is negative. At the same time, inflation and a fall in asset values have eaten away at household wealth. Households nevertheless still have financial assets to serve as buffers against recession and inflation. From 2023, the savings rate will again be slightly positive, with nominal disposable income rising as a result of stability in the employment rate and a healthy trend in earnings.

In 2024 and 2025 the inflation rate will be considerably lower than now. As inflation slows, consumers’ purchasing power will start to improve and confidence will be restored. Private consumption will once again start to rise in the period 2024–2025 at around the same rate as the growth in purchasing power.

Waning investment

Good economic growth at the start of the year has boosted private investment for 2022 as a whole, although uncertainty has been created by the war in Ukraine and the deepening energy crisis as a consequence of it (Chart 5). Both non-residential investment and housing construction this year have continued to be buoyant.

The weakening economy and the general uncertainty are slowing non-residential investment, and in 2023 the level of this investment will fall to some extent compared to the current year. Investment will be affected not only by the economic situation, but also by the rise in interest rates for corporate loans.

The fall in investment will nevertheless be temporary. As the economic situation brightens and companies gradually start to become less uncertain about the future, non-residential investment will begin to recover in 2024 and pick up further in 2025. Over the next few years, business investment will be boosted by the green transition, which is gaining renewed impetus because of the energy crisis.

chart 5.Faltering investment outlook

Housing construction has been exceptionally brisk and the demand for housing has been high for several years now. In 2021 there was a record number of new housing starts and this continued into 2022, which will mean a substantial increase in investment in housing construction for the year as a whole.

High inflation, the tightening of monetary policy that has ensued, and the decline in purchasing power have all meant that consumers and residential property investors are less interested in acquiring property. The demand for housing is expected to decrease markedly, as mortgage interest rates have risen and households have been less willing to take out a mortgage. The rate of new project starts in the immediate years ahead will also be slowed as a result of the exceptionally rapid rise in construction costs and in the financing costs faced by builders. The number of building permits issued for new homes has decreased considerably, which will be reflected as a decline in residential investment in 2023 and 2024. The amount of housing construction has been exceptionally high, but is now starting to return to its normal, long-term level.

Investment in housing construction will start to pick up again in 2025. Lower inflation, a good level of employment and an increase in disposable income will push up the demand for housing. The uncertainty surrounding the economy will also gradually dissipate. However, housing construction will not reach the volume seen in recent years.

Short-lived slowdown in export growth

Slower growth or even the threat of recession in Finland’s main export markets has caused a deceleration in Finnish export growth in 2022. A further factor has been the collapse in exports to Russia. Finland’s export growth will clearly fall below the growth in external demand this year (Chart 6). It will take time before exports to Russia can be replaced with exports to other markets, because companies are unable to replace their lost market shares immediately.

chart 6.Finland’s export growth will slow down

The growth in exports will improve only slightly in 2023, increasing more or less in line with Finland’s external demand. The growth in exports over the next few years will be spurred on particularly by the gradual fading of uncertainty in the euro area and in Finland’s other main export markets and by the easing of the energy crisis. Exports will continue to grow at roughly the same rate as in Finland’s main export markets in 2024 and 2025. The drop in Finnish exports due to the collapse of exports to Russia will be temporary, as exporting companies will discover new markets. Other factors supporting export growth in the forecast period include major deliveries of seagoing vessels.

Imports have grown exceptionally quickly in 2022, easily surpassing the growth in exports. This has reduced the figure for net exports. However, imports will decrease in 2023, as private investment and private consumption, in particular, fall. Imports will go up again in the latter part of the forecast period. Imports will increase more slowly, on average, than exports in the period 2023–2025, and so net exports will help drive economic growth. The increase in imports in 2025 will be due to greater private demand and the public investment in military equipment.

The current account deficit has grown to almost record levels in 2022, reaching around 3.5% of GDP (Chart 7). That is the largest deficit since the start of the millennium. There are several concurrent factors that explain this. The increase in imports of services has been faster than the growth in exported services for various reasons, such as the lifting of restrictions on travel, and this has caused the travel accounts in the balance of payments to weaken. Imports of goods have also been substantial, and this has weakened the trade balance. Companies have paid an unusually high amount of investment income abroad, which is clearly apparent from the weakened primary income balance. Additionally, more current transfers have been paid abroad than received from abroad.

chart 7.Current account deficit at record high

However, the current account deficit will gradually disappear, when net exports increase and strengthen the trade balance. In 2024 the current account will show a slight surplus as exports strengthen. It will, furthermore, remain virtually in balance at the end of the forecast period, although net exports will fall a little because of the rise in imports.

Short-lived improvement in public finances

Discretionary additional expenditure, surging inflation and increased interest expenditure will deepen the deficit in the public finances following a brief period of improvement. The deficit relative to GDP will narrow to almost 1% in 2022 (Chart 8). The increase in public expenditure will exceed the growth in revenues as from 2023, and the deficit relative to GDP will deepen to around 2% in the period 2023–2024. From 2025, public investment will see an increase with the procurement of fighter aircraft by the Finnish Defence Forces, and this will serve to deepen the deficit further.

chart 8.General government deficit relative to GDP will decrease only temporarily

General government revenues have continued to increase rapidly in 2022. Payroll growth and the rise in private consumption have increased tax revenues and the revenue from social security contributions. The increase in public revenues will slow down as from 2023, but this will not be dramatic, as the employment rate and earnings growth will remain fairly stable.

The central government expenditure associated with the COVID-19 pandemic has decreased, but new, additional expenditures connected with preparedness and security of supply have taken its place. The interest expenditure on central government debt had been decreasing since 2013, but has begun to rise in 2022. This will place an ever heavier burden on central government finances in the years covered by the forecast.

The cost of the wellbeing services provided by local government will be pushed up by rising prices for intermediate goods and the significant pay increases awarded in this sector. Public investment will recover as the wellbeing services counties start to function, although heavily increased construction costs will curb the start-up of new projects.

There will be a huge increase in the payment of index-linked social benefits especially in 2023, due to the sharp rise in consumer price inflation. The earnings-related pension funds’ surplus in 2022 has been strengthened by an increase in property income, but the rise in benefit expenditure will temporarily weaken the pension funds’ financial position from 2023.

The government debt-to-GDP ratio will narrow slightly over the period 2022–2023, as the nominal growth in GDP will be more rapid than the increase in the public deficit (Chart 9). The debt ratio will increase once more from 2024, ending up at almost 75% at the end of 2025. The amount of debt will rise because of defence procurement, government capital injections and other additional expenditure.

chart 9.General government debt-to-GDP ratio will start to rise again in 2024

Supply and cyclical conditions

The boom in the Finnish economy is fading and will give way to a mild recession in 2023. Growth will slow to less than its potential rate, and productive resources will be somewhat underutilised. In 2025 the economy will be in a more balanced position. The peak in the labour market has now passed, as the economic effects of the war and rising prices are transmitted to the job market. Employment will remain high throughout the forecast period, but the growth in employment will slow and the unemployment rate will increase temporarily. At the same time, labour shortages will ease somewhat in cyclical industries.

Employment rate to dip temporarily

The positive trend in the labour market that has continued up till now is levelling out. The employment rate will nevertheless remain high. As with GDP, the employment rate will drop temporarily in 2023, but it will then begin to rise and will reach 74.1% in 2025. In 2025 there will be approximately 13,000 more people in work than in 2022, on average. The unemployment rate in 2023 will rise by slightly more than half a percentage point compared to 2022, but will fall again in the coming years (Chart 10).

chart 10.Slowdown in employment growth will only be temporary

The post-pandemic labour market continued to be strong in the first half of 2022, which was due to the rebound in demand for labour-intensive services following the lifting of restrictions. The employment rate has risen to a record high, while the level of unemployment has fallen to just below the structural unemployment rate. At the same time, however, employers have had difficulties finding skilled workers and the number of job vacancies relative to the number of unemployed jobseekers has increased (Chart 11). Despite the tightness of the labour market, employment continued to rise during the first half of 2022. Unemployment has fallen, although by less than the rate at which employment has improved. The labour force participation rate has risen to a remarkably high level.

The peak in the labour market has nevertheless now passed. The rise in the rate of employment will halt temporarily, with the unemployment rate increasing to some extent in the early part of the forecast period. The weakened expectations for employment in all the main industries point to a cooling labour market. This has not so far led to an increase in temporary lay-offs, unlike during the pandemic; instead, the level of unemployment has risen. In 2023 employment growth will slow as private consumption falls, triggered by a decrease in the demand for services and weak purchasing power. At the same time, the number of lay-offs may increase.

chart 11.Tightness of the labour market to ease slightly

The labour shortages and tight labour market are the result of both cyclical and structural factors. The tightness of the labour market will ease slightly as the economy cools, which will mitigate the labour shortages in cyclical industries. However, the labour shortages will also remain a longer term structural problem in Finland. The structural labour shortage in many non-cyclical industries – for example, healthcare and care for older people – is partly due to Finland’s ageing population, and so this can be expected to impede employment growth across business cycles. The rapid rise in the labour force participation rate has eased the labour shortages to some extent. Since the participation rate is already at a record high, and its rise is to slacken off over the forecast period, it cannot be expected in the future to ease the tightness of the labour market or promote any substantial increase in employment unless there are new structural measures in place.

Finnish economy to enter a mild recession

Finland’s economy, with the exception of the public finances, had largely recovered from the deep recession caused by the COVID-19 pandemic when the next crisis hit. Thanks to a good start to the year, there has been rapid growth in 2022 and the output gap has remained positive.5 But due to the crisis caused by the war in Ukraine and the subsequent further rise in energy prices, the assessment of cyclical conditions for the coming years has been adjusted downwards. According to current estimates, the Finnish economy will slide into recession in 2023, and GDP growth will slow to less than the growth potential. The output gap will therefore be negative (Chart 12). In 2025 the economy will be in a more balanced position, with an output gap that is more or less neutral and growth close to its potential rate.6

The war is undermining growth in the economy via its impact on both demand and supply. The uncertainty caused by the war is weakening domestic demand and causing a contraction in Finland’s export markets, and the war is also worsening global supply disruptions and pushing up the prices for energy and other raw materials. Nevertheless, the supply disruptions and general uncertainty are expected to ease gradually.

chart 12.Output gap in Finland and the euro area

Finland’s potential output growth was already recovering from the setback experienced during the COVID-19 crisis when Russia attacked Ukraine (Chart 13). The growth in potential output will remain slow over the forecast period, partly due to weaker-than-projected growth in investment and therefore also in the stock of capital. The war and continuing high prices for energy are expected to reduce the economic growth potential during the next few years. GDP growth is projected to be close to its long-term potential rate at the end of the forecast period.

High levels of structural unemployment will make labour a less significant factor in output in the forecast period.7 The labour supply will also be constrained by the fact that the working age population (aged 15–74) has already started to shrink. On the other hand, and despite headwinds in the economy, a continued high participation rate will support labour input and potential output.

Capital stock is slowly growing, contributing to growth in potential output. Growth in total factor productivity will remain subdued temporarily, due to supply disruptions and a reallocation of resources. Global tensions and supply disruptions are prompting some companies to look for new subcontractors, reorganise production chains and ensure uninterrupted availability of energy. It is especially during crises that structural rigidities and frictions in the economy play an important role in how effectively economic resources are reallocated and how quickly potential output improves.

chart 13.Potential output to grow slowly

The war in Ukraine may affect potential output in many ways, which is why the projection is subject to more uncertainty than usual. The war may have a prolonged or even a permanent negative impact on the economy’s growth potential if it leads to permanently reduced international trade and a less effective global division of labour. This in turn would slow down productivity growth. On the other hand, diversifying critical production chains and moving production closer to the domestic market may reduce the risk of supply disruptions and improve economic resilience going forward.

Growth in the stock of capital will be affected by two opposing forces. On the one hand, the reorganisation of production and a massive investment in the green transition will increase the capital stock, but, on the other hand, possible cancellations of investment due to the war will have an adverse impact on capital stock growth.8 Part of the capital stock may become obsolete if there are major disruptions in the availability of oil and gas or if prices stay high permanently. A permanent increase in the cost of energy could well weaken potential output via a number of impact channels (e.g. ECB: How higher oil prices could affect euro area potential output9). The war is not expected to have any major impact on the overall trend in the labour supply in the forecast period, partly because migrants generally only find work in Finland after a relatively long time lag.

Prices and costs

Inflation has continued to accelerate in 2022 due to the effects of the war in Ukraine and the pandemic. Higher prices for energy and raw materials and protracted supply chain disruptions have led to a widespread rise in consumer prices. Nominal earnings have increased substantially less than inflation, and so real earnings have actually fallen this year. However, the inflation rate will come down in the immediate years ahead, and nominal earnings are projected to rise by more than prices in the period 2024–2025. Finland’s cost competitiveness relative to the euro area as a whole is expected to remain almost unchanged in the forecast period 2022–2025.

Inflation will fall in the forecast period

Inflation has increased rapidly towards the end of 2022. The provisional figure for inflation in November, measured by the Harmonised Index of Consumer Prices (HICP), was 9.1%. The sharp rise was still due in large part to increased energy prices, although inflation has broadened out across the economy during the year. Despite the accelerating inflation, however, there are also signs that the pressure on prices is easing. For example, recent months have seen a slowdown in the rising prices of consumer durables.

Inflation will fall to 5% in 2023, as the inflation-fuelling effects of supply factors grow weaker (Chart 14).10 International freight costs have decreased, and the bottlenecks in production have eased in many places. The fall in crude oil and raw material prices will curb the increase in consumer prices, although, on the other hand, dearer electricity will prolong price pressures, especially in the coming winter months. Some of the accumulated cost pressures will eventually transfer to the prices of food, consumer goods and services.

The low level of consumer confidence and the fall in demand for consumer goods will start to bring inflation down in 2023. In a survey of consumer confidence, respondents felt that these are especially bad times for making purchases, and purchase intent regarding consumer durables in particular was very low. The tightening of monetary policy will also slow the rise in consumer prices during the course of 2023. Nevertheless, the expected rise in earnings will push up prices of services, meaning that underlying inflation will be slightly higher than in 2022.

chart 14.Inflation still high in 2023

In 2024 inflation will slow to less than 2%. Current market expectations indicate that the wholesale prices for crude oil, electricity and gas will decrease, and so consumer prices for energy will begin to fall. The rise in food and consumer goods prices will be much slower than in the two previous years. Services inflation will also fall compared to the year before, but will remain above the long-term average as real earnings start to climb once again. In 2025 inflation will rise slightly as energy prices decline less steeply and consumer demand picks up due to a rise in purchasing power. The underlying inflation rate will slow towards the end of the forecast period, but will remain at just over 2%.

Real earnings will start to rise again

The growth in nominal earnings this year is expected to be 2.6%, measured by the index of wage and salary earnings (Chart 15). Nominal earnings growth in 2023 will rise to above 4%. In the later years of the forecast period the increase in earnings will slow down again. The earnings forecast assumes that real wages will increase at approximately the same rate as productivity – this assumption is based on a long-term link observed between these two variables. Real earnings will fall in 2022 and 2023 on account of high inflation, but will rise in the latter part of the forecast period as inflation slows.

chart 15.Nominal earnings growth to rise in 2023

The cost of labour, or compensation per employee, has increased by 3.7% in 2022 from the previous year, supported by the increase in the employment rate. The cost of labour will continue to increase in 2023, after which it will gradually decrease again. The higher cost of labour and weak growth in labour productivity will push up nominal unit labour costs significantly in 2023. In 2024 and 2025 the cost of labour will rise less markedly and labour productivity will return to growth, causing nominal unit labour costs to increase more modestly towards the end of the forecast period.

Projections of aggregate unit labour costs adjusted for the terms of trade suggest that Finland’s cost competitiveness relative to the euro area as a whole will remain almost unchanged in the period 2023–2025 (Chart 16). However, there is considerable uncertainty surrounding projections of cost competitiveness because of the impacts of the war in Ukraine and the energy crisis, and the change in labour costs.

chart 16.Finland’s cost competitiveness relative to the euro area will remain virtually unchanged in the period 2023–2025

Risk assessment

The risks surrounding the forecast are predominantly on the downside. Finland’s external environment is becoming more volatile due to the war in Ukraine. A more prolonged period of high inflation in Finland than forecast could cut consumers’ purchasing power and private consumption by more – and for longer – than was projected, and this would make an economic recession deeper than expected.

Housing construction is expected to slow down gradually. If the economy performs less well than forecast and the rise in interest rates is faster than predicted, this could cause the housing market to cool down more than expected, which would be reflected quickly in the supply of new housing.

It is still difficult to assess all the economic consequences of Russia’s war in Ukraine. In the Bank of Finland’s December 2022 forecast the assumption is made that the prices for electricity and crude oil will gradually start to fall next year, although the energy crisis may also deepen further. The worsening problems of energy availability across Europe could weaken demand in Finland’s export markets and so slow down the growth in exports. Furthermore, a cold winter with many windless days may push up the price of electricity and compel regulation of its distribution in Finland.

In addition, the COVID-19 pandemic is not yet over in global terms. Although the global supply chain disruptions that emerged during the pandemic began to ease in early 2022, the number of COVID-19 cases, for example in China, has started to rise again fast. If the disease cannot be contained, this could lead to production and logistics bottlenecks.

According to the forecast, inflation will start to slow down in 2023. There is much uncertainty in the forecast, however, as price rises in 2022 have now spread from energy commodities to other sectors of the economy. Moreover, the energy crisis could continue, and energy prices increase, for longer than expected.

Despite rising costs, corporate profitability has remained good, though this will increase wage pressures in pay negotiations in the winter. The pressure on wages will also be intensified if there are higher than usual pay rises in competitor countries. There are nevertheless large differences in profitability between different industries and among companies, and the slowdown in the economy will become visible in company results only after a time lag. If wage rises cannot be funded without price increases, there is an increased risk that consumer prices will rise faster than anticipated.

Besides any negative developments, Finland’s economic growth in the next few years could also include positive surprises. The reduction in aggregate demand and the tightening of monetary policy may slow down inflation faster than anticipated, which would increase the purchasing power of households more than forecast. Furthermore, the exporting companies that have pulled out of the Russian market may succeed in discovering new markets more quickly than expected. The green transition has been gathering pace as a consequence of the energy crisis, and this could increase investment and provide companies with new export opportunities.

Notes

-

The alternative scenario ‘Household consumption could be hard hit in the energy crisis’ examines a situation where the energy crisis escalates and winters are colder than normal in the immediate years ahead. ↑

-

More detailed information on the euro area forecast is available on the ECB website. ↑

-

More detailed information on the ECB’s monetary policy decisions is available on the ECB website. ↑

-

The impact of interest rate rises on private consumption is dealt with in more detail in the alternative scenario. ↑

-

The difference between GDP and potential output is referred to as the output gap and is usually expressed as a percentage of potential output. According to economic theory, a positive output gap cannot be maintained without upward pressure on wages and prices. ↑

-

Potential output is the volume of GDP when all the inputs in the economy are in normal use. ↑

-

The NAIRU (non-accelerating inflation rate of unemployment) is estimated to be around 7.5% during the forecast period. ↑

-

Greater uncertainty and the high cost of energy, for example, will discourage investors. ↑

-

ECB Bulletin 5/2022, Box 4. ↑

-

Inflation in 2023 is forecast to be 5.0%, measured by the euro area’s Harmonised Index of Consumer Prices (HICP). However, using the national Consumer Price Index (CPI), inflation is projected to be 5.5%. The CPI figure is higher mainly on account of the rise in average mortgage interest rates. ↑