Forecast

Finland’s economy is in recession and the recovery will be slow

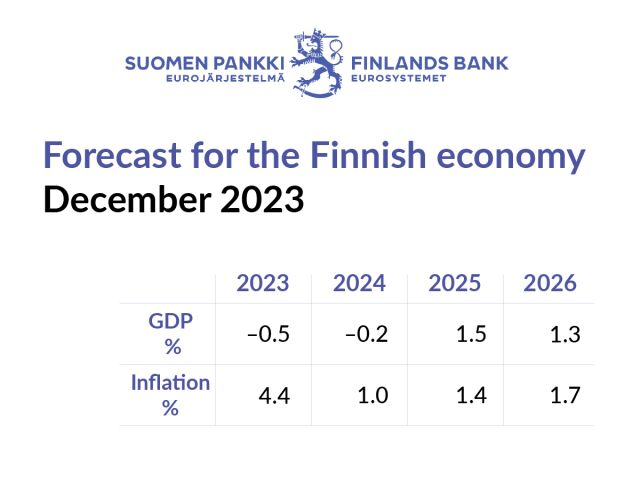

The Finnish economy is in recession. GDP will contract by 0.5% in 2023 and by 0.2% in 2024. The weakness in the economy is widespread. However, households’ purchasing power is improving as inflation slows rapidly. In addition, the financial markets are expecting interest rates to fall in the forecast years. Growth in Finland’s export markets will gradually recover, which will support the recovery of GDP growth from the latter part of 2024. Bringing the public finances onto a different path is proving more challenging than expected, due to the weak economy.

Overview

Growth is currently weak in Finland’s main export markets, making the outlook for exports rather uncertain. However, demand in the export markets will pick up after a brief respite. Export growth will be supported by the euro area’s declining level of inflation and its robust labour market.

Financing conditions have tightened considerably due to the rise in interest rates. Even so, the findings of the euro area bank lending survey (BLS) show that the credit standards and terms and conditions for new loans have not been widely tightened in Finland. The markets expect the 3-month Euribor to decline gradually, on average to below 3% in 2025.

In Finland, inflation has slowed in line with expectations in 2023 and will remain moderate throughout the forecast years 2024–2026. The decline in prices of energy and other production inputs is already feeding through to consumer prices, and due to the tightening of monetary policy and the weak economy, price pressures will continue to be minor, especially in 2024.

Core inflation will fall gradually as nominal earnings growth slows during the forecast period from the high figures of 2023. Finland’s cost competitiveness will be below that of the euro area in 2023, but the lost ground will be recovered in 2024–2026.

Aggregate demand in the economy will weaken across a broad front in 2023 and 2024. Private consumption will be down considerably in 2023. High prices and the low level of consumer confidence in the economy will hold back the growth of private consumption in 2024 as well. The purchasing power of households will gradually recover, but the rise in real interest rates will encourage households to save a greater proportion of their earnings. Growth in private consumption will pick up towards the end of the forecast period as confidence improves and purchasing power continues to grow.

Private investment is declining markedly. Investment in residential construction will be sharply down in both 2023 and 2024. The steep increase in interest rates, the rapid rise in costs for businesses and waning demand are causing a reduction in non-residential investment. Both residential construction and non-residential investment will pick up in 2025, as declining interest rates and recovering exports create space for new investment.

Exports will be down in 2023. However, net exports are supporting GDP growth in 2023, as the weakness of domestic demand is causing an even larger drop in imports than in exports. Exports will continue to decline in 2024 as well, as the weakening of investment and world trade will erode Finland’s exports. Exports will start to grow in 2025 in the wake of GDP growth in the export markets. As a whole, export growth will be quite modest over the forecast years.

Due to the weak economy, the labour market situation will deteriorate in 2023 and 2024. The unemployment rate will rise to 7.8% in 2024, which is above the level of structural unemployment. The employment situation is weakening but will remain relatively good due to the continuing labour shortages in many sectors, despite the weak cyclical conditions. In addition, the number of hours worked per employee has fallen in recent years, which in turn increases the need for recruitment. Towards the end of the forecast period, employment will improve further, as confidence in the economy picks up and private consumption recovers.

The general government deficit and public debt are increasing. The cuts in public expenditure planned by the new Government are significant, but their impact will be dampened by the weak growth in revenues from taxes and tax-like payments and the growing cost pressures on public finances.

The general government deficit relative to GDP will grow to 1.6% in 2023 and will increase further to approximately 3.5% in the years 2024–2026. Finland’s public finances will be undermined in the coming years by significantly lower growth in tax revenues and reductions in social security contributions, as well as by strong growth in social benefits paid and in public demand and interest expenditure. The public debt-to-GDP ratio will exceed 80% in 2026.

Finland’s economy has suffered a series of major shocks

The Finnish economy has gone through a number of major disruptions in recent years, which has led to significant cyclical fluctuations. The Bank of Finland’s Aino 2.0 model can be used to interpret cyclical fluctuations and to assess the significance of different economic shocks in terms of these fluctuations. Chart 1 breaks down GDP growth in 2020–2026 into factors that explain the economic fluctuations.

After the initial shock caused by the COVID-19 pandemic, the recovery of domestic and foreign demand strongly supported economic growth (Chart 1, ‘demand’), but the widespread supply disruptions caused by the pandemic also slowed economic growth in 2021 and 2022 (Chart 1, ‘supply’). These abrupt changes in demand and supply combined with the rise in raw material prices driven by Russia’s war in Ukraine led to a surge in global prices.

In 2023, rising global prices slowed growth in the Finnish economy, but it is estimated that their effects will not continue into 2024–2026 (Chart 1, ‘global prices’). Nevertheless, the dissipation of bottlenecks in the global economy has eased the economic situation.

Domestic and foreign demand was very weak in 2023 and is expected to further dampen economic growth in 2024. However, according to the Bank of Finland’s December 2023 forecast, demand will strengthen during 2024 and start to gradually support growth.

Due to high inflation, monetary policy has been tightened considerably, and the negative impact of this on growth in the Finnish economy will be at its greatest in 2023 and 2024 (Chart 1, ‘financing conditions’). The tightness of financing conditions will be a relatively significant factor weighing on GDP growth in 2024, as the effects of weak demand and high global prices begin slowly to diminish. In 2025 and 2026, financing conditions will no longer significantly limit economic growth (see Alternative scenario: Higher interest rates are slowing inflation and economic growth in Finland).

chart 1.Finland’s economy has suffered a series of major shocks

| Percentage change on the previous year | |||||

|---|---|---|---|---|---|

| 2022 | 2023f | 2024f | 2025f | 2026f | |

| GDP | 1.6 | -0.5 | -0.2 | 1.5 | 1.3 |

| Private consumption | 1.7 | -0.8 | 0.5 | 1.3 | 1.2 |

| Public consumption | 0.8 | 3.7 | 0.3 | 0.0 | 0.9 |

| Fixed investment | 3.2 | -5.5 | -0.8 | 4.4 | 2.4 |

| Private fixed investment | 4.0 | -3.8 | -4.3 | 2.5 | 3.5 |

| Public fixed investment | -0.2 | -13.6 | 18.2 | 12.9 | -1.8 |

| Exports | 3.7 | -1.2 | -1.4 | 2.5 | 3.0 |

| Imports | 8.5 | -7.2 | -1.3 | 3.0 | 3.1 |

| Effect of demand components on growth | 2022 | 2023f | 2024f | 2025f | 2026f |

| Domestic demand | 1.8 | -0.8 | 0.2 | 1.7 | 1.5 |

| Net exports | -1.9 | 2.9 | -0.0 | -0.2 | -0.0 |

| Changes in inventories and statistical error | 1.7 | -2.6 | -0.3 | 0.0 | 0.0 |

| Savings rate, households, % | -0.9 | 1.0 | 1.5 | 0.6 | 0.4 |

| Current account, % of GDP | -2.5 | -0.5 | -0.2 | -0.3 | -0.3 |

| 2022 | 2023f | 2024f | 2025f | 2026f | |

|---|---|---|---|---|---|

| Labour market | |||||

| Number of hours worked | 2.2 | -0.3 | -1.2 | 0.5 | 0.5 |

| Employment rate (20–64-year-olds), % | 78.1 | 78.0 | 77.2 | 77.4 | 77.7 |

| Unemployment rate, % | 6.8 | 7.2 | 7.8 | 7.5 | 7.3 |

| Unit labour costs | 4.1 | 5.5 | 1.3 | 1.6 | 1.8 |

| Labour compensation per employee | 2.9 | 4.2 | 1.5 | 2.8 | 2.9 |

| Productivity per employee | -1.1 | -1.2 | 0.1 | 1.2 | 1.0 |

| GDP, price index | 5.4 | 5.3 | 1.8 | 1.8 | 2.1 |

| Private consumption, price index | 6.1 | 4.8 | 1.5 | 1.6 | 1.9 |

| Harmonised index of consumer prices | 7.2 | 4.4 | 1.0 | 1.4 | 1.7 |

| Excl. energy | 4.8 | 5.0 | 2.0 | 1.9 | 1.9 |

| Energy | 31.0 | -1.6 | -8.7 | -3.8 | -0.0 |

| General government, % of GDP | 2022 | 2023f | 2024f | 2025f | 2026f |

| General government balance | -0.8 | -1.6 | -3.7 | -3.6 | -3.5 |

| General government gross debt (EDP) | 73.3 | 75.0 | 77.0 | 79.2 | 81.2 |

| f = forecast. | |||||

| Sources: European Central Bank and Bank of Finland. |

Operating environment: assumptions and financing conditions

World trade growth will gradually pick up in the years ahead. Demand will also strengthen in Finland’s export markets. Tighter monetary policy will continue to restrain growth in the world economy in 2024. However, in the longer term, growth will be supported by the anticipated relaxing of financing conditions and the fall in the rate of inflation. The Bank of Finland’s forecast is based on the data available on 30 November 2023.

Global economy will grow moderately and inflation will slow

Global economic growth has been supported by strong service consumption and robust labour markets. The strength of domestic markets in the main economic regions worldwide has compensated for the weak performance of international trade, which has suffered from a lack of momentum in the goods trade (Chart 2). However, growth in the global economy has slowed in the latter half of 2023 as monetary policy has been tightened and China’s economic growth has lost steam after its recovery from the pandemic.

Rising raw material prices have delayed the slowing of inflation globally. In addition, underlying inflation, which excludes food and energy prices, has been slow to come down. The global economy is projected to grow moderately in the coming years (Table 2). The problems in China’s real estate sector will continue to weigh on the country’s domestic demand in the immediate years ahead. Although tighter monetary policy will continue to weaken global growth in 2024, the falling level of inflation will support demand in the longer term.

chart 2.Demand growth in Finland’s export markets will strengthen

The growth in world trade is expected to pick up gradually. Demand growth in Finland’s export markets will also start to grow after a brief respite (Chart 2, Table 2). However, growth is currently weak in Finland’s key export markets, such as Sweden and Germany. Finland’s export outlook for the coming quarterly periods is consequently rather uncertain. In recent years, the United States has become one of Finland’s main trading partners. The US economy has grown strongly this year and growth is projected to continue in the coming years, though at a slightly more moderate rate.

The prices of oil and raw materials have remained comparatively high and have fluctuated somewhat due to geopolitical tensions and supply constraints. Oil prices are expected to decline moderately in the coming years, to just over USD 70 per barrel, according to market expectations (Table 2). Raw material prices will still remain rather high in the coming years, in line with market expectations. Uncertainty in the raw material markets is exacerbated by ongoing wars and by climate-related supply risks, and this could be reflected in the prices of energy and other raw materials.

Economic growth in the euro area has been dampened by the tighter financing conditions, frail confidence and weak exports.1 However, growth in the economy is expected to strengthen in 2024 (Table 2), when inflation will fall, wages will rise, employment will remain resilient and export growth will rebound. In the longer term, the slowing effect that tighter financing conditions have on growth will dissipate, and growth in the euro area economy will strengthen further in 2025.

Euro area inflation has continued to fall as a result of declining energy prices, tighter monetary policy and the easing of supply bottlenecks. Inflation will slow gradually to around 2% in 2025. Underlying inflation, which excludes food and energy prices, will also slow, to just over 2% in 2025. The factors contributing to underlying inflation in the euro area include particularly the rise in wages.

Financing conditions have become considerably tighter

At its December meeting, the European Central Bank (ECB) decided to keep its key interest rates unchanged.2 The most important of these, the deposit facility rate, has been at 4.00% since 20 September, while the main refinancing operations rate has been at 4.50% and the marginal lending facility rate at 4.75%. The ECB's Governing Council is determined to ensure that inflation returns to its 2% medium-term target in a timely manner. The Governing Council considers that interest rates are currently at levels that, maintained for a sufficiently long duration, will make a substantial contribution to this goal. Previous interest rate increases continue to be transmitted forcefully to the economy. Future interest rate decisions will be based on an assessment of the inflation outlook, the dynamics of underlying inflation and the strength of monetary policy transmission.

chart 3.Average interest rates on new loans have risen steeply

Interest rates have risen strongly over the past two years (Chart 3). However, market interest rates have fallen considerably in recent weeks and are now at a lower level than in the forecasting assumptions made at the end of November (Table 2). The markets currently expect the 3-month Euribor rate to decline gradually and thus financing conditions to become more relaxed in the coming years.

The euro area Bank Lending Survey indicates that Finnish banks have not extensively tightened their credit standards or terms and conditions for new loans. According to the Confederation of Finnish Industries’ Business Tendency Survey, the prevalence of financial difficulties has risen slightly in recent quarterly periods, but the number of companies reporting financial difficulties remained low. Financial difficulties hamper growth especially in the construction sector, with almost 20% of companies in that sector reporting financial difficulties in the third quarter.

| Volume change year-on-year, % | |||||

|---|---|---|---|---|---|

| 2022 | 2023f | 2024f | 2025f | 2026f | |

| Euro area GDP | 3.4 | 0.6 | 0.8 | 1.5 | 1.5 |

| World GDP (excl. euro area) | 3.3 | 3.3 | 3.1 | 3.2 | 3.2 |

| World trade* (excl. euro area) | 5.5 | 1.1 | 3.0 | 3.0 | 3.2 |

| 2022 | 2023f | 2024f | 2025f | 2026f | |

| Finland’s export markets**, % change | 6.2 | 0.2 | 2.0 | 2.9 | 3.0 |

| Oil price, USD/barrel*** | 103.7 | 84.0 | 80.1 | 76.5 | 73.6 |

| Export prices of Finland’s competitors, EUR, % change | 18.9 | -4.1 | 1.6 | 2.6 | 2.3 |

| 3-month Euribor, %*** | 0.3 | 3.4 | 3.6 | 2.8 | 2.7 |

| Finland’s nominal effective exchange rate**** | 106.6 | 110.3 | 111.3 | 111.3 | 111.3 |

| USD value of one euro***** | 1.05 | 1.08 | 1.08 | 1.08 | 1.08 |

| * Calculated as the weighted average of imports. | |||||

| ** The growth in Finland’s export markets is the import growth in the countries Finland exports to, weighted by their average share of Finland’s exports. | |||||

| *** Technical assumption derived from market expectations. | |||||

| **** Broad nominal effective exchange rate, 2015 = 100. The index rises as the exchange rate appreciates. | |||||

| ***** Assuming no changes in the exchange rate. | |||||

| f = forecast. | |||||

| Sources: European Central Bank and Bank of Finland. |

Demand and the public finances

Aggregate demand in the economy will weaken across a broad front in 2023 and 2024 (Chart 4). Private consumption, private investment and exports are all slowing. The weakness of domestic demand nevertheless means there will be an even larger drop in imports than in exports in 2023, and so net exports are supporting GDP growth in the short term. The purchasing power of households will gradually strengthen and, according to market expectations, interest rates will start to decline. Growth in Finland’s export markets will also see a recovery. As a result, growth in the Finnish economy will pick up from the latter half of 2024. In 2025–2026, GDP growth will return close to its long-term average. The public finances will remain deeply in deficit throughout the years 2023–2026. The cuts in public expenditure planned by the new Government are significant, but their impact will be dampened by the weak growth in revenues from taxes and tax-like payments and the cost pressures related to public spending.

chart 4.Finnish economy will contract in 2023 and 2024

Household purchasing power will improve and support consumption

Real incomes of households will increase and purchasing power will recover in both 2023 and 2024, as consumer price inflation has slowed in 2023 and will continue to slow down markedly (Chart 5). Earned income and current transfers have also increased rapidly in 2023 on account of pay rises and index-linked increases in pensions and other social benefits. Tax reductions and index-linked increases in pensions and in certain other benefits will also boost purchasing power in 2024. Thus, in 2024, the real disposable income of households will return to its 2021 level, and the purchasing power lost due to inflation will be recovered. In subsequent years, employment growth will rebound in line with cyclical conditions, sustaining the positive trend in households’ purchasing power.

Private consumption for the full year 2023 will see a significant decrease and will improve only weakly in 2024. Purchasing power deteriorated exceptionally strongly in 2022 on account of high inflation, and this has continued to dampen consumption in 2023 (Chart 5). Households remain cautious for now, as expectations about the economy are weak and uncertainty elevated. The consumption of services is dwindling, as the strong post-pandemic growth in the demand for services is now over. With the markedly higher interest rates and subdued housing market, the demand for durable consumer goods will also decline in 2024. Consumption will start to recover slowly in 2024 in response to the improvement in household purchasing power, the financial markets’ expectations of a slight decline in interest rates, and the growing confidence in the economy. In 2025–2026, private consumption growth will return more or less to its pre-pandemic level.

Many households have used part of their savings to cover the sharp rise in the cost of living and in interest payments over the past two years. As inflation slows down, this will once again create room for saving. Savings will also be bolstered in the coming years by the higher and distinctly positive level of real interest rates. The household savings rate will be positive throughout the forecast period 2023–2026.

chart 5.Stronger purchasing power will support private consumption

Steep fall in housing construction

In the latter half of 2022, growth in private investment took a discernible turn for the worse due to high inflation, rising interest rates and greater economic uncertainty. The outlook for housing construction in particular darkened rapidly. Private investment will be down considerably in 2023 and 2024, owing to the rapid rise in interest rates and the decline in domestic and foreign demand (Chart 6).

chart 6.Residential investment plunges

Housing construction in Finland experienced a boom until 2022. A significant number of dwellings were built, even in excess of needs. In 2023 and 2024, housing construction will decrease substantially (Chart 6). The numbers of residential building permits and starts have declined sharply for more than a year now. There has also been an increase in the number of new homes constructed but not yet sold.

Higher interest rates on housing loans have meant that the demand for new mortgages has decreased markedly and households have been much less willing to borrow. Interest in buy-to-let housing has also waned notably. Housing construction will start to pick up in the latter half of 2024, influenced by the financial market expectations that interest rates will gradually start declining. Demand will also strengthen.

The outlook for non-residential investment has also weakened considerably over the past year. The steep rise in interest rates and costs for businesses and the waning demand have made businesses less willing to invest in 2023 and this will continue in 2024.

Private investment will not start to recover until 2025, when the market expects a slight fall in interest rates and the demand outlook improves. With the global economy strengthening and exports picking up, there will be more room for new investment. Investment growth will gather pace at the end of the forecast period, when the green transition will also gradually start to boost investment in the energy industry, in particular. Nevertheless, investment ratios3 will still remain relatively low by historical standards (Chart 7).

chart 7.Investment ratio falling

Near-term outlook for exports is modest

Finnish exports started to falter at the end of 2022 and the same trend continued in 2023. Export growth has been markedly weaker than the growth in Finland’s export markets for two years now. Although Finnish exports increased by slightly over 3.5% in 2022, the growth in Finland’s export markets was a little over 6% (Chart 8).

Exports will be down by just over 1% in 2023. Nevertheless, net exports will remain positive, as imports will be down by significantly more than exports due to weak domestic demand. Exports will continue to decline in 2024 on account of the weakness in investment demand among Finland’s trading partners and the gloomy outlook for domestic companies’ exports. Finnish exports are strongly weighted towards intermediate goods and capital goods and are sensitive to movements in demand and interest rates. Finding replacements for the lost Russian markets has also taken significantly longer than expected. The reduction in tourism from Russia and Asia is curbing Finland’s services exports.

The global economy will strengthen slightly and Finland’s main export markets will pick up in 2024, which will gradually increase export demand. Exports will start to grow in 2025 in the wake of growth in export markets. Although Finland’s exports will grow roughly at the same rate as its main export markets in 2025 and 2026, the overall trend in exports looks rather modest over the forecast period. The growth in imports will also be rising at the same time, leaving net exports at a weak level.

chart 8.Exports grew by less than the growth in export markets

The current account deficit increased to almost EUR 7 billion in 2022 (Chart 9). The 2023 deficit will be smaller, however, particularly as a result of a stronger trade balance, as the value of imports has declined faster than the value of exports. On the other hand, the services account will remain in deficit due to the structural imbalance of the travel account (for more details, see Alternative scenario: Higher interest rates are slowing inflation and economic growth in Finland).

The current account will remain in deficit throughout the forecast period, although the deficit will contract towards the end of the period as export growth picks up. Despite this contraction, the current account will not be fully balanced but will remain around 0.5% in deficit in 2026. In 2025–2026, the deficit will be fuelled particularly by public sector defence procurement.

chart 9.Current account will remain in deficit

Cost pressures hampering rebalancing of public finances

The expenditure savings4 planned by the new Government that took office in summer 2023 are significant, but their positive impact on the budgetary position is being offset by a number of factors weakening the public finances. Finland’s public finances will be undermined in the coming years by significantly lower growth in tax revenues and reductions in social security contributions, as well as by strong growth in social benefits paid and in public demand and interest expenditure. The general government deficit relative to GDP will grow to 1.6% in 2023 and will increase further to approximately 3.5% in the years 2024–2026 (Chart 10).5

chart 10.Planned expenditure cuts diluted due to weakening tax and social security contribution revenue and rising cost pressures

Due to the weak cyclical conditions, growth in revenues from income tax and value added tax will slow considerably following the strong increase in recent years. In 2023, revenues accrued from excise tax and other indirect taxes (excl. VAT) will decrease from the previous year and the weak trend will continue in the coming years. Social security contributions collected will decrease due in particular to a reduction in unemployment insurance contributions in 2024. On the other hand, social benefits paid will increase significantly in 2023 and 2024 on account of index adjustments, although this increase will be curbed from 2024 onwards by a temporary freezing of some of the adjustments.

Spending related to, among other things, security, immigration and health and social services will push up public final consumption expenditure. Further factors contributing to higher final consumption expenditure include wage increases and lump sum payments as well as higher prices of intermediate products. With the launch of various investment projects of municipalities and wellbeing services counties, the extent of public investment will increase in 2024 from the low levels seen in 2023. Investment will continue to grow in 2025 due to the substantial defence procurement projects at central government level.

Contingency measures, higher interest payments and growing R&D funding will deepen the central government deficit (Chart 10). At the same time, local government expenditure will be driven up by the health and social services reform that entered into force at the beginning of 2023, as well as by population ageing and investments. The surplus of the social security funds will dip temporarily in 2024 in response to higher pension benefits and other benefits and a reduction in social security contributions. Growth in interest income of earnings-related pension providers and central government will offset the growth in public expenditure. However, with the government debt rising and interest rates increasing, general government interest expenditure will once again climb above interest income at the end of the forecast period.

The consolidated nominal general government debt will grow annually by an average of over EUR 12 billion in the immediate years ahead. The debt-to-GDP ratio will be 75% at the end of 2023 and will rise to 81% by the end of 2026 (Chart 11). This rise will stem from higher general government deficits and, in 2024 in particular, from weak growth in nominal GDP. The debt will also increase slightly for statistical reasons, but some of these factors are temporary.6

chart 11.Growth in the general government debt ratio will accelerate from 2024 onwards

Supply and cyclical conditions

The Finnish economy is in recession in 2023 and will also be in recession in 2024. In both years GDP growth will be below its growth potential. Employment is falling and, due to cyclical factors, the unemployment rate will climb above the level of structural unemployment. When the economic headwinds ease, the labour market will improve and the economy will start to be in a more balanced position. In 2026, GDP is forecast to increase close to its longer term growth potential, and the output gap will have almost closed.7

Unemployment will increase temporarily

Due to the weak cyclical conditions, the strong employment growth witnessed in recent years levelled off already in the first half of 2023. The easing of pressure in the heated labour market, which has long suffered from labour shortages, has been evident in the form of a rapid drop in job vacancies and a partial easing of labour shortages. As a consequence, the decrease in the employment rate has thus far been only small in relation to the cyclical conditions, declining from its peak of slightly over 78%. The number of hours worked has declined and the rapid growth in the labour force in recent years has halted. Unemployment has started to increase in 2023 and the unemployment rate is estimated to be close to the level of structural unemployment.

The employment rate (20–64-year-olds) is projected to decline in 2024 to approximately 77% (Chart 12). Despite this weakening, the employment rate will stay high, which means that a large portion of the employment growth from 2021–2022 will remain permanent. This is partly because the number of hours worked per employee has fallen in recent years. With the greater prevalence of part-time employment and the decrease in the number of hours worked by those in full-time employment, recruitment needs have increased. On the other hand, in many industries labour shortages will continue despite the weak cyclical situation, and so companies will try to hold on to staff where possible. The growth in public sector employment even in a weak cyclical situation is in part due to the demand for health and care services remaining unchanged even amid a recession.

chart 12.Slowdown in employment growth will only be temporary

The unemployment rate is projected to rise to 7.8% in 2024. The sharp fall in construction activity will lead to job losses, and unemployment will also increase in the other industries. This is indicated by companies’ employment expectations and the recent notices of temporary lay-offs in manufacturing. However, the unemployment rate is expected to rise only slightly above the level of structural unemployment, as the economy is suffering from a structural shortage of labour across economic cycles (e.g. in healthcare and care for older people). Thus, despite their rapid decline, the number of job vacancies and the labour shortage indicators have remained high in relation to the cyclical conditions.

Employment will start to improve again in 2025, when confidence in the economy strengthens and private consumption recovers. The employment rate will reach 77.7% in 2026, and at that time there will be approximately 2,000 fewer people in work than the average for 2023. The growth in employment will be restricted by the record high labour force participation rate. This cannot in future be expected to ease labour market tightness or fuel employment growth significantly without new structural measures. Unemployment will start to decline as cyclical conditions improve in 2025, and the unemployment rate will decrease to 7.3% in 2026. The unemployment rate at the end of the forecast period will be close to its structural level, which will restrict growth in employment (Chart 13).

chart 13.Unemployment rate will rise above the level of structural unemployment

Finland’s economy is in recession

GDP growth will slow in 2023 and 2024 to below the economy’s growth potential, and the output gap will be clearly negative (Chart 14). As a consequence, the Finnish economy is in recession in 2023 and will be in recession in 2024. Growth will strengthen in 2025, and towards the end of the forecast period in 2026 the economy will be in a more balanced position, with the output gap near zero and GDP growth close to its potential figure.

chart 14.Finland’s economy is in recession

The growth in potential output in Finland will continue to be slow across the forecast period, rising at an average annual rate of less than 1% (Chart 15). The trend in all production factors will be muted.

This subdued growth in potential output will be due to the weak trend in investment and therefore in the capital stock. The growth in total factor productivity will be temporarily subdued owing to the recent crises, among other things. Some companies have had to reorganise their production chains and resort to more expensive inputs.8

Growth in the supply of labour input will be slow. The high structural unemployment rate will reduce the importance of labour as a source of potential output during the forecast period. The growth in labour input supply will also be constrained by the decrease in the working-age population (15–74-year-olds), which has already begun. An exception to the downward trend in the working-age population this year and in 2024 is the higher than expected increase in immigration.

Despite the economic headwinds, the labour force participation rate remains high and will underpin both labour input and potential output. However, the supply of labour input is weakened by employees working fewer hours on average than before. Population ageing is also likely in the future to weaken the prospects for growth in the average number of hours worked.

chart 15.Potential output will grow slowly

In recent years, the economy has been afflicted by several different crises. This gives rise to uncertainty about the future growth potential. The growth potential can alter if permanent changes are perceived in, for example, globalisation, production methods, energy prices, household behaviour or immigration.9 Climate change is also causing uncertainty over the development of the long-term growth potential.10

Russia’s war in Ukraine could have a long-term adverse impact on the prospects for economic growth if it results in a lasting reduction in international trade and leads to a more inefficient global division of labour. This would, in turn, slow the growth in productivity. On the other hand, the growing diversity of critical production chains and efforts to move production closer to the domestic market could lessen the risk of supply-side disruptions.

The development of the capital stock will be affected by two opposing forces. On the one hand, the reorganisation of production and the potentially huge investment in the green transition would strengthen the capital stock, but, on the other hand, the cancellation or postponement of potential investments due to the war in the short term would hamper any increase in the capital stock.11 Some of the capital stock could, moreover, become obsolete if, in the future, there are major disruptions to the availability of oil and gas or the price of energy remains high permanently. Furthermore, the removal of polluting capital stock will weaken the capital stock generally and will require new investment to replace it with something less polluting.

There is much uncertainty over the effects of the Ukraine war on labour input, concerning, for example, the numbers of immigrants and how immigrants would find employment. Meanwhile, the increase in working remotely, which has resulted from recent crises, may boost the labour supply in the economy if greater flexibility means that economically inactive people start to enter the labour market more than before. The increase in the supply of labour would then strengthen potential output.

Prices and wages

Inflation has slowed considerably in 2023 and will remain moderate during the forecast period 2024–2026. The decline in the prices of energy and other production inputs continues to pass through to consumer prices. Due to the tightening of monetary policy and the weak economy, price pressures will continue to be minor, especially in 2024. However, continued brisk growth in earnings will maintain services inflation. Underlying inflation will slow gradually, as nominal earnings growth slows during the forecast period from the high figures of 2023. Finland’s cost competitiveness will weaken relative to the euro area in 2023, but the lost ground will be recovered in 2024–2026.

Period of high inflation is over

Inflation has slowed substantially in 2023 (Chart 16). Energy prices have come down from the high figures of 2022, and both import and producer prices have started to decrease. The supply bottlenecks which pushed up prices in recent years have disappeared. Their rapid disappearance and the weakening of demand has resulted in oversupply in many consumer goods, which has a slowing effect on inflation.

The tightening of monetary policy and the weak economic conditions are bringing down inflation, which will be at around 1% in 2024 measured using the Harmonised Index of Consumer Prices (HICP). Consumer prices for energy will continue to decline compared with 2023. Weak global demand expectations for crude oil and increased supply are pointing to a downward path for crude oil futures prices, in addition to which in Finland, the decrease in fuel taxes at the beginning of 2024 will reduce petrol prices. However, the uncertainty surrounding energy prices is exceptionally high (see risk assessment). Lower energy prices also reduce upward pressure on food prices. In addition, the import and producer prices of food have started to decrease in 2023. As a whole, the rise in food prices will slow substantially according to the forecast, and the prices of unprocessed food will even decrease slightly in 2024. Underlying inflation, which measures price changes in consumer goods and services, will slow down in 2024, but wage increases and rising rents will keep services inflation higher than usual.

HICP inflation will rise slightly in 2025–2026, when economic conditions start to improve again and the effects of monetary policy begin to diminish. The fall in energy prices will level off and the rise in food prices will return to conventional levels. Underlying inflation will slow to below 2% in 2025, because services inflation will fall due to slower earnings growth.

chart 16.Inflation will be below 2% in 2024–2026

Earnings growth will continue in the coming years

The growth in nominal earnings, as measured by the index of wage and salary earnings, has picked up markedly in 2023, because in addition to negotiated pay increases, lump sum payments have raised earnings (Chart 17). The growth in nominal earnings will slow down in 2024 in accordance with collective agreements already in force. In the latter part of the forecast period, the increase will slow further to around 2.5%. The preparation of the forecast employed an assumption that is based on a long-term observed correlation suggesting that the pace of long-term growth in real wages will be broadly the same as growth in productivity.

The price of labour, measured in terms of compensation per employee, will rise by around 4% in 2023, but by less in 2024. This is due to both slowing earnings growth and a reduction in unemployment insurance contributions paid by employers. Towards the end of the forecast period, the price of labour will rise at a rate of slightly under 3%, which is around the same rate as other earnings indicators.

chart 17.Robust growth in earnings in the immediate years ahead

Finland’s cost competitiveness can be assessed by comparing the rise in unit labour costs, adjusted for the terms of trade, to the rest of the euro area (Chart 18). Cost competitiveness in relation to the euro area will weaken in 2023, but in 2024–2026 it will improve again. However, the favourable development in cost competitiveness is mainly the result of slower earnings growth than in the other euro area countries.

chart 18.Finland’s cost competitiveness in relation to the euro area

Risk assessment

The risks surrounding the growth forecast for the Finnish economy are predominantly on the downside. However, in the inflation forecast, the upside and downside risks are balanced.

There is continued uncertainty surrounding the growth outlook in Finland’s export markets. If high core inflation were to be prolonged, it would restrain growth in the euro area economy, as interest rates in the euro area would remain high for longer than anticipated. There is currently considerable variation in interest rate expectations, and there are both upside and downside risks in regard to the interest rate path.

The wars in Ukraine and the Middle East are causing uncertainty, which could be reflected in the prices of raw materials and energy. Furthermore, geopolitical tensions between the United States and China, for instance, could cause disruptions to international supply chains and global trade. If Russia’s hybrid operations in Finland continue, this could cause general uncertainty in households and companies.

In Finland, the labour market trend is the largest source of uncertainty. Although economic growth has slowed down, households’ purchasing power has so far still been supported by the strong employment situation. However, the sharp decline in housing construction in 2023 and 2024 may lead to more job losses than projected. There are also risks concerning employment in other industries. So far, labour needs in manufacturing have been adjusted through temporary lay-offs, but if the recession is prolonged, the lay-offs will turn into redundancies before long.

According to Statistics Finland’s consumer confidence indicator, the confidence of households in both Finland’s economy and their own finances has remained weak during the autumn. However, the weak confidence might not yet be fully reflected in private consumption and could cause this to slow down during the early part of 2024, following a time lag.

On the financial markets, the biggest risks are associated with the housing market. The decline in residential property prices combined with tightening financing conditions increases the risks for real estate investment funds. These companies are often highly indebted, and their investment portfolios are illiquid. Materialisation of the risks of real estate funds would cause even greater uncertainty on the financial markets.

During the forecast period, central government finances will be consolidated and reforms implemented on the labour market. However, the impacts of these measures on economic growth and employment during the forecast period are difficult to predict. Cuts to unemployment benefits and social security could reduce private consumption by more than anticipated. The current recession adds to the uncertainty when assessing the employment impact of the labour market reforms.

There are both upside and downside risks with respect to inflation in Finland. Energy prices have fluctuated sharply in recent months, and prices could still change in either direction. The increase in the rents of subsidised rental housing will drive up services inflation in 2024. The private rental market could also be subject to upward pressure on rents, as a decline in demand for owner-occupied housing will increase the demand for rental housing. Price pressure from import prices will depend especially on developments in the euro area economy.

It is also possible that there could be unexpected favourable developments in the Finnish economy in the immediate years ahead. Growth in Finland’s export markets, especially in advanced economies outside Europe, could also provide a positive surprise.

As interest rates begin to fall and the economy recovers, private investment could increase by more than forecast. Especially in residential construction, a change for the better could come sooner than expected, as at the end of the forecast period, there could be pent-up demand for new homes following the slump in construction. Investment in the energy sector could pick up, especially in the latter part of the forecast period, due to an acceleration in the green transition both in Finland and in its export markets.

Notes

-

More detailed information on the euro area forecast is available on the ECB website. ↑

-

More detailed information on the ECB’s monetary policy decisions is available on the ECB website. ↑

-

Value of private investment relative to the value of GDP. ↑

-

The Government is seeking permanent expenditure savings totalling EUR 4 billion by 2027. The Bank of Finland’s forecast takes into account about 60% of this total, because of the uncertainty associated with the implementation of the remaining measures and with the magnitude of their estimated impact. ↑

-

Finland’s public finances, the various measures of the new and previous Governments and the fiscal consolidation needs are analysed in more detail in the Bank of Finland’s assessment of public finances (December 2023). ↑

-

The HX Fighter Programme will cause timing differences as the Government front-loads the payment of the fighter procurement, which will initially increase public debt. However, the overall impact on debt growth will ultimately be roughly equal to the procurement price. In addition, interest subsidised loans (ARA loans) also increase the estimated level of public debt (and, at the same time and by exactly the same amount, the level of public financial assets). ARA loans are permanent debt shown in the statistics for technical reasons. ↑

-

Potential output is the volume of GDP when all the inputs in the economy are in normal use. The output gap describes the difference between the economy’s actual and potential GDP. When actual and potential GDP are at the same level and are growing at the same rate, the output gap is zero and the economic cycle is said to be neutral. ↑

-

Higher and more volatile prices of energy may weaken potential output via many channels. See, for example, the projections in Deutsche Bundesbank (2022b) Impact of permanently higher energy costs on German potential output, Monthly Report, December 2022, pp. 29. https://www.bundesbank.de/resource/blob/814804/cff13526d6379180bd93e8a935657592/mL/2022-12-monatsbericht-data.pdf ) and ECB Economic Bulletin 5/2022, Box 4 https://www.ecb.europa.eu/pub/economic-bulletin/focus/2022/html/ecb.ebbox202205_04~f296647c4b.en.html ). ↑

-

European Commission’s Spring 2023 Economic Forecast, special issue (https://ec.europa.eu/economy_finance/forecasts/2023/spring/SpecialIssue-Medium-term_projections.pdf). ↑

-

See the ECB’s article on the impacts of climate change on potential output (How climate change affects potential output), ECB Economic Bulletin, Issue 6/2023, https://www.ecb.europa.eu/pub/economic-bulletin/articles/2023/html/ecb.ebart202306_02~0535282388.en.html). ↑

-

Greater uncertainty and the high cost of energy, for example, will discourage investors. ↑