Editorial

Subdued outlook for Finnish economy – Solutions required to long-term challenges

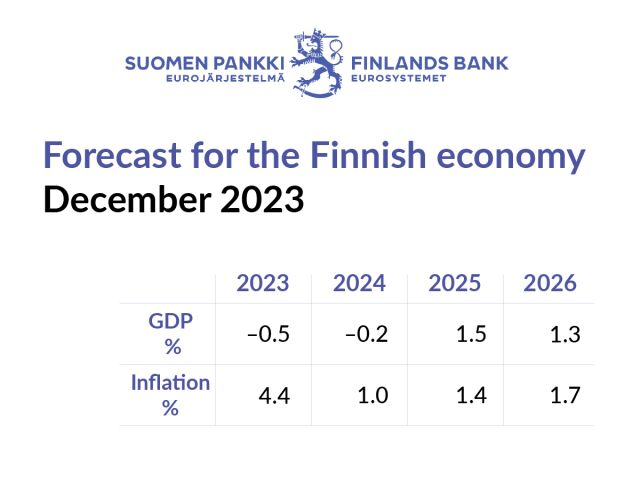

The operating environment outside Finland has become difficult, and the outlook for the economy continued to deteriorate during the autumn. Finland’s economy is in recession and will continue to be weak across a broad front in 2024. Bringing the public finances onto a different path is proving more challenging than expected, due to the weak economy.

The economy will start to slowly pick up from the end of 2024, supported by lower interest rates and by growth in Finland’s export markets. Households’ purchasing power is improving as inflation slows rapidly, in line with monetary policy objectives.

The Governing Council of the European Central Bank (ECB) has been tightening monetary policy since December 2021 in order to return inflation to the 2% medium-term target following its rapid surge. The ECB Governing Council began to raise its key interest rates in July 2022 and has raised them by a total of 4.5 percentage points. It has kept the key interest rates unchanged since September.

The ECB’s monetary policy is conducted for the entire euro area, and the main target variable in this is euro area inflation. Price stability will support durable economic growth and employment in the euro area, which is in Finland’s interests as well.

Monetary policy tightening slows down demand growth and thus, through a number of channels, curbs inflation. When interest rates rise, this encourages saving and reduces consumer spending and investment. By raising key interest rates, the ECB also seeks to manage inflation expectations, which are important for future price developments as expectations affect pricing by companies and the wage demands of employees.

Monetary policy tightening has slowed economic growth and inflation across the entire euro area. Although the transmission channels are largely common among the economies of the euro area, there are differences in the transmission of monetary policy due to differences in economic structure between these countries. The rapid tightening of monetary policy has therefore led to a debate on the strength and speed of monetary policy transmission in the euro area economies.

The pace of monetary policy transmission to the Finnish economy has been rapid. Finnish mortgages are mainly variable rate loans, and so the rise in interest rates has rapidly increased loan servicing costs for Finnish households. However, this only makes a small contribution to the strength of monetary policy effects in Finland. About 30% of Finnish households have a mortgage, and a majority of these are high-income households. These households have a financial margin that they can use to cope with increased loan servicing costs and to smooth consumption over time.

Other structures of the Finnish economy also affect the transmission of monetary policy. Finland’s industrial structure is more heavily weighted towards manufacturing and construction, which increases the economy’s interest rate sensitivity. In addition, the geographical location of Finland and the composition of its foreign trade weaken the position of its economy. Imports of raw materials and intermediate goods important to Finland have become more difficult and expensive due to the situation with Russia. Among Finland’s largest export destinations, the economies of both Germany and Sweden are now weaker than average. The impact of these factors and the overall effect on economic growth of having a similar monetary policy for all countries are clearly more important than the extent to which interest rates are variable or fixed among the loan stock.

The financial markets expect current interest rates to stabilise and start to decline during 2024. The monetary policy tightening carried out thus far is not expected to have any further adverse impacts on growth in the Finnish economy after 2024. Due to the high proportion of variable rate loans, the fall in interest rates means that household loan servicing costs in Finland are also beginning to decrease faster than the euro area average.

The Bank of Finland’s annual assessment of the public finances is now gloomier than it was a year ago. On the basis of the available data, Finland’s public debt-to-GDP ratio will rise to over 80% by 2026. The Bank’s assessment of the sustainability gap, which corresponds to an immediate adjustment that would stabilise the debt ratio in the long term, has also increased to 4.5% of GDP.

The concern about public debt in Finland relates above all to the projected growth in this debt. The European Commission and the Eurogroup have also drawn attention to this issue in the EU’s multilateral economic and fiscal monitoring.

Between 2008 and 2022, the ratio of Finland’s public expenditure to GDP grew by 5.4 percentage points, but revenue by only 0.5 percentage points. Public spending is subject not only to pressure from the long foreseen rise in age-related expenditure but also from expenditure on defence and other contingency preparations. In addition, a parliamentary commitment has been made to increase public R&D funding in order to strengthen the conditions for economic growth. With all this in mind, stabilising the debt ratio will be an extremely demanding task.

Carefully targeted expenditure cuts are necessary, but other reformative measures are also needed. The overall picture is difficult because spending cuts or tax increases have their opponents and structural reforms are no easier. Structural reforms also create winners and losers. Moreover, their economic impact takes time to materialise and its magnitude is not easy to assess reliably.

It is good that the Government Programme sets out the aim of strengthening Finland’s public finances. However, present forecasts suggest that the growth in the general government debt ratio will continue.

Debt sustainability must be taken as a common economic policy priority and a firm commitment made to ensuring this across parliamentary terms. The ways in which this can be achieved and the emphasis placed on the different measures will always involve political judgement. However, it is important that fiscal consolidation measures are targeted in a way that minimises adverse effects on short-term growth and supports long-term growth.

The outlook for long-term growth in Finland’s economy is hampered by the ageing of the population, poor productivity performance, a halt in the growth of educational attainment and a deterioration in learning outcomes. Reforms to increase the total labour input in the economy remain necessary. Since the early 2000s, employment in Finland has been supported by a trend rise in the labour force participation rate of older workers and by reforms undertaken, among other things. As these favourable trends weaken, new measures to boost the labour supply will become increasingly important.

Investment in education and training and in research and innovation is also essential.

It is important for a small open economy such as Finland’s to be actively involved in international cooperation related to technological development and to be able to make effective use of innovations produced elsewhere. Work-based and education-based immigration will also help support this objective.

The innovation, research and development that lead to investment in new technologies will not be possible without an appropriately educated workforce. Skilled workers will also be needed to ensure new ideas and practices are taken up on a large scale. Universities will play a key role, as they generate not only human capital but also research and innovation.

The Government can best promote innovations and their adoption by creating an appropriate environment for individuals and companies. Instead of pursuing quick gains, the aim should be to build a long-term foundation for new ideas, businesses and activities. The conditions for sustainable economic growth can be safeguarded by a coherent economic policy that supports innovations and their utilisation.

Helsinki, 19 December 2023

Marja Nykänen

Deputy Governor