Forecast

From shallow recession to moderate growth

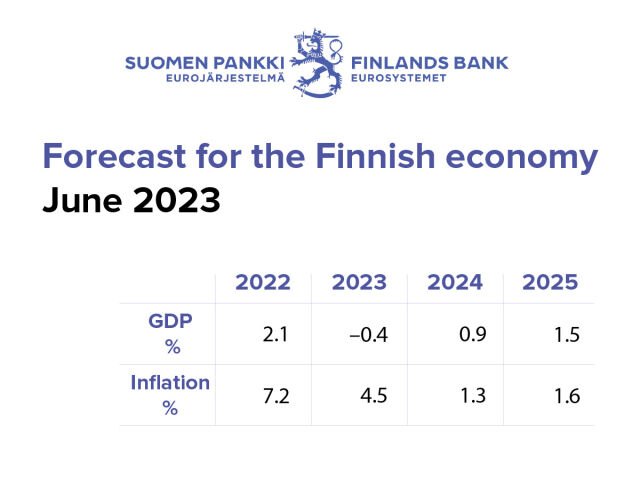

The Finnish economy will contract by 0.4% in 2023 as inflation, tighter monetary policy and weak export demand weigh on growth across a broad front. Inflation is nevertheless falling this year, and this is already improving household purchasing power. As a consequence, economic growth will pick up in 2024, albeit to a modest 0.9%. The rise in interest rates will dampen growth in investment and private consumption in the immediate years ahead. In 2025, growth in the economy will gather pace, reaching 1.5%.

chart 1.Moderate growth in Finnish economy in 2024

Overview

Growth in the global economy will strengthen. Supply-side bottlenecks will ease, China’s economic growth will gain momentum and the labour market will remain robust in many countries. In addition, lower energy prices and receding concerns about energy availability will support growth in the euro area economy. The pace of growth will, however, be curbed by still-too-high inflation and tighter financing conditions. Because of these factors, growth will be weak in the immediate years ahead in Finland’s main export markets and therefore in Finland’s exports. Due to the rapid rise in interest rates, financing conditions have tightened in Finland, too, although banks’ credit standards have not tightened significantly.

The drop in energy prices will bring inflation down significantly this year already. Tighter monetary policy is gradually beginning to bite, and Finland’s inflation will subside next year to 1.3%. However, the level of underlying inflation, measuring price movements in consumer goods and services, will fall only after some delay, as wage increases and rent rises will maintain inflation in service prices. Earnings will rise briskly in the immediate years ahead, and real earnings will grow from 2024 onwards. As inflation slows, this will gradually create more favourable conditions for economic growth.

The trend in the Finnish labour market has so far been particularly favourable, and the labour force participation rate is at a record high. However, weak cyclical conditions will feed through to the labour market during 2023. Consequently, the employment rate will dip, and the unemployment rate will rise. Even though labour shortages will ease on account of cyclical factors, the structural labour shortages in some sectors will remain a problem in Finland. Once economic growth recovers, the labour market will improve again.

Private consumption will rebound this year, due to a brisk rise in nominal earnings and social benefits and an improvement in households’ purchasing power. Year-on-year, however, private consumption will contract slightly from 2022. Some households will be able to cover the rising cost of living by using savings accumulated during the pandemic. In the immediate years ahead, consumption will be boosted by lower inflation, a robust labour market and the rise in employees’ earnings. In the case of indebted households, however, higher interest payments will weaken consumption also in the years to come.

The increase in costs for businesses and the steep rise in interest rates are depressing investment. Residential investment, in particular, will decline dramatically, as rising interest rates and high inflation have stalled the housing market. Non-residential investment will also be hampered by uncertainty over the long-term outlook for growth and the fact that interest rates will still be at elevated levels in 2025. Nevertheless, both residential and non-residential investment will resume growth in 2025, as the cyclical conditions improve and an increasing number of green transition investments are launched.

The general government deficit will deepen in 2023–2025. The public finances are being weakened by high inflation, the need to strengthen the national security of supply, defence procurement projects and higher interest expenditure. Cyclical conditions will no longer support the public finances. The public debt-to-GDP ratio will rise in the forecast period, climbing to over 78% by the end of 2025. The forecast for the public finances coincides with the transition between two parliamentary terms and is based on the assumption of unchanged fiscal policy.

In the short term, strong demand in Finland and elsewhere may boost economic growth and defer the normalisation of inflation. If, because of this, monetary policy were to be tightened more than expected in order to curb inflation, this would, in turn, weaken growth until inflationary pressures abate. Uncertainty surrounding the geopolitical situation and export demand is still high.

| Percentage change on the previous year | |||||

|---|---|---|---|---|---|

| 2021 | 2022 | 2023f | 2024f | 2025f | |

| GDP | 3.0 | 2.1 | -0.4 | 0.9 | 1.5 |

| Private consumption | 3.6 | 2.0 | -0.4 | 0.8 | 1.1 |

| Public consumption | 3.9 | 2.9 | 2.6 | 1.1 | 0.4 |

| Fixed investment | 0.9 | 5.0 | -5.5 | 0.1 | 4.6 |

| Private fixed investment | 4.1 | 6.1 | -5.8 | -1.3 | 2.6 |

| Public fixed investment | -11.8 | -0.0 | -3.9 | 6.9 | 13.9 |

| Exports | 6.0 | 1.7 | 0.1 | 2.4 | 2.8 |

| Imports | 6.0 | 7.5 | -3.0 | 1.9 | 3.3 |

| Effect of demand components on growth | |||||

| Domestic demand | 3.0 | 2.9 | -0.9 | 0.7 | 1.5 |

| Net exports | -0.0 | -2.3 | 1.5 | 0.2 | -0.2 |

| Changes in inventories and statistical error | 0.0 | 1.5 | -1.0 | 0.1 | 0.0 |

| Savings rate, households, % | 2.5 | -1.6 | -1.8 | -0.0 | 0.6 |

| Current account, %, in proportion to GDP | 0.5 | -3.9 | -1.6 | -0.9 | -1.0 |

| 2021 | 2022 | 2023f | 2024f | 2025f | |

|---|---|---|---|---|---|

| Labour market | |||||

| Number of hours worked | 2.4 | 0.6 | 0.3 | 0.4 | 0.5 |

| Employment rate (20–64-year-olds), % | 76.5 | 78.1 | 78.0 | 78.2 | 78.5 |

| Unemployment rate, % | 7.6 | 6.8 | 7.2 | 7.1 | 7.0 |

| Unit labour costs | 3.1 | 3.7 | 5.4 | 2.5 | 1.6 |

| Labour compensation per employee | 3.6 | 3.1 | 4.9 | 3.2 | 2.8 |

| Productivity per employee | 0.5 | -0.6 | -0.5 | 0.8 | 1.2 |

| GDP, price index | 2.1 | 4.3 | 5.5 | 1.9 | 1.8 |

| Private consumption, price index | 1.8 | 5.5 | 6.2 | 1.4 | 1.1 |

| Harmonised index of consumer prices | 2.1 | 7.2 | 4.5 | 1.3 | 1.6 |

| Excl. energy | 1.3 | 4.8 | 5.1 | 2.1 | 2.0 |

| Energy | 9.7 | 31.0 | -1.3 | -6.1 | -3.3 |

| General government, % of GDP | |||||

| General government balance | -2.7 | -0.8 | -2.2 | -2.9 | -3.6 |

| General government gross debt (EDP) | 72.6 | 73.0 | 73.2 | 76.0 | 78.3 |

| f = forecast. | |||||

| Sources: ECB and Bank of Finland. |

Operating environment: assumptions and financing conditions

World trade growth was subdued in early 2023. However, it will pick up as supply disruptions ease, and this will gradually begin to boost demand for Finland’s exports. Tighter financing conditions are dampening growth in both the euro area and the global economy this year and in 2024, but growth will start to gradually pick up as inflation falls in response to the tighter monetary policy. The rapid rise in market rates will tighten financing conditions in Finland as well. The Bank of Finland’s forecast is based on the data available on 31 May 2023.

Decline in inflation will support growth in the global economy

The global economy has been supported by the post-pandemic opening up of China’s economy and the strong labour market in many countries, but global economic activity waned towards the summer. Confidence figures have been weak, especially in manufacturing. Moreover, uncertainty has increased due to banking sector concerns in the United States in particular, although the greatest unease has recently diminished. The tightening of financing conditions in both the euro area and the United States will adversely affect growth in the global economy this year and in 2024. However, growth in the global economy is being steadily underpinned by the slowing of inflation worldwide as a delayed response to tighter monetary policy. The global economy is currently facing both upside and downside risks (see Risk assessment).

World trade growth is slowing this year (Table 2). In the last few quarters, world trade has contracted due to the weak performance of the goods trade, as demand growth has focused more on services with the fading of pandemic concerns (Chart 2). Growth in Finland’s main export markets will be faint this year. However, global supply disruptions will further ease, and so, when the world economy returns to growth, the conditions will be favourable for export market growth in the years ahead.

chart 2.Finland’s export demand will grow slowly this year

Energy prices fell during the first half of 2023 and energy supply concerns in Europe have eased, at least for now, thereby supporting growth. The moderation of energy prices is also lowering production costs and slowing inflation worldwide. The forecast assumes that oil prices will decline moderately, in line with market expectations (Table 2). Based on market expectations, prices of other raw materials will fall slightly this year, but remain almost unchanged after that.

GDP growth in the euro area economy for the full year 2023 will be restrained by the weak growth that occurred at the start of the year (Table 2).1 High inflation and tight financing conditions dampened private consumption early in the year. In the coming quarters, euro area GDP growth will be supported by strong labour markets, improved real purchasing power, moderated energy prices, reduced uncertainty and the easing of supply-side bottlenecks. Curbing euro area growth in 2023 and 2024, however, is the tightening of monetary policy.

Euro area inflation has been more persistent than previously estimated. However, consumer price inflation is expected to slow as energy prices fall and the rise in food prices eases. If energy and food prices are removed, the underlying level of inflation is falling only gradually. The rise in wages is a principal reason for the persistence of underlying inflation in the euro area.

Rapidly rising interest rates are tightening financing conditions

In June 2023, the Governing Council of the European Central Bank (ECB) decided to raise the key ECB interest rates by a further 25 basis points in its continued efforts to curb inflation.2 Inflation is coming down, but projections indicate this is happening too slowly. By raising interest rates, the Governing Council is determined to ensure that inflation returns to its 2% medium-term target in a timely manner. The interest rate on the main refinancing operations is now 4.00%, the marginal lending facility rate 4.25% and the deposit facility rate 3.50%. The Governing Council also confirmed that it will no longer reinvest the principal payments from maturing securities under the Asset Purchase Programme (APP) after June.

The exceptionally rapid rise in market rates has tightened financing conditions significantly. The financial markets expect the 3-month Euribor to remain above 3% this year and in 2024 (Table 2). The rise in interest rates has also been reflected in the average interest rates on new loans, as there has been a strong increase in the interest rates on new loans to enterprises and on new housing loans (Chart 3). In Finland, the majority of housing loans are tied to the 12-month Euribor, which means that based on market expectations, the interest rate on most housing loans will rise to over 3% during the course of this year. Like housing loans, the average interest rate on corporate loans has already increased significantly.

According to the Bank Lending Survey, Finnish banks have not extensively tightened their credit standards and terms and conditions. The credit standards for corporate loans have remained unchanged for the last two quarters and the tightening of credit standards for housing loans has not been widespread. Moreover, in the Business Tendency Survey released by the Confederation of Finnish Industries in April, companies did not report significant financing difficulties.

| Volume change year-on-year, % | |||||

|---|---|---|---|---|---|

| 2021 | 2022 | 2023f | 2024f | 2025f | |

| Euro area GDP | 5.3 | 3.5 | 0.9 | 1.5 | 1.6 |

| World GDP (excl. euro area) | 6.7 | 3.3 | 3.1 | 3.1 | 3.3 |

| World trade* (excl. euro area) | 12.9 | 5.3 | 1.3 | 3.4 | 3.4 |

| 2021 | 2022 | 2023f | 2024f | 2025f | |

| Finland’s export markets**, % change | 10.9 | 6.0 | 1.0 | 3.1 | 3.1 |

| Oil price, USD/barrel*** | 71.1 | 103.7 | 78.0 | 72.6 | 70.4 |

| Export prices of Finland’s competitors, EUR, % change | 9.9 | 19.0 | -1.9 | 2.4 | 2.3 |

| 3-month Euribor, %*** | -0.5 | 0.3 | 3.4 | 3.4 | 2.9 |

| Finland’s nominal effective exchange rate**** | 109.4 | 106.6 | 109.6 | 109.8 | 109.8 |

| USD value of one euro***** | 1.18 | 1.05 | 1.08 | 1.09 | 1.09 |

| * Calculated as the weighted average of imports. | |||||

| ** The growth in Finland’s export markets is the import growth in the countries Finland exports to, weighted by their average share of Finland’s exports. | |||||

| *** Technical assumption derived from market expectations. | |||||

| **** Broad nominal effective exchange rate, 2015 = 100. The index rises as the exchange rate appreciates. | |||||

| ***** Assuming no changes in the exchange rate. | |||||

| f = forecast. | |||||

| Sources: ECB and Bank of Finland. |

chart 3.Average interest rates on new loans are rising ste

Demand and the public finances

Demand growth for the full year 2023 will be weak. Inflation is eroding growth in the purchasing power of Finnish households. High interest rates and uncertainty will dampen investment throughout the forecast period. The falling level of inflation will gradually improve purchasing power and revive household consumption. There will also be a gradual recovery in exports, driven by growth in Finland’s export markets. The increase in exports will nevertheless lag behind the growth in export markets. Finland’s public finances will remain in deficit throughout the forecast period.

chart 4.Economic recession to remain short-lived

Household purchasing power will improve

Household purchasing power and real income will start to recover this year. The rise in consumer prices is slowing, and the increase in households’ nominal income will be brisk on account of larger than usual pay rises and index-linked increases in social benefits. To some extent, households will be able to cover increased living costs by using their savings, which will mean that the savings rate will be clearly negative this year as well. Private consumption will start to increase during the course of the year, although for 2023 as a whole it will be slightly lower than in 2022 (Chart 5).

chart 5.Inflation will consume households’ nominal income growth in 2023

In addition to the rise in earnings, an improved employment situation will cause household income to increase next year. Private consumption will continue to recover in 2024, and this growth will continue in 2025 (Chart 5). Household income will nevertheless increase faster than consumption, which will rebalance the savings rate. Private consumption growth will, in turn, be slowed by interest rates, which will remain elevated in the immediate years ahead.

The rise in interest rates means that a larger share of household income is being used to service loans. The rise in market rates seen already will continue to be felt in lending rates to households as reference rates are revised. The increase in interest rates is nevertheless burdening households unevenly (see Savings help households cope with rising interest rates). Around half of households have no debts at all. It is the high-income and wealthiest households that have the biggest debts, both in absolute terms and in relation to income. Although the rise in interest rates may cause difficulties for individual households, the interest rate burden mainly affects middle and high-income earners. This somewhat dampens the adverse impact of higher interest payments on private consumption.

Rise in interest rates is curbing investment

Private investment increased rapidly in 2022, with sharp growth in housing construction and non-residential investment. Investment grew to euro-era record levels. The substantial increase in the volume of investment in 2022 also boosted the investment ratio, which had remained static for so long (Chart 6).

Non-residential investment last year was boosted especially by investment in industry. Investment in the green transition, and in energy production in particular, was bolstered by a range of wind power construction projects, among other things. The favourable economic conditions for housing construction continued in 2022, with considerable activity in apartment block construction. In recent years there has been a substantial amount of housing construction in Finland, by international standards, too.

The rapid rise in interest rates, however, is turning this trend around in 2023. Furthermore, companies have seen their costs soar, and this is making them more reluctant to invest. Housing construction will decrease substantially in 2023, and this will inevitably be followed by a period of far fewer housing construction projects.

The numbers of residential building permits and new starts have seen a sharp decline for almost a year now, and this will be evident as a considerable decrease in residential investment this year. The rise in mortgage interest rates is making households less likely to take out loans and is therefore weakening the demand for housing. The tightening of monetary policy and the weak economic outlook will also slow the growth in non-residential investment. Private investment is projected to decrease by almost 6% in 2023.

chart 6.Investment ratio falling

Overall, the trend in private investment looks very weak over the entire forecast period (Chart 7). The markets do not expect interest rates to come down significantly from their current levels, and there is still much uncertainty about the economic outlook. Likewise, investment in the next few years will be subdued on account of the rapid rise in the costs of borrowing that businesses face, and due to smaller profit margins. In addition, the capacity utilisation rate has fallen and points to adverse cyclical conditions.

Investment will decrease further in 2024 by a little over 1%, but will start to pick up gradually again in 2025, when it will increase by approximately 2.5%. The increase will be supported especially by the planned investment projects associated with the green transition. Investment in the green transition on a large scale poses a significantly expanding growth risk for investment. The low level of investment growth will also mean a fall in the investment ratio in the years ahead.

chart 7.Investment outlook weakening significantly

Export growth will lag behind the growth in export markets

For several years now, Finland’s exports of goods and services have not kept up with the growth in export markets. Exports rose in 2022, but at a significantly slower rate than the growth in export markets. The increase in exports was attributable in part to the export of services, which increased rapidly as a result of the post-pandemic increase in demand for travel and business-related services, for example. The increase in goods exports, on the other hand, was fairly modest. Net exports also remained very weak on account of the strong increase in imports.

The forecast suggests that export growth will come to a halt in 2023 and subsequently trail behind the growth in export markets. This slowing of export growth is a result of the rapid rise in interest rates and the weakening economic situation in the main export markets. Finnish exports are centred mainly on capital goods and intermediate goods and are very dependent on the global economic outlook, while investment is sensitive to changes in interest rates and uncertainty.

The collapse in trade with Russia as a result of the war in Ukraine will weaken goods exports in the years to come, as it takes time to find new markets to replace the trade with Russia. Moreover, the reduction in tourism from the east will have an adverse effect on Finland’s services exports in the future.

Export growth will gradually recover as from 2024, in the wake of growth in the export markets. The demand for Finnish exports will increase when investment starts to pick up in Finland’s main export markets. In 2024, exports will increase by just over 2%, to rise further in 2025 to almost 3%, close to the growth rate of the export markets. There will therefore be losses in the market shares of exports over the entire forecast period, but to a decreasing extent (Chart 8). The effect of net exports on economic growth in Finland will be positive on average in the period 2023–2025, as sluggish domestic demand will, at the same time, weaken the growth in imports.

chart 8.Export growth slowing

The current account deficit widened in 2022 to a euro-era high (Chart 9). The main reason for this was the growing imbalance of the service account, because of factors such as the growth in imports of travel and business-related services. There was also a goods trade deficit. The current account deficit will narrow in the forecast period as export growth picks up. However, the current account will remain in deficit at around 1% of GDP in 2025, as the growth in imports accelerates due to public sector defence procurement.

chart 9.Current account will remain in deficit

Public expenditure will increase faster than revenue

The public finances will remain in deficit. Public expenditure will increase due to spending on strengthening the national security of supply and defence equipment procurement, as well as the rising costs of social benefits and higher interest payments. Expenditure will increase faster than revenue. General government net lending relative to GDP will weaken to -2.2% in 2023 (Chart 10).3 The structural deficit4 in the public finances will widen to 1.6% in 2023.

The increase in tax revenue has been attributable to the growing level of aggregate wages and the value of private consumption, which will continue to increase rapidly in 2023. In the future, the increase in taxes accrued from personal income tax and corporate tax will level off, following a couple of years of intense growth. Additionally, the revenue from indirect taxes other than VAT relative to GDP will fall further.

chart 10.Inflation, contingency planning and interest payments will all weaken public finances

The pay increases of those employed by the state, the municipalities and the wellbeing services counties and the rise in the prices for consumption of intermediate goods will accelerate the increase in public final consumption expenditure. The volume of public final consumption expenditure will grow in 2023 by around 2.5%. This increase will slow gradually to less than 0.5% in 2025. The volume of public investment, on the other hand, will fall by 4% in 2023, before investment starts to increase once again in 2024.5 In 2025, this will leap upwards as a result of defence procurement concerning ships and fighter aircraft.

The central government deficit in particular will increase. Central government expenditure will increase partly due to the additional expenditure on security and R&D financing. The interest payments of central government will also rise in the forecast period every year by approximately 0.3 percentage points relative to GDP.

Local government’s net borrowing will also increase in 2023. There was a historic change in the public finances at the start of 2023, when the wellbeing services counties, which are part of local government, came into existence. With this reform, central government tax revenue, and also current transfers from central to local government, increase substantially. At the start of their operations, the wellbeing services counties will be in deficit.

In 2023, the rise in consumer prices is pushing up index-linked social benefits faster than in any year since 2009. This considerable increase in index-linked benefit expenditure will also continue in 2024. The financial position of earnings-related pension providers is nevertheless balanced in part by interest income, which has been increasing as interest rates have risen. Unemployment expenditure will rise in 2023 with the increase in the number of unemployed people, but the other social security funds will nevertheless remain in surplus.

The general government debt-to-GDP ratio will rise very slightly in 2023, compared to 2022 (Chart 11). The rise in the debt ratio is being curbed by the rapid rise in nominal GDP due to high inflation. From 2024 onwards, the deficit will again begin to increase the debt ratio rapidly. The amount of debt will also rise with the procurement of defence equipment, among other things. The debt ratio will increase to more than 78% by the end of 2025.

chart 11.Government debt ratio starts to increase again

Supply and cyclical conditions

Finland’s GDP growth in 2023 will slow to below the growth potential, and the economy will be in mild recession. The buoyancy in the labour market will take a step back due to the cyclical conditions. When the economic headwinds ease, employment growth will return and the economy will start approaching a more balanced position. In 2025, GDP is forecast to increase close to its longer term growth potential, and the output gap will have almost closed.6

Labour market buoyancy takes step back

The labour market continued to be strong in the early part of 2023, despite the economic downturn and labour shortages (Chart 12). Employment growth has been boosted by the demand for labour-intensive services, and the number of jobs has risen in manufacturing as well. The employment rate is at an all-time high, while the level of unemployment has fallen to just below the structural unemployment rate. The decrease in unemployment is less than the increase in employment, but this is explained by the substantial rise in the labour force participation rate.

chart 12.Slowdown in employment growth will only be temporary

The number of hours worked per employee has fallen, which in turn has increased the need for recruitment. The large number of job vacancies and the high labour shortage indicators reflect the difficulties in recruiting skilled employees in many sectors (Chart 13). A large number of jobs have been created, however, so the labour market has functioned relatively well despite the problems of the skills mismatch.

chart 13.Peak labour shortage now passed

The weakening economy will be felt in the labour market during the first half of the forecast period, when the decline in purchasing power will dampen private consumption and the demand for services. Weaker expectations for employment, fewer job vacancies and the labour shortage indicators all suggest that the labour market will be cooling. The rise in the employment rate will end in 2023 and the unemployment rate will increase by just under half a percentage point to 7.2%.

The cooling of the labour market will nevertheless mean that recruitment problems will ease somewhat. The demand for labour will be underpinned by the fall in real wages and the accumulated financial buffers of companies. Although the shortage of labour will ease with the economic cycle, the structural labour shortage will remain a problem in many sectors that are not cyclically sensitive, such as healthcare and care for older people. This is due to Finland’s ageing population, so it can be expected to slow employment growth across economic cycles.

Towards the end of the forecast period, employment will improve again, due to greater purchasing power and the recovery of private consumption, among other things. The employment rate will reach 78.5% in 2025, and at that time there will be approximately 15,000 more people in work than on average in 2022. The growth in employment will be restricted by the record high participation rate, which cannot in future be expected to ease labour market tightness or fuel the growth in employment significantly without new structural measures. In 2025, the unemployment rate will decrease to 7.0%. The unemployment rate at the end of the forecast period will be below its structural level, which will restrict growth in employment.

Finnish economy enters mild recession

The Finnish economy had largely recovered from the deep recession caused by the COVID-19 pandemic when the next crises came unexpectedly. GDP growth will slow in 2023 to below the economy’s growth potential, and the output gap will be negative (Chart 14). As a consequence, the Finnish economy is in mild recession in 2023. In 2025, the economy will be in a more balanced position, with the output gap near zero and GDP growth close to its potential figure.

chart 14.Output gap in Finland

The growth in potential output in Finland will continue to be slow across the forecast period, rising at a rate of just over 1% a year on average (Chart 15). This slow growth in potential output will be due to the weak trend in investment and capital stock. The growth in total factor productivity will be temporarily subdued, owing to the ongoing reallocation of resources, among other things. Global tensions could weaken total factor productivity by causing some companies to look for new subcontractors, reorganise production chains and try to secure the uninterrupted availability of energy.

Structural rigidities and frictions in the economy play an important role in how quickly and effectively economic resources are reallocated and potential output improves. A high structural unemployment rate will undermine the production significance of labour inputs in the forecast period. Furthermore, any increase in the labour input supply will be limited by the fact that the number of people aged 15 to 74 has begun to decline. On the other hand, and despite the economic headwinds, the participation rate remains strong and will boost labour input and potential output.

chart 15.Potential output will grow slowly

In recent years, several different crises have afflicted the economy. This gives rise to uncertainty about the future growth potential. The growth potential can alter if permanent changes are perceived in, for example, globalisation, production methods, household behaviour or immigration.7

Russia’s invasion of Ukraine could affect the output potential in many ways. The war could have a long-term, or even permanent, adverse impact on the prospects for economic growth if it results in a lasting reduction in international trade and leads to a more inefficient global division of labour. This would, in turn, slow the growth in productivity. On the other hand, the growing diversity of critical production chains and efforts to move production closer to the domestic market could lessen the risk of supply-side disruptions and improve the economy’s crisis resilience in the future.

The development of the capital stock will be affected by two opposing forces. On the one hand, the reorganisation of production and the potentially huge investment in the green transition will strengthen the capital stock, but, on the other hand, the withdrawal or postponement of potential investment due to the war in the short term will hamper any increase in the capital stock.8 Some of the capital stock could, moreover, become obsolete if, in the future, there are major disruptions to the availability of oil and gas or the price of energy remains high permanently.9 Furthermore, the removal of polluting capital stock will weaken the capital stock generally, and it will take new investment to replace it with something less polluting.

There is much uncertainty over the effects of the Ukraine war on labour input, concerning, for example, the numbers of immigrants and how immigrants are employed. Meanwhile, the increase in working remotely, which has resulted from recent crises, may boost the labour supply in the economy if greater flexibility means that economically inactive people start to enter the labour market more than before. The increase in the supply of labour would then strengthen potential output.

Prices and wages

Inflation will slow markedly in 2023, due particularly to a decline in the consumer prices for energy, and will remain low in 2024 and 2025. In contrast, the decrease in underlying inflation, which measures price changes in consumer goods and services, will be gradual during the forecast period 2023–2025, settling at around 2% in 2025. Earnings growth will be considerable in the immediate years ahead, and annual growth in real earnings will turn positive in 2024. Finland’s cost competitiveness relative to the euro area will remain virtually unchanged during the forecast period, reflecting the fact that the growth in both labour costs and labour productivity in Finland is slower than the euro area average.

Underlying inflation will slow gradually during the forecast period

Inflation, as measured by the Harmonised Index of Consumer Prices (HICP inflation), slowed in May to 5%. Consumer prices for energy have been on a downward track since the end of 2022, and in May they were at the same level as a year ago. At the same time, underlying inflation, i.e. inflation excluding energy and food prices, slowed in May to 4.4%. The base effects of the strong rise in prices in 2022 have in recent months slowed annual inflation significantly, and this is expected to continue in the current year. The seasonally adjusted monthly rise in prices has also slowed.

Inflation will slow this year to 4.5% (Chart 16), reflecting the decline in energy prices compared with last year. The rise in the consumer prices of food has started to slow in recent months, and this trend will continue as the recent decline in the prices of agricultural inputs and the levelling off of producer prices gradually feed through to consumer prices. At the annual level, food prices will, however, continue to rise notably. Underlying inflation too, will slow with a lag and will still be at 4.3% for 2023. The rise in the import prices of consumer goods has halted and the disruptions in the supply chain have subsided, which is starting to slow the rise in consumer goods prices. The weak trend in consumption demand will also contribute to lower inflation in 2023.

Inflation as measured by the national Consumer Price Index (CPI) will, in the current year, remain significantly higher than HICP inflation, at 5.9%. The difference is due especially to the rise in interest rates on housing loans and consumer credit, which are included directly in the CPI.10 The decline in the prices of new dwellings is narrowing the difference between the two measures of inflation. The rise in interest rates will, however, slow growth in aggregate demand during the forecast period, which in turn will push down inflation.

chart 16.Inflation is slowing in 2023 and underlying inflation will fall gradually

HICP inflation is slowing significantly and will stand at 1.3% in 2024. However, the projection is subject to considerable uncertainty, which is discussed both in the risk assessment and the alternative scenario. Consumer prices for energy will continue to decline, on the basis of the futures prices of electricity and oil. The rise in food prices will continue to slow, and the prices of unprocessed food will even fall slightly. Underlying inflation will slow to 2.4% in 2024. Pay increases and rising rents will sustain services inflation, although this will be lower than in 2023.

Towards the end of the forecast period in 2025, inflation will accelerate to 1.6% when the economic cycle takes an upturn. Energy prices will decline less steeply and the rise in food prices will accelerate again. Underlying inflation will slow towards the end of the forecast period, to close to 2%, due to slower earnings growth, among other things.

Real wages will return to growth in 2024

Earnings growth will be considerable in the immediate years ahead. The collective bargaining agreements made last winter and spring largely determine the developments in nominal earnings for the next two years. Growth in nominal earnings this year is expected to be 4.5%, measured by the index of wage and salary earnings. Going forward, earnings growth will slow gradually in the next few years (Chart 17). The forecast for earnings is based on the collective bargaining agreements and the observation that in the long term, real wages will increase on average at the same rate as labour productivity. Real earnings will start to grow in 2024 on account of the declining level of inflation.

chart 17.Robust growth in nominal earnings in the immediate years ahead

Various measures are providing a similar picture of the trend in earnings in the immediate years ahead. Labour compensation per employee, i.e. the cost of labour, will increase by nearly 5% in 2023. The rate of increase will slow to below 3% towards the end of the forecast period in 2025, as growth in nominal earnings slows and employment improves slightly. The higher cost of labour and decline in labour productivity will, in turn, push up nominal unit labour costs significantly in 2023. In 2024 and 2025, the cost of labour will rise less markedly and labour productivity will return to growth, causing nominal unit labour costs to increase more modestly towards the end of the forecast period.

Finland’s cost competitiveness relative to the euro area, as measured by unit labour costs adjusted for the terms of trade, will remain virtually unchanged in the forecast period (Chart 18). Labour cost growth, on the one hand, and labour productivity growth, on the other, are projected to remain below the euro area average.

chart 18.Finland’s cost competitiveness relative to the euro area will remain unchanged

Risk assessment

The economic outlook for the immediate years ahead faces both upside and downside risks. There is continued uncertainty surrounding the likely growth in Finland’s export markets, especially in Europe. If inflation persists, interest rates are also likely to remain higher than expected over the forecast years, thus dampening growth in the euro area more strongly than anticipated.

The tightening of financing conditions has increased the risk of further disruptions in the international financial system, which could undermine access to financing for businesses and households. Geopolitical risks, in particular Russia’s war in Ukraine, are also adding to the uncertainty in Finland’s external operating environment. For the time being, the biggest problems concerning energy availability have been solved, but there nevertheless remains a possibility of new electricity price peaks in the coming winters, especially if there are demanding weather conditions.

Domestic risks include persistent inflation. According to the baseline forecast, inflation will clearly slow at the end of 2023. However, there is a chance that domestic and international demand will grow by more than expected. This would increase underlying inflation, which measures price changes in consumer goods and services, after some delay. A shortage of skilled labour could intensify the pressure on wages. If inflation starts to rise again in other countries too, financing conditions could tighten more than in the baseline forecast, thus delaying the economy’s return to a more robust growth trajectory (see Core inflation could be higher than anticipated in the immediate years ahead).

The purchasing power of households is being eroded not only by inflation but also by the rise in interest rates. The largest personal loans are mostly held by high-income and relatively wealthy households, and these households are able to smooth their consumption over time. However, in addition to personal housing loans, many households also have a share of housing corporation loans, which account for around one fifth of the total housing loan stock. There is no precise information on the distribution of these housing corporation loans among households. It is possible that fast-rising interest payments and capital charges will force heavily indebted households to reduce their consumption more than expected, which would undermine growth in private consumption as a whole.

The forecast does not include any assumptions regarding the fiscal policies to be pursued during the new parliamentary term, and therefore incorporates no information on the size, schedule or means of any fiscal consolidation. The effects of fiscal and structural policies on economic growth and employment over the forecast period are therefore uncertain.

Finland’s economic growth in the next few years could, on the other hand, also include positive surprises. The green transition is expected to generate major investments in Finland in the energy sector and energy-intensive industries, but investments are currently being held back by various factors, such as high interest rates. As inflation slows and interest rates begin to fall, private investment could increase by significantly more than forecast. Greater investment would also enable better employment growth than projected.

There is also a chance that the growth in demand for Finnish exports will be higher than expected. In advanced economies, growth may be higher than forecast if inflation is brought under control and there is room to ease monetary policy. A faster-than-anticipated recovery in the Chinese economy could also boost world trade.

Notes

-

More detailed information on the euro area forecast is available on the ECB website. ↑

-

More detailed information on the ECB’s monetary policy decisions is available on the ECB website. ↑

-

This forecast for the public finances coincides with the transition between two parliamentary terms and is based on the assumption that fiscal policy will remain unchanged. In other words, only the measures known about and already decided that affect public revenue and expenditure were considered when this projection was prepared, in addition to the economic forecast. ↑

-

A structural examination corrects the cyclical effect on public revenue and expenditure. ↑

-

The forecasts for public final consumption expenditure and public investment aim to take account of the assessment by Statistics Finland of the impact of the Finnish Government's defence equipment aid to Ukraine. Because this assessment may need to be adjusted, and because of the commencement of reporting by the wellbeing services counties, there is more uncertainty than usual associated with the forecast for public demand. ↑

-

Potential output is defined as the volume of GDP at which all of the economy’s factors of production are fully and efficiently utilised. The output gap describes the difference between the economy’s potential GDP and actual GDP. When actual and potential GDP are at the same level and are growing at the same rate, the output gap is zero and the economic cycle is said to be neutral. ↑

-

European Commission’s Spring 2023 Economic Forecast 2023, special issue Medium-term projections of potential GDP growth in turbulent times. ↑

-

Greater uncertainty and the high cost of energy will discourage investors. ↑

-

A permanent high increase in the cost of energy could well weaken potential output via a number of impact channels (see e.g. ‘How higher oil prices could affect euro area potential output’, ECB Bulletin 5/2022, Box 4). ↑

-

The national Consumer Price Index includes e.g. costs related to owner-occupied housing, including interest rates on housing loans. In this respect, it is a broader cost of living index than the narrower HICP, which is more purely a price index. ↑