Forecast

Forecast: The economy will recover from the pandemic, but even after recovery, growth will be slow

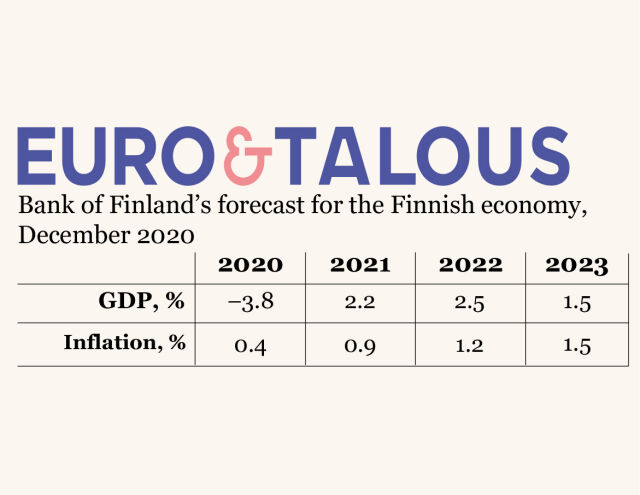

The economic downturn in 2020 will be smaller in Finland than in the rest of the euro area, but this winter will still be difficult. COVID-19 will gradually be left behind in the course of 2021 due to the vaccines, and household consumption will drive growth of 2.2% in the Finnish economy. Growth will strengthen to 2.5% in 2022. At the end of the forecast period in 2023, the economy will return to a slow 1.5% growth rate reflecting the long-term sluggish growth conditions.

The global economy has strengthened since the collapse in the spring, and positive news on vaccine development has improved sentiment. However, the economies of Finland's main trading partners are threatening to deteriorate in the coming months due to the effects of the second wave of the virus. It will take time for Finland's operating environment to recover, and investments in Finland's export markets, in particular, will remain well below pre-pandemic projections. Finnish exports will begin to gradually recover from the 2020 collapse, driven by the export markets. Net exports, i.e. the difference between imports and exports, will not contribute much to growth in the forecast years.

Economic growth in the forecast period will hinge on private consumption. Growth in household income will continue and consumer confidence will strengthen as the threat from COVID-19 recedes. The increased caution of households, the threat of unemployment and the narrowing of consumption opportunities due to restrictive measures has resulted in a record high household savings rate. Income left unused will provide more room for manoeuvre in household consumption in the years ahead.

Uncertainty over economic developments has led companies in Finland to postpone or cancel planned fixed investments. In the next few years, weak developments in construction may also weigh on investment. Overall, private investment will contract in 2020 and 2021 and only begin to clearly grow in 2022 as the uncertainty caused by the pandemic decreases and exports pick up. Even after the pandemic is over, expectations of poor profits will weigh on the appetite for investment.

The labour market will recover slowly from the pandemic and related restrictive measures. The employment rate will decline by one percentage point in 2020 and increase by about 1.5 percentage points in 2021–2023, to slightly over 73%.

Price pressures will be subdued in the forecast period. Consumer price growth has slowed to 0.4% this year due to the COVID-19 pandemic, but will gradually accelerate in 2021, supported by growing private consumption. Wages will increase by around 2% on average over the forecast period. The price of labour will rise only slightly in 2020 but accelerate in 2021 when the temporary deferrals to employers' social security contributions end. Finland's cost-competitiveness will improve compared with the euro area in 2020 but threatens to weaken in the years ahead.

Economic policy has softened the effects of the recession. The general government fiscal position relative to GDP will deteriorate almost as sharply in 2020 as in the recession in 2009 caused by the Global Financial Crisis. The deficit is deepened by a fall in tax revenues and the measures to support the economy, increased unemployment expenditure and expenditure increases under the Government Programme. The deficit in 2020 will be around 7% of GDP, from which it will gradually decrease to just over 2% in 2023. Due to the crisis, the general government debt-to-GDP ratio will increase sharply. In 2023, the debt-to-GDP ratio will be as high as 74%. The general government structural balance will further weaken as a result of the crisis, which is why the estimate of the sustainability gap has weakened to 5.5%.

Although the recession caused by the pandemic has remained smaller than feared, it nevertheless weakens potential growth. The second wave of the pandemic will cause investment to decrease further and delay the recovery of the labour market. Even after the crisis, population ageing and low productivity will weigh on long-term growth potential.

The forecast has risks in both directions. The short-term economic outlook already contains uncertainty regarding how quickly the pandemic can be brought under control. In addition to the baseline forecast, uncertainty is assessed in two alternative scenarios. A positive scenario would be if a medical solution can be brought into play already in the first half of 2021 and the economy as a result grows much more quickly than forecast. It is, however, still possible that the epidemic will spread during the winter and the public will have to be protected by a wide-ranging shutdown of the economy. In the event the epidemic is prolonged, the economy would contract further in 2021. In a worst-case scenario the COVID-19 crisis could leave a deep permanent scar on the Finnish economy.

| Key forecast outcomes | |||||

|---|---|---|---|---|---|

| Percentage change on the previous year | |||||

| 2019 | 2020f | 2021f | 2022f | 2023f | |

| GDP | 1.1 | –3.8 | 2.2 | 2.5 | 1.5 |

| Private consumption | 0.8 | –5.3 | 3.6 | 4.0 | 1.8 |

| Public financial consumption | 1.1 | 3.2 | 2.1 | –0.7 | 0.2 |

| Fixed investment | –1.0 | –3.1 | –2.2 | 3.1 | 2.2 |

| Private fixed investment | –1.6 | –5.6 | –3.2 | 3.8 | 2.3 |

| Public fixed investment | 2.1 | 8.3 | 1.7 | 0.3 | 1.8 |

| Exports | 7.7 | –9.1 | 5.7 | 3.9 | 3.3 |

| Imports | 3.3 | –7.1 | 4.5 | 4.0 | 3.3 |

| Effect of demand components on growth | |||||

| Domestic demand | 0.5 | –2.8 | 1.8 | 2.6 | 1.5 |

| Net exports | 1.7 | –0.8 | 0.4 | 0.0 | 0.0 |

| Changes in inventories and statistical error | –1.0 | –0.2 | 0.0 | 0.0 | 0.0 |

| Savings rate, households, % | 0.4 | 7.7 | 4.7 | 1.6 | 0.6 |

| Current account, %, in proportion to GDP | –0.2 | –0.7 | –0.3 | –0.4 | –0.4 |

| 2019 | 2020f | 2021f | 2022f | 2023f | |

| Labour market | |||||

| Number of hours worked | 1.2 | –1.8 | 0.5 | 1.1 | 0.8 |

| Number of employed | 1.1 | –1.6 | 0.1 | 1.1 | 0.7 |

| Unemployment rate, % | 6.7 | 7.8 | 8.3 | 7.7 | 7.4 |

| Unit labour costs | 1.3 | 2.8 | 1.5 | 0.5 | 1.4 |

| Labour compensation per employee | 1.3 | 0.6 | 3.6 | 1.9 | 2.3 |

| Productivity | 0.0 | –2.2 | 2.0 | 1.4 | 0.8 |

| GDP, price index | 1.8 | 2.1 | 1.2 | 1.3 | 1.5 |

| Private consumption, price index | 1.0 | 0.3 | 1.0 | 1.3 | 1.6 |

| Harmonised index of consumer prices | 1.1 | 0.4 | 0.9 | 1.2 | 1.5 |

| Excl. Energy | 1.0 | 0.8 | 0.8 | 1.2 | 1.4 |

| Energy | 3.0 | –4.8 | 2.2 | 1.8 | 1.9 |

| Sources: Statistics Finland and Bank of Finland. | |||||

External environment: assumptions and financial conditions

The COVID-19 pandemic continues to dominate the economic outlook. The global economy has strengthened since the collapse in the spring, and positive news of medical solutions to get a grip on the pandemic has improved sentiment among economic agents. However, the economies of Finland's key trading partners are threatening to deteriorate in the coming months due to the effects of the second wave of the virus, related restriction measures, and the uncertainty arising from the pandemic. As long as no medical solutions to stop the spread of the pandemic are available or widely adopted in the world, some of the restriction measures will have to be continued and uncertainty will overshadow economic growth. A more permanent brightening of the economic outlook will therefore require that the spread of the virus be brought under control. The forecast is based on data available on 24 November 2020.

Pace of global economic recovery dictated by epidemic developments

The global economy saw a strong recovery in the summer following the collapse in the second quarter. In September, the volume of world trade returned to early-year levels, as the virus situation abated in many countries during the summer. The strengthening of the external economic environment has also improved Finland's economic outlook, and Finland's export demand is recovering in the wake of global trade (Chart 1). However, recovery will be slow and export demand will not surpass its pre-pandemic peak until 2022.

In 2020, the global economy entered an exceptionally deep recession, and, while it appears to be slightly less severe than anticipated, global GDP will not return to the pre-crisis baseline forecast path over the forecast horizon. The global economy will continue to recover in 2021 as medical solutions to combat the spread of the virus are made available. The forecast assumes that medical solutions will be widely and successfully adopted across the globe by the first half of 2022. Towards the end of the forecast horizon, global growth will stabilise close to the long-term average, i.e. just under 4%. Nevertheless, the future development of the global economy still hinges crucially on the coronavirus situation. In the short term, in particular, it appears the uncertainty caused by the pandemic will remain high. Without medical solutions to reduce the concerns caused by the virus and the need for restriction measures, the recovery of the global economy will remain vulnerable.

chart 1.Finland's export demand will recover in the wake of world trade

The euro area economy also witnessed a strong recovery in the third quarter as the virus situation became calmer. However, euro area GDP is still lower than at the end of 2019. The recovery of European economies is slowed by the second wave of the COVID-19 epidemic, which threatens to weaken economic growth again at the turn of the year. In many of Finland’s key trading partners, such as Sweden and Germany, the COVID-19 situation has deteriorated during the autumn. Nevertheless, euro area GDP growth is expected to gain momentum in 2021 (Table 2), with the gradual adoption of medical solutions and an accelerating recovery as virus concerns recede.1 However, recovery will be slow and the output losses caused by the pandemic will mean the euro area will not return to the pre-crisis baseline forecast path over the forecast horizon. The recovery of the euro area is strongly linked to an amelioration of the pandemic.

Both private consumption and private investment will gradually recover in the euro area as uncertainty fades. Consumption and investments will reach pre-crisis levels in mid-2022. As the economy recovers from the recession, inflation in the euro area will accelerate only tentatively over the next few years. A no-deal Brexit at the turn of the year would temporarily weaken Finland's export demand slightly and raise export prices.

Financial conditions support growth

During 2020, the European Central Bank (ECB) has substantially increased its monetary accommodation. It has expanded the existing asset purchase programme and from the end of March commenced purchases under the new pandemic emergency purchase programme (PEPP) launched by the ECB Governing Council, the envelope of which was increased to EUR 1,850 billion in December and the duration extended to at least March 2022. The ECB also further relaxed the conditions of the third series of targeted longer-term refinancing operations (TLTROs) and decided in December to launch three new operations between June and December 2021. Additionally, in December the ECB decided to offer four new non-targeted pandemic emergency longer-term refinancing operations (PELTROs) in 2021. Interest rates remain low. The interest rate on the main refinancing operations is 0.00%, the rate on the marginal lending facility is 0.25% and the rate on the deposit facility is -0.50%. The ECB Governing Council expects the key ECB interest rates to remain at their present or lower levels until it has seen the inflation outlook robustly converge to a level sufficiently close to, but below, 2% within its projection horizon, and such convergence has been consistently reflected in underlying inflation dynamics.

Financial conditions in Finland have remained favourable and supportive of growth also in the latter half of 2020. The average interest rates for both new corporate loans and new housing loans have remained moderate throughout the year in Finland (Chart 2). The financial markets expect euro area short-term interest rates to decline slightly over the forecast horizon (Table 2). Continued low funding costs will contribute to the economic recovery. According to the Bank Lending Survey (BLS), credit standards for corporate loans have eased, credit standards for housing loans remained on average unchanged and credit standards for consumer loans slightly tightened this year in Finland. The survey showed that for the last quarter of the year, banks expect credit standards for household loans in Finland to ease slightly. According to the Business Tendency Survey by the Confederation of Finnish Industries EK, financial difficulties have increased slightly since early in the year in the construction sector, but in general, financial difficulties have not become a particularly significant obstacle to output or sales this year.

chart 2.Average interest rates on new loans have remained moderate

| Forecast assumptions | |||||

|---|---|---|---|---|---|

| 2019 | 2020f | 2021f | 2022f | 2023f | |

| Volume change year-on-year, % | |||||

| Euro area GDP | 1.3 | –7.3 | 3.9 | 4.2 | 2.1 |

| World GDP | 2.7 | –3.5 | 5.6 | 3.9 | 3.4 |

| World trade1 | 0.6 | –9.5 | 7.1 | 4.3 | 3.6 |

| Finland’s export markets2, % change | 1.4 | –9.6 | 6.7 | 4.9 | 3.5 |

| Oil price, USD/barrel | 64.0 | 41.6 | 44.0 | 45.7 | 46.9 |

| Export prices of Finland’s competitors, euro, % change | 1.8 | –4.5 | 0.8 | 2.1 | 1.9 |

| 3 month Euribor, % | –0.4 | –0.4 | –0.5 | –0.5 | –0.5 |

| Finland’s nominal effective exchange rate3 | 106.0 | 108.6 | 110.0 | 110.0 | 110.0 |

| USD value of one euro | 1.12 | 1.14 | 1.18 | 1.18 | 1.18 |

| 1Calculated as the weighted average of imports. | |||||

| 2The growth in Finland's export markets is the import growth in the countries Finland exports to, weighted by their average share of Finland's exports. | |||||

| 3Broad nominal effective exchange rate, 2015 = 100. The index rises as the exchange rate appreciates. | |||||

| Sources: Eurosystem and Bank of Finland. | |||||

Demand

The COVID-19 pandemic and related restriction measures will continue to strain Finland's economic growth in early 2021. However, as vaccinations bring the pandemic under control in 2021, the Finnish economy will begin to grow, driven by private consumption.

chart 3.Economic recovery led by domestic consumption

Consumption will recover rapidly as uncertainty fades

Growth in aggregate demand will rest mainly on growth in private consumption (Chart 3). In the forecast period, the purchasing power of households will be increased primarily by an increase in earnings and public transfers. Employment will start to recover slowly in 2021, which will raise household disposable income and support growth in purchasing power. Transfers will be increased especially by higher unemployment and pension income. Inflation will remain low, supporting growth in purchasing power. Overall, household disposable income will increase by an average annual rate of about 2% between 2020 and 2023. Real income will grow by an average of 1% between 2020 and 2023.

Consumer confidence is still low after the autumn, and the second wave of the coronavirus pandemic will continue to weigh on demand for private services in early 2021. As the pandemic is brought under control and uncertainty fades, private consumption will recover rapidly. In 2021 and 2022 private consumption will grow at an average rate of slightly below 4% per annum, but will later decelerate towards the long-term average, i.e. below 2%. The pandemic is not expected to leave a permanent mark on private consumption growth, but its structure may change. E-commerce, for example, may permanently increase its share of trade.

In response to households’ increased caution, the threat of unemployment, and reduced opportunities for consumption due to restriction measures, the household savings rate jumped to a record high, and will remain high in 2021 (Chart 4). As the situation normalises, the savings rate will gradually return closer to long-term levels. Over the next few years, income left unused will provide households with more scope for consumption.

The housing market has remained lively despite the coronavirus pandemic. A large number of new housing loans have been drawn down in 2020, thus accelerating the growth of the housing loan stock. Holiday cottage loans also attracted a lot of interest. At the same time, consumer credit growth has slowed significantly. No significant changes occurred in housing loan interest rates, and loan interest rates have remained moderate.

chart 4.Household savings rate returning to normal

Uncertainty weighing on investment

Uncertainty over the path of the economy has led companies in Finland to postpone or cancel fixed investments. Weak developments in construction, especially in new-build housing construction, are also weighing on investment. The volume of housing construction has continued to decline, and the number of building permits granted has declined further in 2020. In addition to the increased uncertainty, the slowdown in housing construction is explained by normal cyclical fluctuations, as there was a long boom in housing construction before the pandemic. Overall, private investment will contract in 2020 and 2021 and only begin to clearly grow in 2022 as the uncertainty caused by the pandemic decreases. Even after the pandemic is over, unfavourable demographic trends and weak productivity growth will weigh on the appetite for investment.

While the COVID-19 crisis barely tightened the financial conditions of Finnish companies, demand for corporate loans has decreased during the summer and early autumn due to low investment.

Exports will recover, but slowly

Finland's exports will decrease by almost 10% in 2020 due to contracting export markets. As the acute phase of the pandemic gradually recedes, the world economy and the Finnish export markets will begin to recover (Chart 5). Finnish exports will recover from their slump in 2020 on the back of export markets and grow by some 6% in 2021. In 2021–2022, exports will grow only slightly slower than the export markets. Finnish exports will catch up with growth in the export markets with a slight delay in 2023. Finland's goods exports are centred on capital and intermediate goods, and global uncertainty will hamper investment at the beginning of the forecast period. Overall, exports are expected to recover reasonably well over the next few years from the slump caused by the COVID-19 pandemic.

Over the next few years, imports will grow at roughly the same rate as exports. One of the factors contributing to import growth is that the Finnish export industry uses plenty of foreign raw materials and intermediate goods. The recovery of private consumption and investment will also increase imports, especially at the end of the forecast period. Net exports, i.e. the difference between imports and exports, will not contribute much to growth during the forecast period. The current account will remain in deficit in the forecast years, on average at around 0.5% of GDP.

chart 5.Export growth will remain slower than growth in export markets

Public debt will grow substantially

The general government fiscal balance relative to GDP will deteriorate almost as sharply in 2020 as in the recession in 2009 caused by the Global Financial Crisis. In 2020, the deficit will be around 7% relative to GDP, from which it will gradually decrease to just over 2% in 2023 (Chart 6).

chart 6.Coronavirus crisis severely weakening the general government fiscal balance relative to GDP

Coronavirus-related measures to combat the epidemic and support the economy, increased unemployment expenditure, and expenditure increases under the Government Programme will all significantly raise public spending in 2020. At the same time, population-ageing will sustain the annual growth in the need for services. Public investment will increase in the forecast period due to, for example, infrastructure projects and municipal authorities’ construction investments.

Revenue from taxes and tax-like payments will decrease in 2020, especially value added tax, corporate tax and employers' social security contributions. Index adjustments of earned income tax and a lowering of the industrial electricity tax will also reduce tax revenue. On the other hand, the public finances will be strengthened over the forecast horizon by tightening of certain indirect taxes, such as fuel taxes.

Out of general government, the central government bears the heaviest burden of the COVID-19 crisis. The state strongly supports municipal authorities through public transfers and changes in tax parameters, thereby temporarily strengthening the fiscal position of local government. Social security funds will temporarily post a deficit, but soon return to surplus.

In addition to the cyclical situation and accommodative fiscal policy, central government capital injections and tax payment arrangements with eased terms also directly raise public debt, even though they have no impact on the deficit. The general government debt-to-GDP ratio will increase by about 9 percentage points in 2020 compared with 2019. By 2023, the debt ratio will rise to 74% (Chart 7).

chart 7.General government debt will exceed 70% in proportion to GDP

Supply and cyclical conditions

The recession caused by the coronavirus pandemic has been less severe than anticipated, but potential growth will nevertheless slow temporarily. As a result of the second wave of the pandemic, investment will decrease further, and the recovery of the labour market will be delayed. Growth in the capital stock and labour will remain modest during the forecast period.

Employment will recover slowly

The labour market will recover slowly from the pandemic and the associated containment measures. The employment rate will decrease by one percentage point in 2020, but in 2021–2023 will increase by some 1.5%, to slightly over 73%. The number of employed at the end of the forecast period will be some 7,000 persons higher than in 2019. The unemployment rate will climb to 8.3% in 2021 and will decrease gradually, to 7.4% in 2023.

Employment weakened significantly in spring during the first wave of the pandemic, as demand collapsed due to the containment measures and health concerns related to the spread of the virus (Chart 8). As the first wave of the pandemic receded at the end of the second quarter of 2020, employment improved markedly in the third quarter. In spring, the increase in unemployment was smaller than the decrease in the number of persons employed, reflecting the large number of furloughs. The number of those on full-time furlough reached a peak in May and was approximately 170,000, and in October the number of persons furloughed was still nearly 60,000.

The labour market remains weak, despite the recovery in employment from the levels in spring when employment contracted. In late 2020, employment growth will decline as a result of the second wave of the coronavirus epidemic. In the early part of the forecast period, uncertainty will dampen both household propensity to consume and employers’ courage and possibilities of creating new jobs. Employment expectations also began to decline in autumn 2020. All the leading labour market indicators are weak, and the continued sluggishness of economic growth and the unaltered structural challenges similarly point to a slow recovery in employment. The working-age population will continue to shrink in 2020 and in the years to come, and there will be mismatch problems between vacant jobs and unemployed jobseekers. The turning of furloughs into permanent job losses and prolonged unemployment spells will slow the recovery of the labour market during the forecast period.

chart 8.Some of the furloughs will turn into unemployment

Conditions for economic growth are weak

Finland drifted into the recession caused by the coronavirus pandemic in a situation where the economy had just contracted for two consecutive quarters at the end of 2019. Annual GDP growth nevertheless remained above its potential rate in 2019, but in 2020 the output gap will turn negative, at about −3.5%, as a result of the recession (Chart 9). This is less than estimated during the summer, because the recession has not been as deep as expected. The weakening activity in service sectors had a considerable impact on the sudden deepening of the output gap during the coronavirus spring (see The depths of the COVID-19 crisis, and the recovery). The current crisis is expected to slow the economy’s potential rate of growth temporarily during the forecast period, but GDP growth is estimated to be close to its potential rate towards the end of the forecast period.

The coronavirus pandemic is a symmetric shock that has pushed the euro area economy into a deep recession. Developments in the output gap in Finland will correlate closely with the output gap in the euro area during the forecast period, even though Finland's negative output gap will not be as deep as in the euro area on average. Despite this, there will be significant underutilization of resources in the Finnish economy during the forecast period.

chart 9.Finland and the euro area in a deep recession

The crisis will dampen growth in potential output temporarily in 2020–2023 (Chart 10). Even though economic growth will return to pre-crisis rates over the medium term, the level of potential output will remain lower than before. Growth in the capital stock will remain very moderate in 2020–2021 due to the weakness of investment, which will erode potential output. The decrease in labour input caused by the pandemic and its slow recovery, as well as the slight increase in structural unemployment, will reduce the importance of labour as a source of potential output during the forecast period. Labour supply will be constrained further by the fact that the working-age population (15–74-year-olds) is beginning to shrink. Growth in total factor productivity will remain subdued, due, for example, to disruptions in supply chains and lags in the reallocation of resources.

If the pandemic drags on, it may erode the economy’s rate of potential growth even permanently (see Risk Assessment). Protracted furloughs and unemployment spells may result in higher structural unemployment and a decline in the participation rate and thus lead to a permanent decrease in labour input. Persistent weakness of investment, as well as bankruptcies and destruction of capital will erode the capital stock, and the decrease in R&D investment may also slow productivity growth in the long term. The structural rigidities and frictions in the economy will play an important role in how effectively economic resources are reallocated and how quickly potential output improves.

chart 10.The crisis will slow growth in potential output

Prices, wages and costs

The rise in consumer prices has slowed in 2020 to 0.4%, due to the effects of the COVID-19 pandemic. Inflation will, however, recover gradually during the forecast period, supported by growth in private consumption. Growth in nominal earnings will slow to 1.7% in 2020 and will pick up slightly in 2021. The index of wage and salary earnings will increase by an average of some 2% per annum in the forecast period. Reflecting furloughs and permanent layoffs, total wages dipped in the second quarter of 2020, despite the rise in earnings. As a result, compensation per employee will increase in 2020 only slightly, but the rate of increase will return to pre-pandemic levels during the forecast period. Finland's cost-competitiveness will improve relative to the euro area in 2020, but threatens to weaken in the coming years.

Rise in consumer prices came to a halt

Consumer price inflation, as measured by the harmonised index of consumer prices (HICP inflation) will slow to 0.4% in 2020, due to the indirect effects of the COVID-19 pandemic (Chart 11). The rate of inflation in Finland has, however, been higher than in the euro area. For example, HICP inflation in October was in Finland 0.2%, whereas in the euro area, it was only −0.3%. The rise in prices was dampened by the notable fall in crude oil prices in the second quarter; oil prices have however risen from their trough in the course of the year. Underlying inflation too, has slowed notably in Finland in 2020, as in the other euro area countries. Due to the effects of the pandemic, services inflation will slow to only some 1% and the prices of consumer goods (non-energy industrial goods) will decline by 0.5% compared with the previous year. In contrast, food prices (incl. alcohol and tobacco) have risen by over 2%, due to higher demand as a result of the pandemic.

chart 11.Inflation will pick up during the forecast period as consumption recovers

In 2021, inflation will pick up to 0.9%. In the early months of the year, inflation will remain slow, continuing the trend witnessed in the fourth quarter of 2020, as demand is dampened by the impacts of the pandemic. In the second quarter, inflation will increase to 1.2%, as a result of the upward pressure exerted on energy prices. Towards the end of the year 2021, higher consumption, and the fading of the impacts of the pandemic as assumed in the baseline scenario, will support particularly services inflation. Tax increases will push inflation by 0.4 percentage points in 2021, reflecting the rise in fuel taxes in August 2020 and the rises in tobacco and alcohol taxes agreed for 2021.

Towards the end of the forecast period, inflation will be supported by growth in private consumption and the closing of the output gap. Underlying inflation will pick up gradually, reflecting particularly a rise in services prices. The upward trend in energy and food prices will continue as the economy recovers. Overall HICP inflation will accelerate to 1.2% in 2020 and will reach 1.5% in 2023.

Wages will rise by some 2% per annum

Increases in negotiated wages, included in the two-year collective labour agreements concluded in early 2020, were slightly above 3%. The increases in negotiated wages were in 2020 as a rule smaller than those agreed for 2021. Based on data for the first three quarters of 2020, growth in nominal earnings measured by the index of wage and salary earnings will slow to 1.7% in 2020 (Chart 12). In 2021, the rise in the index of wage and salary earnings will accelerate to 2.2%, even though growth in wage drift is expected to remain slow, reflecting the weakness of the economic cycle. Nominal wages are expected to rise by some 2% on average during the forecast period 2020–2023.

chart 12.Earnings growth close to 2%

Compensation per employee will increase by only 0.6% in 2020. The slower rate of increase is due to, for example, the extensive furloughs in response to the pandemic as well as the temporary reductions in employer pension contributions in 2020 to mitigate the effects of the pandemic. The upward trend in compensation per employee will pick up to 3.6% in 2021, and in 2022–2023 it will be close to 2%. Nominal unit labour costs will increase by nearly 3% in 2020 as labour productivity starts to decline. Towards the end of the forecast period, the increase in unit labour costs will, however, slow significantly as labour productivity growth returns to pre-crisis levels.

Cost-competitiveness will weaken slightly

Due to the COVID-19 pandemic, estimates of developments in cost-competitiveness, and particularly labour productivity, are subject to significant uncertainty. Finland's cost-competitiveness is projected to weaken slightly during the forecast period. Cost-competitiveness appears to improve relative to the euro area in 2020, as measured by unit labour costs adjusted for the terms of trade. Cost-competitiveness, however, threatens to weaken in the later years of the forecast period (Chart 13). According to the December 2020 Eurosystem macroeconomic projections, growth in unit labour costs in the euro area will be negative, but in Finland it is expected to enter positive territory.

chart 13.Finland's cost-competitiveness relative to the euro area

Risk assessment

The forecast includes both upside and downside risks. The greatest uncertainty with regard to the economic outlook relates to how quickly the pandemic will be brought under control with a medical solution and how swiftly the global uncertainty will fade. There is also considerable uncertainty as to how the spreading of the virus can be prevented before a medical solution is successfully implemented. If the number of infections increases and containment measures must be tightened, it would have significant negative impacts on the economy, particularly in the labour-intensive service industries.

It is uncertain whether the coronavirus pandemic can be fully contained during 2021. The rapid strengthening of the second wave and the fear of new infections will cut domestic demand and particularly the consumption of services. Merely lifting the containment measures will not be enough to restore economic activity to previous levels. Consumers may be wary of consuming services in particular until a medical solution is effectively introduced to deal with the spread of the virus.

Developments in export markets are also subject to considerable risks. The strong second wave of the coronavirus epidemic in Finland’s export markets and the re-tightening of containment measures towards the end of 2020 create uncertainty and may result in investments important for Finnish exports being deferred long into the future. The strength of the epidemic and the robustness and timing of the containment measures put in place differ across countries. So, the uncertainty in the export market will continue for quite some time.

It is difficult to estimate when a medical solution will be implemented successfully. It is therefore also difficult to estimate the economic impact of the virus and the prolongation of the containment measures. The exceptional degree of uncertainty associated with the baseline forecast can, however, be illustrated with alternative scenarios. This risk assessment describes the December 2020 baseline forecast and two alternative scenarios on Finnish economic developments in the years to come (Table 3).

| Description of scenarios and baseline forecast | |||

|

|

Mild scenario |

Baseline forecast |

Severe scenario |

|

Assumptions on the pandemic |

The virus is contained quickly (e.g. due to advances in medical treatment or other measures). |

The virus cannot be contained rapidly, and some containment measures must remain in place in 2021. A medical solution is implemented successfully into the entire population in 2021. |

The virus is not properly contained. Successful implementation of medical solutions takes longer. Strict containment measures must be reintroduced and some of them must be kept in place for significantly longer than assumed in the December 2020 baseline forecast. |

|

Rate of economic recovery |

Rapid economic recovery begins at the start of 2021. |

Economic recovery strengthens in 2021. |

The economic recession is deep and the recovery remains clearly slower than the December 2020 baseline forecast. |

|

GDP in 2023 |

No significant permanent economic impact. GDP returns to the trajectory projected before the onset of the crisis. |

Some permanent economic impact. GDP remains slightly below the trajectory projected before the onset of the crisis. |

Significant permanent economic impact. GDP remains well below the trajectory projected before the onset of the crisis. Uncertainty remains very high. |

|

Inflation |

Demand factors, e.g. subdued consumption, curb price increases in the short term. No significant supply factors. |

Temporary slowdown in inflation. Demand factors curb price increases, as supply factors remain less significant. |

Inflation slows over the longer term. Demand factors curb prices more than supply factors. |

Baseline forecast: As the pandemic fades, economic growth starts to strengthen

The Bank of Finland's December 2020 baseline forecast assumes that the virus will be contained only in late 2021. A vaccination or an effective treatment will be rolled out to the public to an adequate extent during 2021. Uncertainty will however prevail until late 2021.

The baseline forecast assumes that the Finnish economy will recover in 2021–2023, but that in the later years of the forecast period GDP will remain slightly below levels projected in the Bank of Finland's December 2019 forecast, i.e. the pre-crisis trajectory (Chart 14). The losses in the volume of goods and services output, i.e. GDP, are cumulatively estimated at over EUR 25 billion in 2020–2023.2

The economy will suffer some permanent output losses as a result of the weaker employment situation and bankruptcies. Unemployment will remain higher than pre-crisis levels (Chart 15). GDP will decline considerably in 2020 and economic recovery will be relatively slow in 2021. Uncertainty will fade towards the end of 2021 and export markets will pick up, which will boost GDP growth in 2021 and 2022. In 2023 economic growth will return close to medium-term growth rates.

chart 14.Baseline forecast subject to exceptionally high uncertainty

The economy will recover gradually in 2021 and 2022, supported by private consumption. Exports too will return close to the pre-crisis growth path, driven by growth in export markets. Imports will grow, alongside consumption and exports, and therefore net exports will not have a positive contribution to GDP growth. Private investment will pick up in 2022 and 2023, but will remain moderate relative to historical levels.

chart 15.Sharp rise in unemployment

Mild scenario: a rapid vaccination programme roll-out would save the economy from permanent damage

The mild scenario describes a situation where the pandemic is contained worldwide faster than estimated in the baseline forecast, as a result of medical advances and robust targeted measures. With the pandemic brought under swift and unwavering control, fears of new outbreaks are substantially diminished. The containment measures can be eased significantly already in the early months of 2021. In this scenario, there are hardly any significant long-term output losses.

The rate of economic recovery in the mild scenario is rapid (Chart 14), and by 2023 real GDP returns very close to the trajectory projected before the coronavirus crisis. GDP growth contracts sharply in 2020 but picks up again and reaches a robust rate in 2021 (Table 4). In 2023, GDP growth decelerates towards its medium-term path. Employment growth is significantly stronger than assumed in the baseline forecast, and towards the end of the forecast period employment is already very close to its pre-crisis growth path.

| Forecast summary | ||||||

| 2019 | 2020f | 2021f | 2022f | 2023f | ||

| GDP, annual growth (%) | Mild scenario | 1.1 | –3.7 | 3.2 | 2.7 | 1.5 |

| Baseline forecast | 1.1 | –3.8 | 2.2 | 2.5 | 1.5 | |

| Severe scenario | 1.1 | –3.9 | –0.4 | 1.3 | 1.8 | |

| Employment rate (%) | Mild scenario | 72.6 | 71.7 | 72.4 | 73.2 | 73.5 |

| Baseline forecast | 72.6 | 71.6 | 71.8 | 72.7 | 73.2 | |

| Severe scenario | 72.6 | 71.6 | 71.2 | 71.3 | 71.7 | |

| Unemployment rate (%) | Mild scenario | 6.7 | 7.8 | 8.0 | 7.1 | 6.7 |

| Baseline forecast | 6.7 | 7.8 | 8.3 | 7.7 | 7.4 | |

| Severe scenario | 6.7 | 7.9 | 8.9 | 8.8 | 8.4 | |

| General government deficit, relative to GDP (%) | Mild scenario | –1.0 | –6.9 | –3.8 | –2.5 | –1.8 |

| Baseline forecast | –1.0 | –7.1 | –4.7 | –3.2 | –2.4 | |

| Severe scenario | –1.0 | –7.1 | –6.6 | –5.1 | –3.8 | |

| General government debt, relative to GDP (%) | Mild scenario | 59.3 | 68.3 | 69.5 | 69.9 | 70.8 |

| Baseline forecast | 59.3 | 68.4 | 71.3 | 72.6 | 74.0 | |

| Severe scenario | 59.3 | 68.6 | 75.2 | 79.2 | 81.7 | |

| Inflation* (%) | Mild scenario | 1.1 | 0.4 | 1.2 | 1.5 | 1.7 |

| Baseline forecast | 1.1 | 0.4 | 0.9 | 1.2 | 1.5 | |

| Severe scenario | 1.1 | 0.4 | 0.6 | 0.8 | 1.0 | |

| Mild scenario: The economy recovers quickly without significant and permanent output losses. Baseline forecast: The Bank of Finland's December 2020 baseline forecast. Severe scenario: The economy recovers slowly and with significant permanent output losses. |

||||||

| * Harmonised Index of Consumer Prices, HICP. f = forecast |

||||||

| Sources: Statistics Finland and Bank of Finland. | ||||||

Containment measures and fear of the virus cause a temporary dip in private consumption, especially in the demand for services, which, however, recovers rapidly as the threat of the virus fades. Growth in private consumption is considerably stronger than assumed in the December 2020 baseline forecast and is already in 2021 higher than pre-corona crisis levels. Consumption continues to grow at a rapid pace also in 2022, as income saved during the corona crisis is spent on private consumption. Consumer demand starts to grow as the corona crisis is left behind. The export market suffers, but, as uncertainty fades, there is a relatively rapid recovery in exports and investment activity. Weak aggregate demand slows inflation only in the short term.

Severe scenario: a prolonged pandemic would leave permanent scars on the economy

In the severe scenario, the virus is not properly contained until towards the end of the forecast period and some containment measures must remain in place for considerably longer than assumed in the December 2020 baseline forecast. Uncertainty concerning health and the economy, therefore, remains clearly higher than in the baseline scenario. As in the baseline forecast, in the severe scenario it is assumed that a vaccine or viable treatment will come onto the market in 2021, but here its extensive introduction is delayed considerably. Broadly speaking, this adverse scenario thus describes the risks caused by the virus, indicating weaker-than-expected economic developments relative to the December 2020 baseline forecast.

In the severe scenario, the economy contracts also in 2021 and begins to grow only slightly in 2022. There are considerably more permanent production losses in various sectors than in the situation described in the December 2020 baseline forecast. A substantial number of companies go bankrupt and a large part of the rise in unemployment becomes permanent. In this scenario, GDP remains nearly 4% lower in 2023 than the trajectory projected before the coronavirus crisis.

In the severe scenario, containment measures and fear and uncertainty regarding new infections reduce household consumption. Firms put off investment as demand is weak, capacity utilisation is low and there is elevated uncertainty about the future. The globally unfavourable investment environment weakens the prerequisites for a recovery in Finnish exports. A decline in investment in Finland’s important export markets depresses economic growth in Finland over the long term. Weak demand keeps inflation low during the forecast period.

General government finances will weaken

The sharp contraction in the Finnish economy weakens the public finances considerably in all three scenarios, including the baseline forecast. The weakest trend is in the severe scenario, where the permanent decline in output and employment levels is especially significant. The increase in the general-government debt ratio from 2019 to 2023 varies between over 10% and over 20%, depending on the scenario. In 2019, the debt-to-GDP ratio was just under 60%. The decline in employment and private consumption decreases tax revenues, while at the same time higher unemployment is pushing up public expenditure. The widening of the general government deficit is also due to the measures implemented by government to soften the impact of the recession (see General government debt).

Economic recovery will depend on the evolution of the pandemic

The forecast is subject to both downside and upside risks. Particularly in the short term, i.e. in 2021, economic growth may be stronger than in the December 2020 baseline forecast. This can be the case if a vaccine is rolled out to the public more effectively than expected. It needs to be stressed that the uncertainty contained in the assessments stems particularly from the fact that we do not know how the coronavirus pandemic will play out in the near future, in Finland and elsewhere in the world. There is also considerable uncertainty as to how the spreading of the virus can prevented in various parts of the world. The pandemic will not be over until it has been suppressed all around the world.

If there are considerable delays in the roll out of the vaccine, or if targeted measures to reduce infections prove unsuccessful or voluntary recommendations, such as social distancing and the use of masks, are not adequately followed, the number of infections will increase and containment measures will have to be tightened. This would have significant negative impacts on the economy, particularly in the labour-intensive service industries. While there have been advances in the medical treatment of the coronavirus, the disease is by no means conquered yet. For one, there is still uncertainty pertaining to the effective roll-out of vaccines, so that the virus can be suppressed globally.

Other factors will also shape the recovery

There is also uncertainty as to what sort of structural changes the crisis will bring in the areas of, say, international trade, the division of labour, and production. In terms of economic impact, it is also relevant how the crisis will affect digitalisation and influence consumer behaviour. Structural changes can have both favourable and adverse impacts on the economy.

The extensive fiscal and monetary policy measures implemented globally have mitigated the recession caused by the pandemic, in both Finland and elsewhere around the world. Future economic developments will depend on the continuation, targeting, and timing of these and similar measures. In a crisis, it is important that economic support-measures remain in place for as long as necessary to minimise long-term harm. Similarly, cost-competitiveness will be a crucial factor in how Finland emerges from the crisis.

The December 2020 baseline forecast is the likeliest outcome for the economy. However, the mild and severe scenarios do not necessarily depict the best or weakest possible economic outcomes, and economic growth may prove slower or faster than indicated.

The longer the coronavirus crisis continues, together with the immense uncertainty surrounding it, the more long-term harm it will cause the economy as bankruptcies and unemployment increase. Reallocating resources effectively is important in terms of economic recovery, and it is also subject to uncertainty. For example, the allocation of labour from low-productivity service industries to, say, the ICT sector requires training and does not happen without friction.

Furthermore, a delay in the revival of the export market would have a very detrimental impact on the recovery of Finnish export industries. A prolongation of the crisis combined with a possible decline in competitiveness and rapidly increasing general government debt would exacerbate and prolong the economic recession in the years ahead. The article The depths of the COVID-19 crisis, and the recovery, discusses the channels through which the crisis may leave long-term scars on employment, the capital stock or on productivity.

Notes

-

More detailed information on the euro area forecast is available at https://www.ecb.europa.eu/pub/projections/html/index.en.html. ↑

-

The baseline scenario preceding the coronavirus crisis refers to the Bank of Finland's December 2019 forecast for 2019–2022. The forecast is based on the assumption that economic growth in 2023 will move closer to long-term growth rates. ↑