Blog

Money in the digital era

Olli Rehn

GovernorDigitalisation a formidable force of change

Digitalisation is currently the most significant force transforming banking as well as the entire financial industry at large. Most payment and financial services have already shifted online and are readily accessible through people’s mobile devices. In the future, financial services will become increasingly untethered from the constraints of location, granting users immediate and on-the-go access. The adoption of instant payment infrastructures will only accelerate this process.

From the perspective of the individual, the financial industry's digital transformation will be most evident in the nature of payments. Payment methods have proliferated as a variety of mobile applications have joined the ranks of card payment and cash. Credit transfers between bank accounts will soon happen instantaneously. For many, digital services have effectively become a form of hidden consumption, where payment is relegated as a background process. Purchases might be made irrespective of cash on hand or account balance, demanding strong financial literacy and spending practices from consumers.

New opportunities, new risks

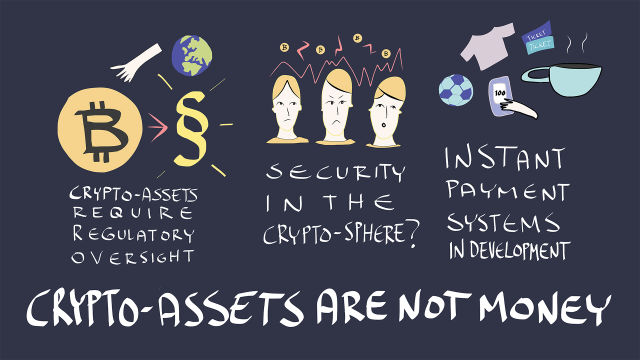

The financial industry's transformation will leave individuals and society with a variety of new phenomena to contend with. First, there are those which should be actively developed and adopted, such as instant and mobile payments. These will, however, place greater weight on personal financial literacy and data protection. Second are phenomena that ought to be approached with caution or avoided outright, such as, for example, crypto-assets, which are laden with issues and risks including high volatility, tax evasion, money laundering, and wasteful energy consumption. Third are those which still require a period of maturation. One such example is blockchain technology, which is not yet ready for implementation by central banks but holds promise for the financial sector and central banks alike.

Authorities must actively monitor the financial market's structural transformation and ensure that the use of digital financial services is safe and reliable. While maintaining financial stability remains a duty of primary importance, authorities should also seek to promote innovation within the heavily-regulated financial sector.

Productivity growth dependent on technological change

Digitalisation will transform work and labour markets. Technological change is an enduring feature of civilisation and one that has been feared in equal measure. Machine learning, robotic process automation and artificial intelligence are gaining foothold across all sectors in society, including the financial industry. Digital technology is being leveraged, for example, to automate work processes and utilise big data.

Economic history suggests that the adoption of new technology does not result in permanent mass unemployment. Instead, the tasks of workers change, and new jobs are created in new sectors. Promoting life-long learning and providing opportunities for further training or requalification would allow society to better prepare against disruptions caused by technological change.

Tasks that require interpersonal interaction or expert knowledge as well as jobs in creative fields, management and high value-added manufacturing are all examples of professions that are unthreatened by technological change. Education looks to remain a prudent investment for society, particularly in view of rapidly shifting labour markets.

Monetary policy in a digitalising world

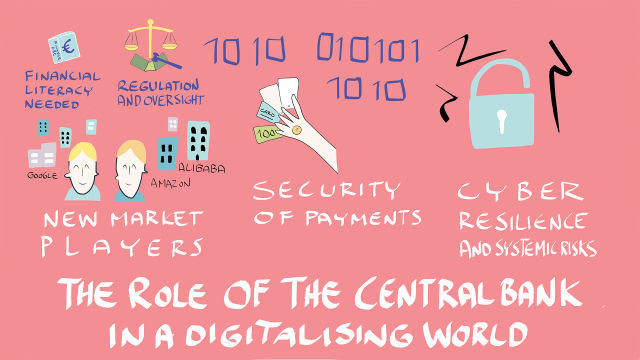

Monetary policy is the key responsibility of any central bank. In the euro area, national central banks implement the Eurosystem's single monetary policy, via monetary policy operations conducted with eligible counterparties. Should the situation arise where a large proportion of financial services are provided by institutions who are not central bank counterparties, then the operational framework for monetary policy implementation ought to reflect this. The successful transmission of monetary policy into the real economy requires good understanding of how financial services will be offered in the future, and by whom.

Finland well-positioned to become a leading country in finance

Finland has long enjoyed considerable expertise in technology and finance, backed by an operating environment conducive to innovation. As such, Finland has all the right elements to become a leading country in financial technology (FinTech). The financial sector is a diverse growth industry that spans not only personal banking and payments but also corporate finance, securities trading, investment and insurance activities and cyber security.

Finland may yet grow into an increasingly attractive hub for the financial industry with the right amount of resolve, investment and collaboration between authorities and domestic businesses. The Bank of Finland, the Financial Supervisory Authority and other national authorities are tasked with exercising an operating model which at once fosters innovation but does not compromise on the stability and security of financial sector operations.