Editorial

Inflation down and recovery supported by interest rate cut

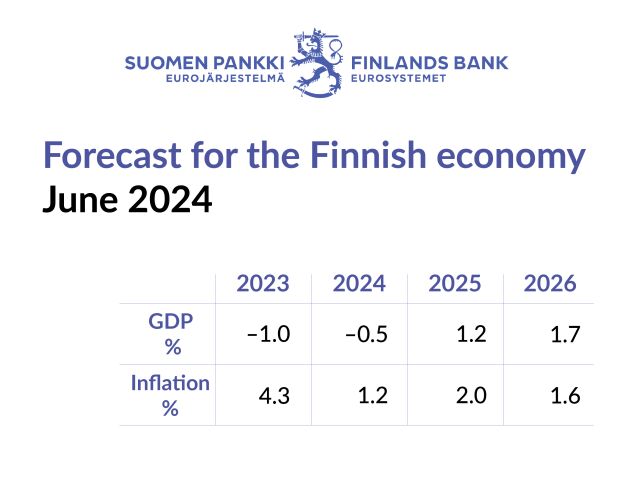

The Bank of Finland’s June forecast shows that the Finnish economy will gradually recover as the year wears on. Inflation has come down, and the purchasing power of Finnish households is rising. Household and business confidence will also start to improve gradually. As the economy recovers, employment, too, will start to pick up.

The purchasing power of households began to rise in spring 2023 as inflation fell significantly, supported by tight monetary policy, and earnings and current transfers increased strongly. The improvement in purchasing power began earlier in Finland than in the euro area. During the recent years of high inflation, Finland’s inflation rate has stayed below the euro area average, which has improved the real purchasing power of Finnish households in comparison with the euro area.

The severest inflationary pressure in the euro area has abated, and inflation is declining towards the European Central Bank’s (ECB) symmetric 2% target. Inflation is expected to return to the 2% target next year.

It is important to see the forest for the trees. Considerable progress has been made in bringing inflation down to target, especially since September 2023. Financing conditions have been held tight in order to curb demand and to keep inflation expectations firmly anchored to the inflation target. Overall, the dynamics of inflation continue to indicate that it will fall in the medium term, even though its downward path has slowed somewhat in recent months.

Against this backdrop, we decided, in the ECB’s Governing Council, to reduce policy rates by 0.25 percentage points at our June meeting. The deposit facility rate is now at 3.75%. In the decision-making we focused on three factors in particular: the inflation outlook, the dynamics of underlying inflation, which excludes energy and food prices, and the strength of monetary policy transmission. We decided that it is appropriate now to moderate the degree of monetary policy restriction after nine months of holding rates steady.

The Governing Council is determined to ensure that inflation returns to the 2% medium-term target in a timely manner, and to set the monetary policy stance on this basis. We will set our rates based on our analysis at each Governing Council meeting. We are not pre-committing to any particular rate path.

The global crises of recent years have transformed Finland’s international operating environment. Analysis by the Bank of Finland suggests that the Finnish export industry lost market shares in world goods export markets during the 2010s. Finland's exports are focused on the kinds of products and market areas whose share of world trade has developed weakly. Europe has been an important market for Finnish exports, but growth in the European economy was subdued for a long time after the global financial crisis. Neither has the composition of Finland's exports in terms of countries and products adjusted itself to the structural changes in world trade.

Following Russia’s invasion of Ukraine, the foreign trade of Finland and most other European countries with Russia has collapsed. In Finland, imports in general have shrunk in products where Russia's share of imports was large before the war. For example, roundwood imports from Russia have been only partially replaced with imports from other countries. In addition, the cessation of trade with Russia has increased prices of production inputs previously imported from there. However, for the economy as a whole, the effects of ending trade in goods with Russia have been limited.

Finland’s cost competitiveness weakened after the global financial crisis, but then improved and has remained fairly stable in recent years. However, a closer examination reveals a longer term development that is concerning for Finland.

Since the global financial crisis, Finland’s cost competitiveness has been weakened by the low growth in labour productivity in comparison with the country’s trading partners. At the same time though, competitiveness has been bolstered by the fact that the growth in labour costs has remained moderate. Put another way, weak productivity performance has not permitted labour cost growth to be any higher. A sustainable improvement in competitiveness in the longer run can only happen through an improvement in productivity.

Finland’s weak productivity performance since the global financial crisis has been the result of slow adjustment to negative shocks in key industries and structural difficulties. It is, of course, possible that the economy’s adjustment to the negative shocks is still a work in progress. In any event, it is necessary to support productivity development through public sector measures as well.

Now, when public funding for research, development and innovation (RDI) is also being increased, it is important when directing this funding to take into account that most innovations used in Finland have been produced elsewhere. By investing in basic research and related higher education, we strengthen our capacity to adopt innovations made in other countries.

Innovation potential can also be improved by work-based immigration of highly educated individuals and through the internationalisation of Finnish companies. It is also important to ensure that we have an efficient tax system and well-functioning competition policy. This is all about having an overall package of policies and measures that requires commitment on a long-term basis.

Work must also continue at the same time to rebalance the public finances. In the immediate years ahead, Finland’s public finances will remain in deficit and the public debt-to-GDP ratio will continue to grow, despite the Government’s substantial fiscal adjustment measures. The weakness in the economy and the still rising level of interest payments on government debt will make it difficult to rebalance the public finances.

Direct fiscal adjustment measures to strengthen the public finances are justified, on both the expenditure and revenue side, although the measures will probably reduce output temporarily in comparison with having no adjustment measures.

The employment rate has fallen with the cooling of the economy, and the unemployment rate has risen from its low level of spring 2022. On the other hand, employment is still relatively high in comparison with recent history, and it is projected to rise again next year. Therefore, the current timing for fiscal adjustment measures does not appear to be especially problematic.

Going forward, it is important to set shared goals for the longer term and to commit to these across parliamentary terms. Reform of the domestic fiscal framework will provide a valuable opportunity for this debate.

Helsinki, 11 June 2024

Olli Rehn

Governor