Forecast

Finland's economy will gradually recover from the sudden shutdown

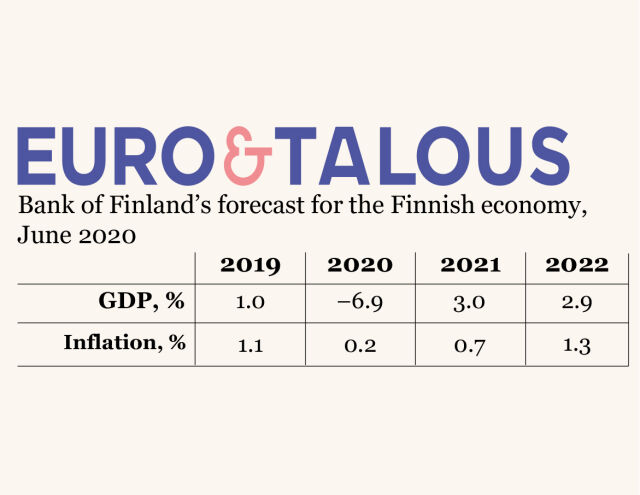

The Finnish economy is experiencing a sharp contraction on account of the coronavirus pandemic. Gross domestic product will decline by around 7% this year and grow around 3% per annum in 2021 and 2022. The forecast contains an exceptionally large degree of uncertainty. According to alternative scenarios, the contraction in the economy in the current year could be just 5% or as much as 11%, depending on how the epidemic progresses in Finland and what success there is in bringing it under control. The degree of success in controlling the epidemic will also determine how quickly the economy will recover. It will probably not be possible to avoid permanent losses of output, but economic policy can be used to mitigate their scale.

chart 1.Economic recovery led by domestic consumption

The global economy will drift into recession this year, and the economies of Finland’s most important trading partners will suffer considerably from the corona pandemic. The outlook for the Finnish economy is overshadowed by both the weakness of the global economy and the restrictive measures taken domestically in response to the coronavirus. Weakened household and business confidence also overshadow the prospects for growth. Key to recovery in the global economy will be how successfully the virus can be brought under control around the world and how long the restrictions have to be kept in place.

Both domestic demand and net exports will contract strongly in 2020. Growth in public demand will, however, somewhat moderate the contraction in the economy. At the same time the structure of the economy will change in an unfavourable direction, towards increasing dependence on public demand. The acute phase of the corona crisis will gradually pass, and the economy will begin to recover, led by private consumption. Foreign trade will not support the Finnish economy during the years covered by the forecast, as the halt in global investment caused by the corona crisis and Finland’s weakening cost-competitiveness will keep the outlook for exports very subdued. Moreover, the prevailing uncertainty will continue to slow growth in consumption and investment even after the lifting of restrictions.

The corona pandemic will cause lasting damage to the Finnish economy, as not all companies will survive the deep recession and some job losses will be permanent. During the years covered by the forecast, GDP will certainly come in lower than the pre-crisis level, as the recovery from the recession will be slow. In the present recession, unemployment will decline much less than during the depression of the 1990s, but a little more than during the financial crisis of around a decade ago. The employment rate will decline around 2 percentage points in 2020–2021 and recover only partially in 2022.

Consumer price inflation will be subdued in the current year, with weakened demand due to the coronavirus and the decline in the price of crude oil having a dampening effect on inflation. The effects of the pandemic will be reflected in inflation throughout the forecast period, but the pace of price rises will begin to be restored towards the end of the period as demand recovers. Nominal wages will rise an average of around 2% per annum in 2020–2022. Finland’s cost-competitiveness will decline somewhat relative to the euro area.

The general government balance will deteriorate and public debt will grow by a record amount in a short time. This is due to the decline in tax revenues, growth in unemployment expenditures and other expenditures as well as government measures to soften the economic impacts of the lockdown. In addition, there will be a further increase in risks arising from government guarantees. The general government balance will also be weakened by the expenditure increases contained in the Government Programme, which will exceed the growth in revenues. The general government deficit relative to GDP will deepen to 8%, and public debt will rise to a full 71% in proportion to GDP in 2020. In 2022, the debt ratio will already be approaching 75%, from where it will continue to grow in the years ahead.

| Key forecast outcomes | ||||

|---|---|---|---|---|

| Percentage change on the previous year | ||||

| 2019 | 2020f | 2021f | 2022f | |

| GDP | 1.0 | –6.9 | 3.0 | 2.9 |

| Private consumption | 1.0 | –6.4 | 4.6 | 3.4 |

| Public final consumption | 0.9 | 5.5 | 0.1 | 0.1 |

| Fixed investment | –0.8 | –9.2 | –1.0 | 4.8 |

| Private fixed investment | –1.0 | –12.4 | –1.1 | 6.0 |

| Public fixed investment | 0.3 | 6.0 | –0.3 | 0.4 |

| Exports | 7.2 | –15.8 | 4.4 | 7.0 |

| Imports | 2.2 | –9.4 | 2.4 | 6.8 |

| Effect of demand components on growth | ||||

| Domestic demand | 0.5 | –4.2 | 2.3 | 2.9 |

| Net exports | 1.9 | –2.6 | 0.7 | 0.0 |

| Changes in inventories and statistical error | –1.4 | 0.0 | 0.1 | 0.0 |

| Savings rate, households, % | 0.4 | 6.9 | 3.9 | 2.3 |

| Current account, %, in proportion to GDP | –0.8 | –2.3 | –1.9 | –1.9 |

| 2019 | 2020f | 2021f | 2022f | |

| Labour market | ||||

| Number of hours worked | 0.8 | –4.5 | 1.3 | 0.8 |

| Number of employed | 1.1 | –2.8 | –0.5 | 0.8 |

| Unemployment rate, % | 6.7 | 9.0 | 9.3 | 8.8 |

| Unit labour costs | 1.7 | 3.9 | 1.8 | 0.1 |

| Labour compensation per employee | 1.6 | –0.5 | 5.4 | 2.2 |

| Productivity | –0.1 | –4.2 | 3.5 | 2.1 |

| GDP, price index | 1.8 | 0.3 | 0.9 | 1.8 |

| Private consumption, price index | 1.1 | 0.2 | 0.8 | 1.4 |

| Harmonised index of consumer prices | 1.1 | 0.2 | 0.7 | 1.3 |

| Excl. Energy | 1.0 | 0.7 | 0.8 | 1.1 |

| Energy | 3.0 | –6.8 | –0.2 | 2.9 |

| Sources: Statistics Finland and Bank of Finland. | ||||

External environment: assumptions and financial conditions

The coronavirus pandemic is causing considerable uncertainty in the growth outlook for the global and euro area economies. The global economy will enter recession in the course of 2020, with the economies of Finland’s major trading partners suffering from both the direct consequences of the pandemic and the uncertainty created by the virus. The outlook for the Finnish economy is overshadowed by the weakness of the external environment. The recovery of the global economy will depend, among other things, on how successfully the virus can be contained in different parts of the world and how long the containment measures will have to remain in place. The forecast is based on data available on 25 May 2020.

Global outlook has suddenly weakened

Global economic conditions have deteriorated considerably during the spring in response to the Covid-19 outbreak developing into a global pandemic. In many countries, the measures adopted to contain the spread of the virus, together with the widespread uncertainty following in the wake of the pandemic, have weakened the operating environment of especially the service sector but also damaged global production chains and hence hampered industrial activity. The uncertainty weighs on both consumption and investment on a global scale, which will be reflected in a sharp decline in Finnish export demand this year (Chart 2). The outlook for Finland’s major trading partners has also declined drastically (Short-term economic outlook has deteriorated drastically in Finland, Sweden and Germany).

Prospects for recovery in the global and euro area economies are currently shrouded in major uncertainties, given the difficulties in predicting the course of the pandemic. Some containment measures are assumed to remain in place, as a medical breakthrough, for example in the form of a vaccine, is not expected until the middle of 2021. Following the collapse witnessed in the second quarter of the year, Finland’s export markets will start to revive in the second half of the year. Recovery will be slow, however, and export demand will not exceed the level of 2019 during the forecast period. The export prices of Finland’s competitors will fall this year in response to the decline in global demand (Table 2).

chart 2.Employment contracts dramatically

The euro area economy is projected to see a clear downturn. In the absence of a medical cure to contain the spread of the coronavirus, containment measures will have to be kept partly in place, with high uncertainty still surrounding future developments. This weighs on the euro area economic outlook, and potential output will not have been restored by the end of the forecast horizon. Euro area GDP will contract 8.7% in 2020, following a sharp decline in both domestic demand and exports. In an environment of sluggish economic activity and falling prices for commodities, notably oil, consumer price pressures in the euro area will remain subdued.

During the course of the spring, the European Central Bank (ECB) has substantially increased its monetary accommodation. It has expanded the existing asset purchase programme and from the end of March commenced purchases under the new pandemic emergency purchase programme (PEPP) launched by the ECB Governing Council, the envelope of which was enlarged to EUR 1,350 billion in June and the duration extended to mid-2021. In addition, the ECB further relaxed the conditions of the third series of targeted longer-term refinancing operations (TLTROs) and decided to launch a new series of untargeted pandemic longer-term refinancing transactions.

Interest rates remain low. The interest rate on the main refinancing operations is 0.00%, the rate on the marginal lending facility is 0.25%, and the rate on the deposit facility is −0.50%. The ECB Governing Council expects the key ECB interest rates to remain at their present or lower levels until it has seen the inflation outlook robustly converge to a level sufficiently close to, but below, 2%, within its projection horizon, and such convergence has been consistently reflected in underlying inflation dynamics. The financial markets do not expect short-term interest rates to rise over the forecast horizon (Table 2). Continued low funding costs will contribute to the economic recovery. The recovery of the euro area economy is also important for the revival of the Finnish economy.

chart 3.Finland and euro area in deep recession

| Key forecast assumptions | |||||

|---|---|---|---|---|---|

| 2018 | 2019 | 2020f | 2021f | 2022f | |

| Finland's export markets1, annual growth (%) | 3,7 | 1,6 | –14,1 | 8,8 | 5,1 |

| Oil price, USD/barrel | 71,1 | 64,0 | 36,0 | 37,2 | 40,7 |

| Export prices of Finland's competitors, in euro, annual growth (%) | 1,4 | 1,6 | –3,7 | 0,9 | 2,4 |

| 3 month Euribor, % | –0,3 | –0,4 | –0,4 | –0,4 | –0,4 |

| Finland's 10-year government bond yield, % | 0,7 | 0,1 | -0,1 | –0,1 | 0,1 |

| Finland's nominal competitiveness indicator2 | 106,8 | 106,3 | 108,0 | 108,4 | 108,4 |

| US dollar value of one euro | 1,18 | 1,12 | 1,09 | 1,08 | 1,08 |

| 1The growth in Finland's export markets is the import growth in the countries Finland exports to, weighted by their average share of Finland's exports. | |||||

| 2Broad nominal effective exchange rate. | |||||

| Sources: Eurosystem and Bank of Finland. | |||||

Demand

Private consumption, private investment and net exports will contract sharply in 2020. Public consumption expenditure and investment, in turn, will grow and dampen the decline in GDP. The acute phase of the corona crisis will pass sometime next year and the economy will gradually begin to recover, led by private consumption.

chart 4.Finland's cost-competitiveness may well weaken

Uncertainty will dampen private consumption for a long time to come

In an environment of rapidly waning employment, the wage bill will shrink in the early part of the forecast period, especially in the current year. However, higher earnings, increasing current transfers and the persistently low level of inflation will support household purchasing power. Thus, household disposable income will remain roughly at the previous year’s level in 2020 and will already grow at a fairly brisk pace in 2021 and 2022. Household real disposable income will also grow in the forecast period, at an average annual rate of slightly over 1%. In 2022, the number of persons employed will begin to rise again, lending support to growth in the wage bill and purchasing power.

The substantial weakening of the economic outlook in response to the corona pandemic is eroding consumer confidence, which in turn curbs private consumption. As business restrictions are relaxed and uncertainty abates, household consumption behaviour will gradually return towards normal. In 2020, private consumption will contract by as much as 6.4%, but will already grow by nearly 5% in 2021, after which the growth rate will moderate somewhat towards the end of the forecast period (Chart 5). Restriction measures and household fears of new infections will push up the savings rate to almost 7% in 2020. The savings rate will remain at a notably higher level than in the past few years throughout the forecast period.

The increased uncertainty will weigh on private investment, especially at the beginning of the forecast period. With muted housing market activity, residential investment will contract by more than 5% in the current year and will resume growth only in 2022. The exceptional increase in uncertainty will lead companies to withdraw or postpone fixed investments, which will decline in the current year. The forecast assumes that a medical solution to the pandemic will be found in the first half of 2021, and uncertainty will then dissipate. This will not be reflected in investment demand until 2022, however, as there is plenty of spare production capacity in the economy due to the slow pace of economic growth.

Borrowing by companies and banks on the international financial markets has become more difficult. Risk premia on loans have risen and asset values have decreased. However, the monetary stimulus provided by the ECB has supported bank lending. In Finland, companies’ financing conditions have tightened only marginally. Loan interest has not risen markedly, and access to finance has not deteriorated.

Weakness of global investment will slow recovery of Finnish exports

Demand in Finland’s export markets will decline exceptionally strongly in 2020, by about 14% (Chart 6). Uncertainty will curb the global recovery for a long time to come, but the deepest recession will be short-lived, and in 2021 Finland’s export markets will already grow by almost 9%. The recovery will be slow, however, and the export markets will not reach the 2019 level by the end of the forecast period. In 2020, exports will decline slightly more than export market demand, but will lag behind export market growth in 2021. Finnish exports largely consist of capital goods and intermediate products, meaning the weakness of global investments will weigh on Finnish exports over the next few years.

Imports will also contract sharply in 2020 in response to the fall in both domestic and foreign demand. The current account will remain in deficit in the immediate years ahead, at around 2% relative to GDP.

chart 6.The rise in pay and labour costs continues

The corona crisis will change the composition of aggregate demand markedly during the forecast period. The demand share of both private and public consumption will increase, and the shares of investments and exports will decrease compared with their GDP shares before the crisis.

Public debt will grow rapidly

The general government balance will deteriorate and public debt will grow by a record amount in a short time. This is due to the decline in tax revenues, growth in unemployment and other expenditures as well as government measures to soften the economic impacts of the coronavirus lockdown.1 In addition, there will be a further increase in risks arising from government guarantees. The general government balance will also be weakened by the expenditure increases contained in the Government Programme, which will exceed the growth in revenues.

The general government deficit-to-GDP ratio will deepen to 8% in 2020, but will gradually rebound to just under 4% in 2022, as the economy recovers. The general government debt-to-GDP ratio will rise to a good 71% in 2020. In 2022, the debt ratio will already approach 75% and will continue to grow thereafter. Both the deficit and the debt ratio will significantly exceed the limits set for them by the EU Treaty. However, due to the coronavirus crisis, the European Commission, supported by the Member States, has activated a clause that allows Member States to deviate from the regulatory limits in exceptional circumstances.

Supply and the economic cycle

The coronavirus pandemic is causing permanent losses of output for the Finnish economy. Potential growth is slowing, investment is in decline, bankruptcies are on the rise, there is a fall in the use of labour and structural unemployment is increasing. Employment is not by any means falling in the way it did during the recession of the 1990s, although the trend is worse than it was during the financial crisis.

Some job losses will be permanent

The coronavirus pandemic and the containment measures connected with it have had a rapid and dramatic effect on the labour market. The employment rate will be down by 2 percentage points over the period 2020–2021 and will only partially recover in 2022. At the end of the forecast period there will be around 65,000 fewer employed people than in 2019, and the employment rate will be roughly 71%. The unemployment rate will rise in 2021 to over 9%, and then fall slightly in 2022.

Companies have reacted to poorer sales by adjusting labour costs. Employment will fall by over 70 000 jobs in 2020. The adjustments that businesses have implemented have taken the form of a considerable number of temporary layoffs, or furloughs. The number of those on full-time furlough (as opposed to being put on short-time work) during the first few months of the crisis has risen to 160,000. The increase in unemployment has therefore remained relatively moderate for the time being.2 Some of those laid off will, however, drift into the unemployment category on account of the slow pace of the economic recovery. Job losses in some sectors could become long-term, as lower-than-normal demand will persist for quite some time and the number of bankruptcies will increase. Structural unemployment will begin to rise.

chart 7.Finland's export markets recovering slowly

A dramatic fall in employment was particularly noticeable in services during the first few months of the coronavirus pandemic. Although the worst is over in service industries, with containment measures being gradually lifted, the slowdown in the export sector predicted for the rest of the year will eventually have an adverse impact on employment in manufacturing. Economic uncertainty will mean fewer vacancies, and the weakening condition of the public finances may lead to recruitment in the general government sector being reduced in the longer term.

Finland will only partially recover from the deep recession

Finland is drifting towards recession from a position where the economy was balanced on the whole and GDP was growing close to its estimated potential.3 Because of the layoffs and redundancies due to the coronavirus pandemic and the fall in companies’ capacity utilisation, the negative output gap will widen in 2020 to around 6%, and it will remain mildly negative at the end of the forecast period. The coronavirus pandemic is a symmetric shock that is also tipping the euro area economy into deep recession: Finland’s output gap will be going much the same way as in the euro area overall during the forecast period. This will mean significant underutilisation of resources. During the financial crisis in Finland, the output gap was about the same as is now predicted.

chart 8.Employment contracts dramatically

The crisis will slow potential output growth in the years covered by the forecast. Although economic growth will pick up, after having temporarily slackened, potential output will remain lower than before. In the period 2020–2021, the decrease in investment and rise in the number of bankruptcies due to the pandemic will make any increases in the capital stock only modest and thus hamper potential output. The importance of labour input as a source of potential output will weaken, as hours worked fall and structural unemployment begins to increase. At the same time, any increase in the supply of labour will continue to be constrained by the fact that the number of people between the ages of 15 and 74 is starting to decrease. The increase in total factor productivity will remain subdued, partly on account of supply chain disruptions.

As a consequence of the coronavirus crisis, economic structures will to some extent change permanently, and there will be permanent production losses as a legacy of the pandemic. At the end of the forecast period, output will continue to be a good 1% down on 2019 levels, and around 4% below the trajectory projected before the onset of the crisis. The structural rigidities and frictions in the economy will be of great relevance to how effectively economic resources can be reallocated and how quickly potential output improves.

chart 9.Finland and euro area in deep recession

Prices, wages and costs

Consumer price increases will remain modest in the current year as weakened demand and falling crude oil prices due to the coronavirus pandemic slow inflation. The effects of the pandemic will be reflected in inflation over the forecast period, but prices will start to increase again at the end of the period as demand picks up. Nominal wages will rise by an average of 2% per annum in the period 2020–2022, but compensation per employee will fall slightly this year as a result of a temporary drop in employers’ pension insurance contributions. If the trend in unit labour costs in the euro area is as predicted, Finland’s cost-competitiveness will weaken somewhat relative to the rest of the euro area.

Rises in consumer prices remain slow

Inflation has slowed a good deal in the past few months. Whereas as recently as January the annual change in the Harmonised Index of Consumer Prices (HICP) was 1.2 %, by April inflation had slowed to −0.3%. This was the result of several factors. The sharp fall in the price of crude oil was felt in the cost of fuel and, indirectly, other commodities. The restrictions imposed on account of the coronavirus pandemic have also been reflected in consumer prices, as core inflation (HICP, excluding energy and food) stood at 0.0% in April. The pandemic will impact price trends throughout the forecast period. Furthermore, inflation expectations have clearly abated in the euro area.

With the restrictions in place, many services shut down in the spring – either that or little use was made of them – so changes have also had to be made to the way data has been collected for the consumer price index. The exceptional situation has meant that services inflation over the months to come will not necessarily fully reflect actual price pressures. In addition, the market basket has changed as a result of the restrictions, so the indices do not depict inflation as it is experienced by consumers quite so well as when things are normal.

chart 10.Inflation slows substantially in the current year

In 2020, HICP inflation will be just 0.2% (Chart 10). The fall in fuel prices will lower consumer prices substantially in the second quarter and will have an effect on prices until 2021. The uncertainty and weak demand due to the coronavirus situation will slow inflation. Core inflation will remain slow even after the restrictions are lifted as companies try to make up for fallen demand and once again try to utilise their full capacity. The prices of services will only rise by just under 1%, and those for goods (industrial products excluding energy) will actually decrease by almost 1%, so core inflation will be just 0.3% in 2020. Supply factors may, however, push up the prices of individual commodities or commodity groups. Because of production disruptions, fresh food will become more expensive in 2020, although this counts for little in the overall index.

Due to base effects, the rate of inflation will pick up slightly in the second quarter of 2021, and inflation for the year as a whole will be 0.7%. Energy prices will rise, but will generally stay somewhat lower than in 2020. Core inflation will start to normalise at the end of the forecast period as demand revives. An increase in nominal wages will bring with it rising price pressures, especially in labour-intensive services.

In 2022, inflation will accelerate to 1.3%. Energy prices will clearly contribute to this, and core inflation will accelerate to 0.9%. Despite the rise in demand, the output gap will not yet be completely closed, and price pressures will remain moderate.

Total wages and salaries dip despite rise in earnings

The increases in negotiated wages as a result of the round of collective bargaining conducted in winter and spring were in general slightly above 3% over the next two years. Wage drift is predicted to be less than average over the next few years, so nominal earnings measured by the index of wage and salary earnings will go up at the level of the economy as a whole by an average of 2.1% in the period 2020 (Chart 11). The growth in real earnings of just under 2% will slow to 0.7% in 2022, when inflation accelerates.

Compensation per employee will decrease by 0.5% in 2020, due partly to a temporary reduction in employers’ pension contributions, as well as layoffs. In 2021, compensation per employee will rise substantially, when reductions in employers’ pension contributions are no longer an issue, but the employment rate will fall compared with the previous year. The increase in nominal unit labour costs, on the other hand, will soar to almost 4% in 2020, with labour productivity declining with the sharp contraction in production. However, the rise in unit labour costs will slow during the forecast period, ending at 0.1% in 2022.

chart 11.Exceptionally high uncertainty in the forecast

The coronavirus pandemic also means that there may be changes in the way different countries manage in the area of cost-competitiveness. This is especially relevant for recovery in the wake of the crisis. If the trend in the euro area is as forecast, Finland’s cost-competitiveness will weaken overall during the forecast period, when measured according to exchange-rate adjusted unit labour costs (Chart 12). In 2020, Finland’s cost-competitiveness will improve relative to the euro area as a whole, but in 2021 it may well weaken. In 2021, unit labour costs in the euro area will embark on a downward trend, according to a forecast in June by the European Central Bank, while at the same time the prediction is that they will rise fast in Finland.

chart 12.Average interest rates on new loans have remained moderate

Risk assessment

The coronavirus pandemic is causing immense uncertainty

Economic developments in the immediate years ahead will be characterised by exceptional uncertainty as a result of the coronavirus pandemic. A sharp contraction in the global economy and the demand for Finnish exports, eroded confidence among households and businesses, and containment measures on the home front will cut Finnish economic growth dramatically in 2020. The greatest uncertainty with respect to the economic outlook relates to how the economy will recover over the next few years. Key to that recovery is how fast the pandemic can be contained and the general uncertainty dispelled.

It remains unclear just how the pandemic can be contained. The fear of new infections is hurting domestic demand, especially for services. Merely easing restrictions is still not enough to restore economic activity to previous levels. Consumers may be wary of ordering services, in particular, until a medical solution is found to deal with the spread of the virus. Furthermore, there are many risks associated with trends in the export market, as imposed restrictions and uncertainty about their continuation may result in important investment for Finland being deferred long into the future. Uncertainty is putting the brakes on household spending and companies will put off investment if demand is weak and capacity utilisation is low. Moreover, countries vary as to the virulence of the virus and the robustness and timing of the restrictions they have put in place to restrain it. So the prevailing uncertain mood in the export market will continue for quite some time.

It is enormously challenging to predict how the coronavirus pandemic and the possible prolongation of restrictions resulting from it will affect economic development. The exceptional degree of uncertainty associated with any baseline forecast can, however, be illustrated with the formulation of two alternative scenarios. What follows in Table 3 is a description of these two scenarios and the baseline forecast relating to Finnish economic development in the years to come (Table 3).

| Description of scenarios and baseline forecast | |||

|

|

Mild scenario |

Baseline forecast |

Severe scenario |

|

Assumptions on the pandemic |

The virus is contained quickly (e.g. due to advances in medical treatment or other measures). |

Containment of the virus is delayed and some containment measures must remain in place for a protracted period of time. No effective medical solution is found until a vaccine becomes available in mid-2021. |

The virus is not properly contained until a vaccine is developed in mid-2021. Significant general containment measures must be continued up to this point. |

|

Rate of economic recovery |

Rapid economic recovery begins in summer 2020. |

Economic recovery begins at a slow pace at the end of 2020. |

The economic recession is deep and the recovery remains slower than baseline. |

|

GDP in 2022 |

No significant permanent economic impact. GDP returns close to the trajectory projected before the onset of the crisis. |

Some permanent economic impact. GDP remains below the trajectory projected before the onset of the crisis. |

Significant permanent economic impact. GDP remains well below the trajectory projected before the onset of the crisis. |

|

Inflation |

Demand factors curb prices in the short term. No significant supply factors. |

Temporary slowdown in inflation. Demand factors curb prices, as supply factors remain less significant. |

Inflation slows over the longer term. Demand factors curb prices more than supply factors. |

The mild scenario describes a situation where the pandemic is contained reasonably fast globally, as a result, for example, of robust targeted action and medical advances. With the pandemic under control quickly and long-term, the fear of new outbreaks will obviously diminish substantially. It is assumed that containment measures will generally remain in place until the end of May 2020. In the mild scenario, there will be hardly any significant long term production losses.

The rate of economic recovery to normal levels, as described in the mild scenario, is rapid (Chart 13), and in 2022 GDP returns close to the trajectory projected before the coronavirus crisis. GDP falls by almost 5% in 2020, but picks up again in the shape of a healthy growth rate of 5% in 2021. In 2022, GDP growth slows to close to the long-term potential rate. Employment decreases sharply in 2020, but returns almost to 2019 levels by the end of the projection period (Chart 14). Containment measures temporarily cause the demand for services to fall, although it recovers fairly quickly almost to previous levels after restrictions are lifted. The export market suffers, but, as confidence grows, there is a fairly rapid recovery in investment activity. Weak aggregate demand only slows inflation in the short term (Table 4).

chart 13.Finland's export markets recovering slowly

The assumption in the Bank of Finland’s baseline forecast is that it will take longer to contain the virus and that some of the containment measures will have to be kept in place longer. It is assumed that a vaccine or viable treatment will be ready in mid-2021. The uncertainty is therefore more prolonged.

The speed of economic recovery in the baseline forecast is slower, and GDP falls more substantially than in the mild scenario. Nor does GDP return to 2019 levels, while the economy suffers permanent production losses with bankruptcies and decreased employment. The unemployment rate also remains elevated. GDP declines considerably in 2020, and economic recovery is fairly slow in 2021 and 2022. The caution that consumers exercise in order to avoid new infections and the prevailing uncertain mood in the export market dramatically cut economic growth in Finland. GDP at the end of the projection period is at a much lower level than was predicted before the crisis. Overall, the crisis costs around EUR 35 billion in lost production in the goods and service sectors (i.e. lost GDP) during the period 2020-2022, compared with earlier forecasts. Inflation slows down long-term as weak overall demand puts a damper on price rises.

In the severe scenario, the assumption is that the virus is not properly contained in 2020, and major community containment measures have to be extended, at least to some extent, until mid-2021. Uncertainty, therefore, also remains much greater than with the mild scenario or the baseline forecast. As with the baseline forecast, it is assumed in the severe scenario that a vaccine or viable treatment will come onto the market in mid-2021.

chart 14.Employment contracts dramatically

In the severe scenario, economic recovery is slow and there are considerably more permanent production losses in various sectors than in the baseline forecast. A substantial number of companies go bankrupt and a large part of the rise in unemployment becomes permanent. GDP falls sharply in 2020 and only starts to pick up slightly in 2021. GDP in this scenario remains around 10% lower in 2022 than the level predicted before the onset of the crisis.

In the severe scenario, uncertainty regarding new infections cuts household consumption and firms postpone investment, as demand is weak, capacity utilisation is low and there is enormous uncertainty about the future. The unfavourable investment environment globally also weakens the chances of recovery for Finnish exports. Less investment in Finland’s important export markets reduces economic growth in Finland. Weak demand means there is a slowing in the inflation rate and even temporary negative inflation in 2020.

The sharp contraction in the Finnish economy weakens the public finances considerably in all scenarios,4 including the baseline forecast. The weakest trend in public finances is contained in the severe scenario, where the permanent decline in production and employment levels is especially harsh. The increase in the government debt ratio from 2019 to 2022 varies between 10 and as much as 30%, depending on the scenario. In 2019, the debt-to-GDP ratio was just under 60%. The decline in employment and in private consumption mean a decrease in tax revenues, with a higher unemployment rate pushing up public expenditure. Furthermore, the measures that the government implements to soften the impact of the recession increase the deficit. There is a good deal of uncertainty in the years to come regarding the public finances and, especially, the scope and timing of adjustment measures.

It needs to be stressed that the uncertainty contained in the assessments stems particularly from the fact we do not know how the coronavirus pandemic will play out in the near future, both in Finland and elsewhere in the world. It is also uncertain as to what sort of structural changes the crisis will bring in the areas of, say, international trade, the division of labour and production. Also relevant is how the crisis will affect digitalisation and influence consumer behaviour. Furthermore, future economic developments will depend on the scale of fiscal and monetary policy measures to mitigate recession as a result of the pandemic, and how and when it is targeted in Finland and elsewhere around the world. Similarly, cost-competitiveness will be a crucial factor in how Finland emerges from the crisis.

The baseline forecast is the likeliest outcome for the economy. However, the mild and severe scenarios do not necessarily depict the best or weakest possible economic forecast: growth can also prove to be slower or faster than they suggest.

The longer the coronavirus crisis and the immense uncertainty that comes with it continue, the more long-term harm it will cause the economy, with more and more bankruptcies and unemployment. Furthermore, a delay in the revival of the export market would have a very adverse effect on the recovery of Finnish export industries. A long-term continuation of the crisis combined with a possible decline in competitiveness and rapidly worsening government indebtedness would exacerbate and prolong an economic recession over the years ahead.

| Forecast summary | |||||

| 2019 | 2020f | 2021f | 2022f | ||

| GDP, annual growth (%) | Mild scenario | 1.0 | –5 | 5 | 2 |

| Baseline forecast | 1.0 | –7 | 3 | 3 | |

| Severe scenario | 1.0 | –11 | 2 | 2 | |

| Employment rate (%) | Mild scenario | 72.6 | 72 | 72 | 73 |

| Baseline forecast | 72.6 | 71 | 70 | 71 | |

| Severe scenario | 72.6 | 69 | 68 | 68 | |

| Unemployment rate (%) | Mild scenario | 7.0 | 8 | 7 | 7 |

| Baseline forecast | 7.0 | 9 | 9 | 9 | |

| Severe scenario | 7.0 | 10 | 12 | 11 | |

| General government deficit, relative to GDP (%) | Mild scenario | –1.1 | –6 | –2 | –2 |

| Baseline forecast | –1.1 | –8 | –5 | –4 | |

| Severe scenario | –1.1 | –11 | –8 | –7 | |

| General government debt, relative to GDP (%) | Mild scenario | 59.4 | 68 | 66 | 67 |

| Baseline forecast | 59.4 | 71 | 73 | 75 | |

| Severe scenario | 59.4 | 78 | 85 | 90 | |

| Inflation* (%) | Mild scenario | 1.1 | 0.4 | 1.0 | 1.5 |

| Baseline forecast | 1.1 | 0.2 | 0.7 | 1.3 | |

| Severe scenario | 1.1 | –0.1 | 0.4 | 1.1 | |

| Mild scenario: the economy recovers rapidly without significant and permanent output losses. Baseline forecast: Bank of Finland June 2020 forecast trajectory. Severe scenario: the economy recovers slowly and there are significant permanent output losses. |

|||||

| * Harmonised index of Consumer Prices. f = forecast |

|||||

| Sources: Statistics Finland and Bank of Finland. | |||||

Notes

-

The forecast for the public finances takes into account, as discretionary fiscal measures, actions agreed in the Government’s first three supplementary budgets for 2020. ↑

-

The Statistics Finland Labour Force Survey defines a person who has been laid off as employed if the layoff is for a fixed period and has lasted no more than three months. Of those laid off indefinitely, an unemployed person is one who meets the criteria for unemployment, i.e. has searched, and would be available, for work. A person laid off for a fixed period can also be classified as unemployed if the absence from work has lasted for over three months and the criteria for unemployment are fulfilled. If the criteria for unemployment are not satisfied, the person is classified as being economically inactive. For the definitions used by Statistics Finland and the Ministry of Employment and the Economy, and the differences between them, see http://tilastokeskus.fi/til/tyti/tyti_2013-08-20_men_006.html. ↑

-

Potential output describes the level of GDP, when all the economic production factors are normal. ↑

-

The public finance scenarios are calculated using elasticities described in the upcoming BoF Economics Review (Jalasjoki & Kokkinen, 2020). ↑