Analysis

Russian economy and imports to contract substantially in 2015

The Russian economy has begun to contract due to the fall in the price of oil. GDP will contract by over 4% in 2015. The uncertainty will cause a decline in investment, and consumption will be cut particularly by rapid inflation. Imports will be reduced by the contracting economy, a weak rouble and declining export income. In 2016–2017, the price of oil will rise and the contraction in the economy and imports will flatten out. Forecast risks relating to investment and imports, in particular, are high.

Economy has begun to contract due to lower oil price – imports down substantially

Russian economic growth has slowed for three years in a row, due to e.g. waning growth in the available labour force, capital and productivity. In addition, a slight decline in export prices, the Ukraine crisis, sanctions, Russia’s counter-sanctions and other negative measures, with the accompanying increase in uncertainty, slowed Russian GDP growth to just over ½% in 2014. Growth was at a standstill for a part of the year. The decline in export prices steepened towards the end of the year on the back of the slide in the oil price. The impact began to show in the early months of 2015, with a slight contraction in GDP. Without transient factors, the economy would already have contracted in 2014.

As in 2013, industrial production was partly supported by strong growth in defence spending. The depreciation in the real exchange rate of the rouble since the early months of 2013 has underpinned the position of certain industrial branches relative to imports, and may also have slightly boosted exports of certain non-energy basic commodities.

The rouble’s strong depreciation led to consumer spending rushes, which kept private consumption growth at some 2%. However, wage growth slowed, as did pension growth. Inflation rocketed (to almost 17% in February) on the back of rouble depreciation and Russia’s counter-sanctions in the form of restrictions on food imports. Consequently, real household incomes contracted in annual terms for the first time since 1999. Aggregate income was underpinned by employment, which remained buoyant for the time being. Household borrowing decreased further.

Steered by the government, investment by most large state enterprises was relatively high. This was, however, insufficient to prevent total investment from falling by some 2%. The net capital outflows of the corporate sector increased, due partly to repayment of foreign debt and considerable constraints in access to foreign funding as a result of domestic uncertainties and external financial sanctions.

Export volumes declined by 2%. Exports of crude oil and gas dwindled markedly, while exports of petroleum products continued to grow at a robust pace. As the fall in export prices steepened, export income in the last months of 2014 was already well over 10% lower (in euro terms) than a year earlier. Import volumes declined by 7% in 2014 and have now been in decline for 1½ years. The decline steepened considerably towards the end of the year.

Economy contracts substantially and imports decline further, while recovery is slow

The price of oil has now dropped by about a half from the average price in 2014, and this forecast assumes an oil price in 2015 of over USD 55 a barrel, i.e. about USD 40 lower than a year earlier. The impact of this change will be profound, since energy exports account for almost a fifth of Russia’s GDP. In addition, the situation in Ukraine, sanctions, restrictive measures imposed by Russia on the economy and trade as well as the slide in the oil price have increased the uncertainties surrounding the Russian economy. The sanctions are assumed to remain unchanged for a relatively long period. Due to the sanctions and instability in Russia, access to foreign funding is expected to remain constrained. Government expenditure is forecast to decline in real terms.

According to the Bank of Finland forecast, Russian GDP will contract by over 4% in 2015 (Chart 1). The high degree of uncertainty will cause a shrinkage in private investment, while private consumption will be cut particularly by rapid inflation. Even though Russian imports have already edged down, they are estimated to fall further, by one fifth, in response to the sharp depreciation of the rouble during the last months of 2014.

In 2016–2017, global economic growth and world trade will pick up, and it is assumed the oil price will rise to around USD 65 a barrel. The Russian economy is expected to continue slightly downward, before a slow recovery in 2017. The drop in investment is expected to flatten out towards the end of the forecast period. With real household income remaining low, it will also take time for private consumption to recover. Export volumes will grow at a very subdued pace. Imports will recover after 2016.

chart 1.Russian imports depressed by decline in export income and the real exchange rate of the rouble

Consumption and investment both down

Private consumption will decrease substantially in 2015, and slightly further in 2016. Inflation, which will ease only gradually, will erode purchasing power so that real household incomes will fall substantially. The growth prospects for private sector wages are slim in a context of weak corporate profitability and downsizing pressures. Public sector wages are expected to rise only slightly, at the most, and below the inflation rate. The government is also seeking to cut the number of public sector employees. Pensions will barely keep pace with inflation, at best. Household borrowing will remain subdued, even though the debt-servicing burdens stemming from payback of short-term loans will ease gradually. As during the crisis of 2009, savings may be rather substantial. Public consumption will decline amid pressures on the central government finances.

Russian exports should benefit from a recovery in world trade but will increase only very slowly. Energy exports, in particular, which constitute over 60% of total export income, will remain relatively unchanged according to e.g. the most recent estimates by the Russian authorities. The weakness of the rouble may bolster exports of some basic goods as long as there is capacity, but companies’ willingness to make new investments is questionable considering Russia’s uncertain business environment and the possibility of new trade sanctions.

Investment will dwindle substantially this year and next. Private investment, in particular, will be depressed by a number of uncertainties relating to the ongoing tensions in East Ukraine, uncertain prospects for sanctions and the unpredictability of Russian economic and trade-related measures stemming from possible additional sanctions and recession countermeasures. Investment by state enterprises (efforts to boost them having waned among government leaders) and large projects financed by the state and state-owned banks will remain relatively small in terms of their impact. Domestic funding is already being constricted by e.g. the need to support non-financial corporations and banks in repayment of foreign debt. As the recession hits, companies will also further cut their inventories.

Imports depressed by economic contraction, the weak rouble and lower export incomes

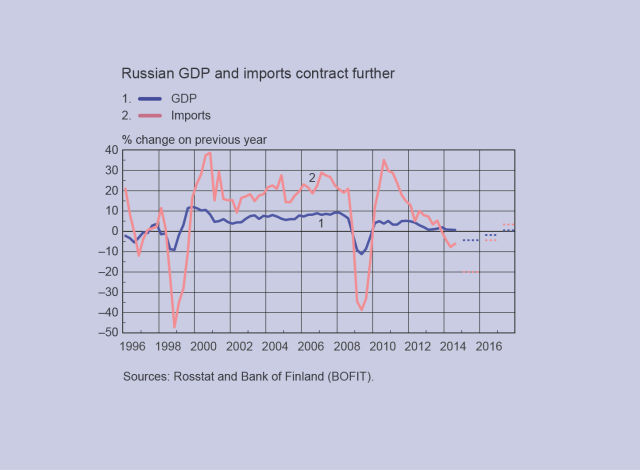

Russian imports will react strongly in 2015, partly dragged down by the economic contraction. As a comparison, import volumes declined by 30% when GDP fell by 8% during the recession of 2009. The real exchange rate of the rouble has now depreciated much more than in 2009: it is a quarter weaker than the average rate for 2014 (Chart 2). Russia’s income on exports, which dropped by a third in 2009, will deteriorate under the forecast oil price assumption, by almost a quarter in 2015. Imports will have to adjust to the smaller export income even more than usual, since it would be difficult to fund a current account deficit in the present situation. The current account last posted a deficit for a short period only, during the crisis of 1998. Against this background, import volumes are estimated to fall by a fifth in 2015.

The decline in imports will level off after 2015 as the economic contraction eases. In addition, the rouble’s real exchange rate will strengthen, since inflation is considerably faster in Russia than in its trading partners (the difference has grown to over 10%). In the absence of shocks which would lead to capital outflows, the rouble’s nominal exchange rate is expected to remain fairly stable, because net capital outflows stemming from e.g. repayment of foreign debt by non-financial corporations and banks will not necessarily exceed the surplus on the current account. The current account will be bolstered by diminishing imports and a recovery in Russia’s export income resulting from rising oil prices. The recovery in export income will, in turn, create room for an increase in imports.

chart 2.Russian GDP and imports contract further

Monetary policy tightened at same time as government seeks to cut expenditure

It has been difficult to boost economic growth through monetary policy, as corporate willingness to invest has suffered from the prevailing uncertainties. In winter 2014–2015, the monetary policy focus shifted to prevention of instability. The Bank of Russia substantially raised its key policy rate – which is, however, not quite at the level of inflation – to ease inflation and rein in capital outflows. This has driven up bank deposit and lending rates substantially, putting further strain on investment prospects.

State funding has been used for new business support measures, import substitution and to sustain economic growth. Banks have enjoyed financial support. However, falling oil prices and the looming recession have depressed the outlook for government revenues, even though the rouble weakness compensates for the loss in nominal budget revenue thanks to dollar-denominated oil taxes. In the winter, President Putin called for a reduction in federal budget expenditure in real terms in 2015‒2017 (excluding expenditure on defence and internal security). The resulting government policy targets fairly substantial cuts in real expenditure in the years ahead (also excluding pensions). Credit to projects as well as other support to be granted from the National Welfare Fund will compensate to only a relatively limited degree.

If the oil price remains, as assumed, at around USD 55 a barrel, and despite savings decisions, the federal budget deficit is set to grow so large in 2015 (to about 3.5% of GDP) that the government Reserve Fund may be eroded by as much as a half. It is possible that support measures will be implemented using government bonds (as in the bank support operations in December 2014, which amounted to 1.4% of GDP). The support operations can also draw on debtors’ bonds (as in the funding of the state-owned oil giant Rosneft, which was just under 1% of GDP). Where necessary, banks can use both instruments as collateral against even relatively long-term central bank funding. Recourse to the central bank has already become more substantial than ever before (Chart 3).

chart 3.Unprecedented recourse to the central bank

In addition to state financing, the Russian Government has increased reactive manual steering in several areas ahead of the recession. Import controls have been intensified, e.g. by raising certain import duties and favouring domestic products in public procurement and also projects of state-owned enterprises. Capital outflows have been restricted by e.g. strengthening banking controls and issuing instructions to state-owned enterprises. Companies have been encouraged to apply targeted price controls, although this has not been widely used, as yet.

The longer-term outlook is deteriorating. The foundations of growth are being eroded by the contraction in private investment. Government spending is focused increasingly on defence and pensions, while public investment is subject to the largest cuts. Efforts to counter recession via support and protective measures are serving to dampen even minimal reform efforts and undermine competition.

No shortage of forecast risks

The risks to the forecast are substantial and relate particularly to uncertainties in the Russian economy, investment and imports. Renewed fighting in East Ukraine and additional sanctions as well as Russian restrictions on the economy and trade resulting from the additional sanctions or recession countermeasures could further weaken private sector incentives to invest in the real economy. The outflow of private capital could increase despite government efforts to restrict the flows. This would lead to rouble depreciation, faster inflation and lower consumption, which would further depress imports.

The price of oil could turn out to be lower or higher than assumed. The price change would have a rapid impact on the rouble, Russian export income, imports and state revenues. The contraction we predict in private investment could, in turn, further restrict the productive capital of the economy, in which case the economy’s ability to respond to the recovery in demand could turn out to be very weak.

Bank panic situations where households and enterprises withdraw their funds from banks are possible, even though the authorities have intensified banking supervision. On the other hand, the Bank of Russia is ready to take immediate support measures.

Turning to the public finances, regional budgets, which are difficult to finance via debt, may end up on a surprisingly weak footing if receipt of key revenue items (profit tax, labour income tax and transfers from the federal budget) should fail. Economic growth in the immediate years ahead may be supported by government finances more than expected, if Russia’s leadership cannot cut federal expenditure as targeted. It is also possible they will considerably step up funding via state banks and the central bank. In the longer term, however, this would aggravate the emerging funding gridlock.