Forecast

Forecast for the Finnish Economy, June 206

Finnish economy on verge of stronger growth

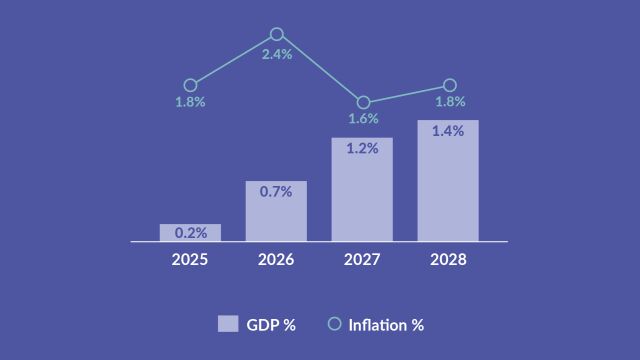

Finland’s economy is on the verge of stronger growth, but growth is being slowed by the Middle East conflict. Despite the external challenges, the economy is forecast to grow at a gradually increasing rate. This year, growth will edge up to 0.7%, and in 2027 and 2028 it will rise to 1.2% and 1.4%, respectively. The inflation rate will increase this year to 2.4%, due to higher energy prices, but it will then moderate to around 1.7% in 2027 and 2028. The unemployment rate will fall slowly. Finland’s public finances will continue to be deeply in deficit, and public borrowing will continue to rise. This forecast for the Finnish economy is based on market assumptions that the rise in energy prices will remain relatively short-lived. The forecast’s alternative scenarios examine the economic impacts of both higher and lower oil and raw material prices than in the baseline forecast.

Overview

The Finnish economy is on the verge of stronger growth. Growth picked up in the early part of 2026 as private consumption – which had long been in the doldrums – started to grow, in addition to growth in exports and business investment. Growth in the economy will gather pace, despite the difficult international environment. This year, economic growth in Finland will edge up to 0.7%, and will rise to 1.2% and 1.4% in 2027 and 2028, respectively. At the end of the forecast period, growth in Finland’s economy will be above its long-term potential as a result of cyclical factors.

The growth outlook for the global economy, however, is overshadowed by the energy crisis resulting from the Middle East conflict. Higher energy prices and rising inflation will moderate growth in the Finnish and euro area economies this year in particular. There are nevertheless a number of positive factors affecting growth in the global economy, including the diffusion of artificial intelligence (AI) and, in various major economies, an increase in incomes that will boost demand. Even so, growth in Finland’s export markets will be down from last year, and the external environment will remain difficult due to the geopolitical landscape, trade policy and Europe’s competitiveness problems. The Middle East crisis has led to a slight increase in market interest rates, which will dampen economic growth both in Finland and the euro area.

Inflation in Finland is being driven up this year by the energy crisis caused by the Middle East conflict. The rise in energy prices is being transmitted with a lag to other prices as well, but the energy price increase is expected to be temporary and the indirect effects to be moderate. As energy prices come down, the inflation rate will slow in 2027 to 1.6% from this year’s 2.4%. In 2028, inflation is projected to be 1.8%. Nominal earnings will increase by about 3.5% in both 2026 and 2027, and will then slow a little in 2028.

Private consumption began to grow at the end of 2025, and this growth will strengthen over the years of the forecast. Consumption will be underpinned by favourable earnings growth and a gradual improvement in employment, but it will also be curbed by the rise in energy prices and higher market interest rates. The savings rate will remain elevated throughout the forecast period.

Growth in private investment will be boosted in the immediate years ahead by business investment, the level of which will be linked above all to the construction of data centres and to green transition and defence industry projects. By contrast, the downturn in residential construction is likely to ease only a little, and new-build housing construction will continue to be in severe difficulty. Growth in renovation work will support residential investment, which will start to grow slowly towards the end of the forecast period, but there will be no repeat of the housing production levels seen in the peak years of 2018–2022.

The growth in exports is expected to continue at a reasonably brisk level in the immediate years ahead and to almost match the growth rate of Finland’s export markets. However, the international environment will remain challenging, and growth in export markets will be curtailed especially by the slowdown in economic growth in the euro area. Finland’s export growth will be sustained by, for example, the metal industry. Investment in AI and data centres and in defence will continue to be very active globally and will bolster Finland’s exports.

The situation in the labour market will continue to be difficult. Unemployment has risen to a markedly high level but will begin to gradually decline as the economy recovers, and more significantly in 2027. At the end of the forecast period the unemployment rate will be 9.0%. Employment will rise at a steady rate during the years of the forecast as the economy improves. The increase in the labour force participation rate is expected to slow down.

General government finances will remain significantly in deficit. The deficit as a percentage of gross domestic product (GDP) for 2026 will increase to 4.2%, particularly as a result of major defence procurements. The deficit-to-GDP ratio will rise to 4.8% in 2027 and then decline to 4.5% in 2028. Expenditure adjustment measures in central and local government will continue, but concurrent tax cuts and subdued economic growth will moderate the extent to which the budgetary position is strengthened. The general government debt-to-GDP ratio will be almost 92% at the close of 2026, and will rise to a little under 97% in 2028.

Risks are evenly balanced between the growth forecast being too low or too high. The biggest source of uncertainty in the forecast is the situation in the Persian Gulf. Uncertainty over the United States’ trade policy is continuing, and the war in Ukraine remains the greatest uncertainty regarding Europe’s security. On the other hand, economic growth may still produce a positive surprise, especially if the geopolitical situation improves quickly. In the first quarter of 2026, there was broad-based growth in the Finnish economy. The pace of economic recovery at turning points in the business cycle has often been faster than initially expected. Inflation risks are tilted slightly to the upside.

| Percentage change on the previous year | 2025 | 2026ᶠ | 2027ᶠ | 2028ᶠ |

|---|---|---|---|---|

| Gross domestic product (GDP) | 0.2 | 0.7 | 1.2 | 1.4 |

| Private consumption | -0.2 | 0.8 | 1.2 | 1.3 |

| Public consumption | -0.2 | 0.0 | -0.2 | 0.5 |

| Fixed investment | 0.8 | 6.3 | 1.5 | 2.0 |

| Private fixed investment | 0.4 | 3.3 | 2.1 | 3.3 |

| Public fixed investment | 2.4 | 17.9 | -0.4 | -2.5 |

| Exports | 3.4 | 1.7 | 2.4 | 3.1 |

| Imports | 1.7 | 3.7 | 1.8 | 3.0 |

| Effect of demand components on growth | ||||

| Domestic demand | -0.0 | 1.8 | 0.9 | 1.3 |

| Net exports | 0.7 | -0.8 | 0.3 | 0.1 |

| Changes in inventories and statistical error | -0.5 | -0.2 | -0.0 | 0.1 |

| Savings rate, households, % | 4.4 | 3.8 | 4.1 | 3.5 |

| Current account, % of GDP | 1.3 | 0.3 | 0.1 | -0.0 |

| 2025 | 2026ᶠ | 2027ᶠ | 2028ᶠ | |

|---|---|---|---|---|

| Labour market | ||||

| Number of hours worked | -1.2 | 0.2 | 0.6 | 0.7 |

| Employment rate (20–64-year-olds), % | 76.0 | 75.5 | 75.6 | 75.7 |

| Unemployment rate, % | 9.7 | 10.4 | 9.9 | 9.0 |

| Unit labour costs | 1.8 | 2.4 | 2.5 | 1.8 |

| Compensation per employee | 2.6 | 3.3 | 3.1 | 2.5 |

| Labour productivity | 0.7 | 0.9 | 0.6 | 0.7 |

| Gross domestic product (GDP), price index | 1.5 | 1.7 | 2.0 | 1.9 |

| Private consumption, price index | 1.1 | 2.4 | 1.7 | 1.9 |

| Harmonised index of consumer prices | 1.8 | 2.4 | 1.6 | 1.8 |

| Excl. energy | 2.4 | 1.7 | 2.2 | 1.8 |

| Energy | -3.8 | 9.6 | -4.0 | 2.2 |

| General government, % of GDP | ||||

| General government balance | -3.4 | -4.2 | -4.8 | -4.5 |

| General government gross debt (EDP) | 88.5 | 91.9 | 94.1 | 96.9 |

| f = forecast. | ||||

| Sources: Bank of Finland and Statistics Finland. | ||||

Operating environment: assumptions and financing conditions

The rise in energy prices is slowing growth in the global economy and driving up inflation. The outlook for Finnish exports has remained broadly unchanged, although Finland’s export markets are growing. The unpredictability of Europe’s external operating environment and higher prices of imported energy are nevertheless casting a shadow over the growth outlook. The forecast’s external assumptions are based on data available on 21 May 2026.

Global economic outlook overshadowed by rising energy prices

Energy prices have risen steeply following escalation in February of the conflict between the United States, Israel and Iran. About one fifth of world trade in oil and liquefied natural gas passes through the Strait of Hormuz, and thus closure of the Strait together with damage to the energy production infrastructure has caused global supply disruptions. The availability of refined petroleum products, such as aviation and other fuels, has also been put at risk. The impact has also fed through to the prices of other raw materials, including fertilisers, inert gases and aluminium. The sensitivity of the forecast to fluctuations in energy prices is discussed in a separate feature article (see ‘Alternative scenario on the impacts of higher energy prices on the Finnish economy’).

The crisis has pushed up energy prices, and inflation is gathering pace in all major economies, but especially in those which are big importers of raw materials. Inflation has risen in the United States and China, and businesses are reporting in surveys that price pressures are mounting amid growing production costs.1 The effects of the energy price shock will ultimately depend on how broadly based the rise in prices and wages will be. Global inflation is expected to be higher, especially for 2026, than indicated in the Bank of Finland’s March interim forecast. As well as price increases, energy imports may face supply disruptions in the present crisis.

Energy prices and the related market expectations rose markedly in the early part of the year. The price of oil is expected to be 20% higher on average this year than the market price quoted in March, and more than 50% higher compared with the beginning of the year. In the forecast assumptions based on market expectations (Table 2), the price of oil will fall gradually in 2027 and 2028. A further assumption is that raw material prices will increase much more quickly this year than previously expected. The exchange rate of the euro has remained virtually unchanged. Changes in the assumptions about raw material and energy prices and about exchange rates are reflected in the forecast as a downward revision to economic growth and an upward revision to inflation.

| Volume change year on year, % | 2025 | 2026ᶠ | 2027ᶠ | 2028ᶠ |

|---|---|---|---|---|

| Euro area gross domestic product (GDP) | 1.5 | 0.8 | 1.2 | 1.5 |

| World GDP (excl. euro area) | 3.6 | 3.0 | 3.2 | 3.3 |

| World trade (excl. euro area)1 | 5.5 | 4.2 | 3.6 | 3.5 |

| 2025 | 2026ᶠ | 2027ᶠ | 2028ᶠ | |

| Finland’s export markets, % change2 | 4.1 | 2.7 | 2.8 | 3.1 |

| Oil price, USD/barrel3 | 69.1 | 96.9 | 82.2 | 77.1 |

| Raw material prices (excl. energy), USD, % change4 | 5.8 | 3.0 | 0.8 | -1.9 |

| Export prices of Finland’s competitors, EUR, % change | -1.4 | 2.6 | 2.4 | 1.6 |

| 3-month Euribor, %3 | 2.2 | 2.4 | 2.8 | 2.7 |

| Finland’s nominal effective exchange rate5,6 | 105.6 | 106.4 | 106.3 | 106.3 |

| USD value of one euro6 | 1.1 | 1.2 | 1.2 | 1.2 |

| 1Calculated as the weighted average of imports. 2The growth in Finland’s export markets is the import growth in the countries Finland exports to, weighted by their average share of Finland’s exports. 3Technical assumption derived from market expectations. 4Technical assumption derived from market expectations. In the longer term, raw material prices are assumed in part to follow movements in global economic activity. 5Broad nominal effective exchange rate, 2020=100. The index rises as the exchange rate appreciates. 6Assuming no changes in the exchange rate. f = forecast. | ||||

| Sources: European Central Bank and Bank of Finland. | ||||

chart 1.Demand for Finnish exports will grow in the next few years

Growth in the global economy and in world trade remained robust in the early part of the year (Chart 1), with data from purchasing managers’ indices (PMI) pointing to an increase in industrial production, in particular. The increase in energy prices will, however, be negatively reflected in the economy. The rise in inflation is eroding households’ purchasing power, while production input prices for businesses are increasing and uncertainty about the future is reducing investment and consumption intentions.

The global economy is forecast to grow at an annual rate of slightly over 3% (Table 2). This year the pace of growth is assumed to remain below the path indicated in the European Central Bank’s (ECB) March projections. The latest PMI data point to a deterioration in the outlook for the service sector, in particular, whereas for the present, the manufacturing outlook remains brighter. A number of positive factors will continue to boost growth in the global economy, including a strong increase in productivity, diffusion of artificial intelligence (AI) and of the potential economic benefits to be derived from it, and higher household income. While trade barriers have increased, uncertainty over these has faded, at least for the time being, due to new trade agreements.

Finland’s export markets are growing broadly at the same pace as assumed in the March forecast. Due to the energy crisis, export prices of Finland’s competitors are rising faster than previously expected.

The outlook for Finnish exports nevertheless remains difficult, which is also the case for Europe’s external operating environment. The outlook for the economy is weakened by geopolitical unpredictability, higher trade barriers and structural competitiveness issues. Uncertainty over the availability and cost of energy is high. Europe is dependent on imported energy, and energy producer prices have been higher in Europe than in competitor countries ever since the 2022 crisis (see also ‘Productivity and energy costs are weaknesses in euro area competitiveness’).

Economic growth in the euro area has slowed in the early part of 2026, and growth may be further curbed by the rise in energy prices. The deceleration in growth is also evident in the latest survey indicators released in May. PMI data shows that the growth which was taking shape in manufacturing is coming to a standstill. Manufacturing cost pressures are building while delivery times are being extended. The outlook for the service sector has weakened, too.

According to the Eurosystem’s June 2026 macroeconomic projections, growth in the euro area economy is expected to be somewhat slower than was forecast in March (Chart 1). The slower rate of growth now forecast reflects the impact of the Middle East conflict on raw material and energy prices and real income, and on confidence in the economy. The rise in energy prices will have a downward impact on economic growth and an upward impact on inflation, this year in particular. Inflation will nevertheless slow to around 2% in the latter half of the forecast period. Factors supporting euro area economic growth will include stronger domestic demand amid ongoing steady income growth, aided by robust labour market performance. Domestic demand has also been underpinned by private and public investment. Euro area demand for Finnish exports is forecast to grow somewhat faster than assumed in the March forecast.

Interest rates will rise moderately over the forecast period according to market expectations

At its June 2026 meeting, the Governing Council of the ECB decided to raise all three key policy rates by 25 basis points. The Middle East war is creating inflationary pressures. The outlook remains uncertain and is surrounded by upside risks to inflation and downside risks to economic growth. The ECB’s Governing Council will monitor the situation carefully and follow a meeting-by-meeting and data-dependent approach to determining the monetary policy stance. The interest rate decisions of the Governing Council will be based especially on an assessment of the inflation outlook and the related risks in the light of the incoming economic and financial data, the dynamics of underlying inflation and the strength of monetary policy transmission. The Governing Council is not pre-committing to a particular rate path.

The Middle East crisis and higher energy prices have slightly pushed up market interest rates in the euro area and Finland. Short and medium-term market rates, in particular, have increased compared with the assumptions made in the March forecast. On the basis of market expectations, the 3-month Euribor will average 2.4% this year, rise to 2.8% next year and fall back to 2.7% in 2028 (Table 2). However, the risk priced in by the financial markets has remained virtually unchanged during the spring, and a broader analysis shows that the changes in financing conditions are moderate. The interest rates on new household and corporate loans granted by Finnish banks increased somewhat in April (Chart 2).

chart 2.Rise in interest rates feeding through to lending rates

According to the ECB’s most recent Bank Lending Survey (in Finnish), credit standards for corporate and household loans in Finland remained unchanged in the first quarter of 2026. Similarly, no significant changes were identified in the credit terms for corporate loans, while the demand for corporate loans was reported to have grown slightly. Demand for housing loans decreased during the survey reference period. Banks also reported that they anticipated an easing of credit standards for housing loans as mortgage margins were considered to have decreased. It should be noted, however, that the level of interest rates has increased since the survey, and this may have become reflected in credit standards. According to the Business Tendency Survey of the Confederation of Finnish Industries conducted in April, access to financing is not presenting any major constraints on output growth in any industry.

Demand and the public finances

Finland’s economy will grow moderately in the years 2026–2028. Growth will be driven especially by increases in non-residential investment and exports (Chart 3). As incomes rise, consumption will gradually pick up but will be overshadowed by rising energy prices and economic uncertainty. Defence spending, especially on the procurement of fighter jets, will increase public investment and imports. Finland’s public finances will remain deeply in deficit throughout the forecast period.

chart 3.Growth in the economy will gather pace

Consumption recovering amid crises

Private consumption returned to growth in the second half of 2025, and according to the latest statistics, this growth accelerated significantly in the first quarter of 2026.2 However, consumer confidence remains weak. Rising energy prices and uncertainty stemming from the Middle East crisis, along with domestic factors such as tight fiscal policy, could reduce households’ spending intentions in the future, too (see also ‘Household confidence and the news’). Growth in household purchasing power has slowed due to a weaker employment situation and rising energy prices. The household savings rate has stayed high and is above the long-term average (Chart 4).

chart 4.Private consumption is recovering

Despite the uncertainties, private consumption will strengthen in 2026 and will pick up somewhat in 2027–2028 (Chart 4). This growth will be supported by savings accumulated earlier, and by consistent earnings growth and a gradual improvement in the labour market. On the other hand, the consumption trajectory will be overshadowed by slower growth in purchasing power, higher energy prices, rising market interest rates, and growing uncertainty regarding both household finances and the economy.

Purchasing power will grow slightly throughout the forecast period. As the labour market strengthens, growth in households’ nominal income will increase slightly. However, in 2026, the increase in living costs due to rising energy prices will cause real income growth to stall. Additionally, the recent rise in market interest rates is passing through to lending rates, leading to higher interest payments and eroding disposable income. The savings rate is expected to stay above the usual level throughout the forecast period.

Data centres boost investment

Private investment began to increase slightly in 2025 following two years of strong contraction (Chart 5). Private investment in the coming years will be driven by growth in non-residential investment, while residential investment will continue to trail.

Non-residential investment began to grow rapidly in the first half of 2025 after two weak years. Construction of data centres has remained especially active, and green transition projects will become increasingly common in the coming years. The plans for green transition projects in the years ahead are historically large, and even if they only partially materialise, they will support strong investment growth. The defence industry is also expected to increase its investment in the immediate years ahead. Non-residential investment is projected to increase rapidly during the forecast period.

chart 5.Clear pick-up in non-residential investment

The situation for residential construction and for housing investment by households is not likely to ease much. During the forecast period, growth in renovation work will provide some support to housing investment. By contrast, new-build housing construction has faced severe difficulties, and no significant increase is expected. However, nascent growth in overall residential construction was finally observed in the latter half of 2025, although this included a large volume of state-subsidised residential construction. Sales of new dwellings remain at a standstill, and housing prices have declined further. Households’ intentions to purchase homes are at a low point, expectations are pessimistic regarding finances and the economy, and the risk of unemployment is high. The oversupply of rental dwellings is suppressing residential property investors’ interest, with no indication of an upturn in the near future. The recent rise in interest rates may also delay housing investment by households.

At present, housing construction consists to a large extent of state-subsidised projects. However, fiscal consolidation measures targeting subsidised housing production will begin to take effect in 2026, substantially slowing the growth of new-build construction. This will significantly slow the overall growth of housing investment in the coming years. Residential investment will begin growing gradually towards the end of the forecast period, although housing production will not return to the peak levels of 2018–2022.

Overall, private investment growth will rise to slightly above 3% in 2026, as business and consumer confidence in the future outlook gradually improve. Despite the prevailing uncertainty, the economy will strengthen and conditions for investment growth will improve. In the baseline forecast, the increase in energy prices is expected to be relatively short-lived. The forecast does not envisage a significant increase in inflation or production costs, either. Export growth will also generate opportunities for investment. Overall, growth in private investment will remain strong in 2027 and 2028.

Exports will grow despite challenges

Finland’s export growth exceeded 3% in 2025, driven by robust goods exports. Notably, the metal industry – particularly shipbuilding – contributed to this increase. By contrast, services exports declined slightly compared to the previous year. To date, the import tariffs imposed by the United States do not appear to have significantly affected Finnish exports. Imports grew more slowly than exports last year, due to weak domestic demand.

Despite the challenging international environment, many major exporting companies have succeeded in increasing their exports. However, regardless of the strong growth in exports, this has not yet fully matched the growth rate of Finland’s export markets (Chart 6). Finnish exports, which have centred on capital and intermediate goods, are vulnerable to international economic conditions and geopolitical uncertainties.

chart 6.Exports will grow despite challenges in the global economy

Export growth is expected to remain reasonably high in the immediate years ahead, averaging close to 2.5% during the forecast period. However, the international environment will remain challenging with high uncertainty, and growth in export markets will fall short of last year’s level, particularly as a result of slower growth in the euro area economy. Rising uncertainty will dampen investment growth in Finland’s key export markets. Nevertheless, export growth in the coming years will almost match the growth rate of the export markets. Finland’s export growth will be driven by, for example, the metal industry. Additionally, investments in artificial intelligence and data centres, along with increasing global demand for defence equipment, will further bolster Finland’s exports.

Import growth will be significantly higher for 2026. This will be attributable especially to defence-related measures like the procurement of fighter jets. Investment in data centres will also lead to increased imports during the forecast period. Furthermore, the rise in domestic demand and the gradual strengthening of the economy will lead to higher imports during the forecast period. Imports will also rise due to the imported goods and services required for producing exports. Imports will, on average, increase at a slightly faster rate than exports in the years 2026–2028.

An exceptional current account surplus emerged in 2025 as a result of a robust trade surplus (Chart 7). The value of goods exports exceeded the value of goods imports by a significant margin. However, the substantial current account surplus will diminish in 2026 as the value of imports rises significantly. The current account will be particularly weakened by defence-related procurements, data centre investments and higher energy prices. It will also be weakened, especially in the short term, by a deterioration in the terms of trade resulting from an increase in energy import prices. However, the current account will remain close to balance throughout the forecast period due to the rising value of exports.

chart 7.Current account will remain close to balance in the forecast period

Defence spending and tax cuts will slow the rebalancing of public finances

Finland’s public finances will remain significantly in deficit. The deficit as a percentage of gross domestic product (GDP) for 2026 will increase to 4.2%, particularly as a result of major defence procurements (Chart 8). In 2027, the deficit relative to GDP will increase to 4.8%, then decline slightly to reach 4.5% in 2028. Expenditure consolidation measures in central and local government will continue particularly in 2026–2027, but concurrent tax cuts and subdued economic growth will moderate the extent to which the budgetary position is strengthened. The EU has opened an excessive deficit procedure for Finland.3

Taxation of earned income will be reduced in 2026, followed by a reduction in corporate income tax in 2027. The gradual strengthening of private consumption and the impact of inflation will bolster the revenue from consumption taxes, but tax revenue will nevertheless grow more slowly than nominal GDP. The tax-to-GDP ratio will decrease by 0.7 percentage points between 2025 and 2028.

Public final consumption expenditure will increase because of rising costs and wages, despite the decline in public sector employment. Growth in social benefit expenditure and other current transfers will also be constrained due to the cuts implemented. Public investment will increase significantly in 2026 as new Air Force and Navy materiel is delivered and recorded in the National Accounts. Public investment will remain high throughout the forecast period.

chart 8.Expenditure pressures and subdued growth will mean the public deficit stays high

The central government deficit is substantial and will worsen due to defence investments. Growth in central government revenue will be constrained by tax cuts and weak economic growth. However, the central government’s on-budget entities will be strengthened through an increase in the income transfer from the State Pension Fund. Interest expenditure will rise due to higher interest rates and increased debt, and R&D funding will also contribute to the growth in government expenditure. Fiscal consolidation measures will help slow expenditure growth, but the central government’s budgetary position will not improve.

In local government too, revenue growth will be slower than expenditure growth. The financial position of the local government sector will improve slightly in the latter half of the forecast period, once the effects of the temporary cuts in central government transfers to municipalities have ended. The deficit of wellbeing services counties will remain moderate due to fiscal consolidation measures and adjustments to central government funding. However, staff costs, the rising demand for services, and investment will continue to drive local government spending pressures, causing the sector’s deficit relative to GDP to increase in 2026 and particularly in 2027.

The social security funds will remain in surplus. The strengthening budgetary position of earnings-related pension providers is based on steady growth in pension contributions and property income. However, the surplus will decrease, particularly in 2027, due to additional transfers from the State Pension Fund to the central government budget. The budgetary position of other social security funds is slightly positive and will gradually improve due to, for example, the increase made in unemployment insurance contributions. Expenditure growth in other social security funds will be restrained by social security cuts and a decline in the unemployment rate.

The general government debt-to-GDP ratio will be nearly 92% at the close of 2026, increasing to just under 97% by the close of 2028 (Chart 9). A major contributor to the increase in public debt will be the substantial negative primary balance of central and local government.4 Additionally, increasing interest payments will further add to the debt level. Growth in the economy will begin to slow the increase in the debt ratio, but this will not be enough to stabilise it. A proportion of central government expenditure will be funded by selling government assets, but this will only slow debt growth temporarily and will not change the net general government debt. Conversely, the increase in the stock of government-supported interest subsidy loans5 and the Government’s issue losses will continue to add to public debt in 2026.

chart 9.Growth in the debt ratio will not be reversed during the forecast period

Supply and cyclical conditions

The Finnish economy is starting to recover. Cyclical conditions will improve during 2026 and the upturn will strengthen in 2027. Despite this, the output gap will remain significantly negative in 2026–2027, indicating that economic resources will not be fully utilised. Unemployment is high and above its structural level, and it will not begin to decline significantly until 2027. Employment will improve steadily as cyclical conditions strengthen. By 2028, production will have reached its potential and the output gap will be close to neutral.

Unemployment rate will slowly decline as economy improves

The difficult situation in the labour market is still continuing. The unemployment rate rose to over 10% in the latter part of 2025, where it has persistently remained in the early months of 2026. By contrast, employment has weakened only slightly since its steepest decline, which was in early 2025. Weak labour demand has constrained employment growth. The number of job vacancies has remained low since the beginning of last year and no turning point has yet been reached. Due to the weak demand for labour, many unemployed jobseekers have been unable to find work. An increase in the supply of labour has also added to unemployment, as prospective employees have transitioned from outside the labour force and then been unable to find work. On the other hand, the increase in labour supply has also strengthened employment.

The unemployment rate will be higher in 2026 and 2027 than was projected in recent forecasts (Chart 10). Unemployment is forecast to be persistent and the decline in the unemployment rate is expected to be slow at the beginning of the forecast period. When a cyclical upturn occurs there is usually a lag before unemployment declines, and in this case uncertainty caused by the Iran conflict is also clouding the labour market outlook. Long-term unemployment has also continued to rise, which has led to an increase in the structural unemployment rate (Chart 11). The average unemployment rate for 2026 is expected to be 10.4%. As economic growth picks up, the unemployment rate will start to gradually decline and is forecast to fall to 9.9% in 2027. Towards the end of the forecast period, the unemployment rate will decline more rapidly, falling to 9.0% in 2028. However, even at the end of the forecast period, the unemployment rate will still be just above the level of structural unemployment (Chart 11).

Employment will start to improve as growth in the economy gathers momentum in the immediate years ahead. This will be underpinned by a recovery in the demand for labour and a strong labour supply. The employment rate is forecast to be 75.5% for 2026. This will rise steadily in subsequent years, to 75.6% in 2027 and 75.7% in 2028 (Chart 10).

chart 10.Unemployment rate will slowly decline as the economy improves

In recent years, the supply of labour has been boosted by various factors. These include longer working careers due to pension reforms, high net immigration and stricter requirements for active jobseeking as part of unemployment and social security benefits. The impact of these factors is expected to diminish in the coming years. The slowdown in labour force growth will contribute to a decline in the unemployment rate towards the end of the forecast period, as more people transition from unemployment to employment. At the same time, there will be fewer people transitioning to unemployment from outside the labour force.

chart 11.Unemployment rate will approach its structural level in 2028

Cyclical conditions improving

The Finnish economy is starting to recover. Cyclical conditions are improving this year, and the upturn will strengthen in 2027. Despite this, the output gap will remain significantly negative in 2026–2027, indicating that economic resources will continue to be underutilised.6 The unemployment gap will also remain positive, as unemployment will exceed its structural level (Chart 11). In 2028, gross domestic product (GDP) will grow at an above average pace and the output gap will be close to neutral (Chart 12).

chart 12.Cyclical conditions will improve but economic resources will continue to be underutilised

The growth in Finland’s potential output in 2026–2028 will be low, rising at an average annual rate of less than 1% (Chart 13). The growth in all production factors (capital, labour input, total factor productivity) will be subdued.

Last year, growth in potential output was particularly slow because the capital stock hardly increased at all following many years of low investment, and because there was an increase in structural unemployment. Structural unemployment has increased because high unemployment and increased long-term unemployment make it more difficult to return to the labour market (hysteresis).

Growth in capital stock will be slow in the early part of the forecast period, which will curb growth in potential output. However, corporate fixed investment is expected to strengthen as defence, technological changes and the green transition increase investment needs.7 Higher market rates have also curbed investment appetite. High uncertainty about the international operating environment will reduce risk-taking, and low utilisation rates will further reduce companies’ investment needs. Growth in the capital stock will therefore be subdued this year, but it will strengthen towards the end of the forecast period.

The crises of recent years have weakened growth in total factor productivity due to the cessation of trade with Russia, the reorganisation of supply chains and more expensive inputs.8 , 9 Higher tariffs are exacerbating the situation, as they can cause production losses due to inefficient reallocation of resources across different sectors and countries.10 ,11 Population ageing is slowing productivity growth, as the economy’s capacity for renewal weakens and resources shift to public sector services, where productivity growth is typically slower than in the private sector. Defence investment12 is not expected to boost productivity in the same way as investment in productive capacity or in education.13

The supply of labour will grow slightly in the years ahead. After a long decline, the number of working-age people started to grow in 2023–2025, due to increased immigration. According to Statistics Finland’s population projection, the working-age population will continue to grow in the future as a result of net immigration. This would support growth in potential output (Chart 13). The increase in the labour force participation rate has also supported growth in potential output, although the impact is waning. On the other hand, the supply of labour is being weakened by employees working considerably fewer hours on average than before the COVID-19 crisis, and this trend is not expected to change. The lengthening of working careers, combined with population ageing increases part-time work and improves the participation rate, but at the same time reduces the growth potential of average hours worked.14 With the improvement in the economy, structural unemployment is expected to decline slightly at the end of the forecast period, which will increase potential output.15

chart 13.Potential output will grow slowly

Prices and costs

Inflation will be up in 2026 as a result of the rise in energy prices caused by the war in Iran. The forecast assumes the rise in energy prices to be temporary, and so inflation will ease in 2027. The growth in nominal earnings will be close to 3% in each of the years 2026–2028. The Finnish economy’s cost competitiveness relative to the euro area will remain unchanged.

Energy shock will drive up inflation temporarily

Consumer price inflation has risen in Finland during the spring, due to the surge in energy prices caused by the Iran war. According to preliminary data, inflation was already at 3.0% in May, as measured by the Harmonised Index of Consumer Prices (HICP). Core inflation, which excludes energy and food prices, also increased to 2.2%.

The inflation forecast for 2026 is 2.4% (Chart 14). Based on the market assumptions underlying the forecast, consumer energy prices will rise by nearly 10% this year. However, there is considerable uncertainty surrounding the outlook, particularly regarding crude oil prices and their response to developments in the Iran war. The rise in energy prices is being transmitted with a lag to other prices as well, but these so-called indirect effects will remain moderate if the increase in energy prices is temporary. In the ‘alternative scenario’ section of the forecast, the inflation outlook is examined using two scenarios. In these scenarios, energy prices deviate from the market assumptions underlying the forecast. Core inflation will rise from its level of the first few months of this year, but will average less than 2% for 2026 as a whole.

Inflation will slow in 2027 as energy prices decline. However, core inflation and food price inflation will rise after a time lag, reflecting higher import prices. In 2028, the final year of the forecast period, inflation will rise to 1.8%. As cyclical conditions improve, price pressures will start to increase gradually, although there will still be slack in the economy as the output and unemployment gaps remain slightly open. The forecast assumes that the EU’s emissions trading system for fuel combustion in specified sectors (ETS2) will enter into force in 2028, which will push up energy prices.

chart 14.Rise in energy prices will drive up inflation temporarily

Earnings growth will remain above inflation

Collective bargaining agreements in Finland are in force in most industries until the end of 2027, which will largely determine the growth in nominal earnings this year and in 2027. Based on these agreements, negotiated wages will rise at an average annual rate of around 3% in 2026–2027. Taking into account wage drift, the level of nominal earnings – as measured by the index of wage and salary earnings – is expected to rise by about 3.5% in 2026 and 2027 (Chart 15). In 2028, growth in nominal earnings is expected to slow to below 3%, but wage growth will still remain above inflation. In the preparation of this forecast, an assumption was used that is based on a long-term observed correlation suggesting that the pace of long-term growth in real wages will be broadly the same as growth in productivity.

chart 15.Growth in nominal earnings will stay at around 3% in the immediate years ahead

Cost competitiveness can be assessed by comparing between countries the development of unit labour costs, adjusted for the terms of trade. Based on this indicator, Finland’s cost competitiveness relative to the euro area will remain unchanged during the forecast years 2026–2028 (Chart 16). According to the forecast, the cost of labour will rise at a slightly slower pace than the euro area average, which will improve cost competitiveness. Labour productivity per person employed will grow in Finland in the forecast period at almost the same pace as in the euro area.

chart 16.Finland’s cost competitiveness relative to the euro area will remain virtually unchanged in the immediate years ahead

Risk assessment

The risks surrounding the growth forecast for the Finnish economy are evenly balanced between downside and upside risks. Finland’s near-term growth outlook continues to be overshadowed by uncertainty, but growth may also provide a positive surprise if the geopolitical situation eases rapidly. Inflation risks are tilted slightly to the upside.

Forecast’s growth risks evenly balanced, inflation risks slightly to the upside

The biggest source of uncertainty in the forecast is the situation in the Persian Gulf. Despite progress achieved towards resolving the issues, the crisis may continue for longer than assumed in the baseline scenario (see the ‘alternative scenario’ section of the forecast). If the crisis is prolonged, the prices of crude oil and natural gas may rise further and availability problems may increase. The rise in energy prices will gradually spill over to other prices. A rise in euro area inflation could increase inflation expectations and lead to a larger rise in market interest rates than has been assumed.

Uncertainty about US trade policy continues and new trade restrictions, such as product-specific tariffs, are still possible. For the security situation in Europe, the largest uncertainty factor is still the future direction of the war in Ukraine.

Households and businesses may remain cautious for longer than expected. Household confidence is being undermined particularly by weak public finances. Finland’s next Government will have to decide on new tax increases and expenditure cuts. The extent and nature of these are not yet known. For private investment, the largest risks are related to the housing market. The recovery of new-build housing construction may take longer than expected.

The inflation risks to the forecast are slightly to the upside. If the Strait of Hormuz were to stay closed, the prices of oil and fertilizer components will remain high for a long time. The indirect effects of this would be reflected in food prices, in particular. Inflation may also turn out to be lower than forecast if the market price of oil declines to a level lower than assumed in the baseline scenario.

It is also possible that the Finnish economy will grow more quickly than forecast. In the first quarter of 2026, there was a fairly broad-based pick-up in economic growth. The pace of economic recovery at turning points in the business cycle has often proved to be faster than initially expected.

In manufacturing, there have been signs of an upturn in recent months. Order books have grown, and export performance has been stronger than expected. Increased investment in Europe’s infrastructure and defence will also improve the opportunities for export and investment growth in Finland. Progress with the green transition has been seen as an increase in the production of renewable energy. The low price and good availability of electricity in Finland has so far attracted mainly data centres, but this could in future also attract higher value added production.

Notes

-

In the United States, for example the Manufacturing and Services Purchasing Managers Indices released by the Institute for Supply Management (ISM) show that businesses raised prices more frequently in April-May. In China, the S&P Global purchasing managers' index for May suggests a rise in production input prices, notably in manufacturing. Nevertheless, inflation has remained moderate so far, but the increase in the producers’ price index has been stronger than before, amounting in April to 2.8% year on year. ↑

-

In the first quarter of 2025 private consumption was roughly at the same level as in 2019. Household consumption has increased in recent quarters especially regarding non-durable consumer goods. Consumption of durables has dropped to a level that is 10% below where it was in 2019. Consumption of services has remained steady since 2022. ↑

-

The Bank of Finland’s forecast does not attempt to anticipate any fiscal consolidation or growth measures that the next Government may decide. ↑

-

The primary balance is the difference between general government revenues and expenditures excluding interest payments. ↑

-

The Centre for State-Subsidised Housing Construction (Varke) provides government assistance, subsidies and guarantees for housing and construction. ↑

-

Potential output is the volume of GDP when all the inputs in the economy are in normal use. The output gap is the difference between the economy’s actual and potential GDP. When actual and potential GDP are at the same level and are growing at the same rate, the output gap will be zero and the economic cycle is said to be neutral. ↑

-

See the ECB’s article on the impacts of climate change on potential output (How climate change affects potential output, ECB Economic Bulletin, Issue 6/2023.) ↑

-

Higher and more volatile prices of energy may weaken potential output through various channels. See: e.g. Deutsche Bundesbank (2022b) Impact of permanently higher energy costs on German potential output, Monthly Report, December 2022, p.29 and the ECB’s projections(ECB Bulletin 5/2022, Box 4 ), as well as the assessments presented in the Bank of Finland Bulletin 2026 (Productivity and energy costs are weaknesses in euro area competitiveness). ↑

-

The economy has been hit by various different crises in recent years. This has led to uncertainty in the growth potential estimates for the economy. The growth potential could be affected by permanent changes in, for example, trade barriers, tariffs, globalisation, production methods, energy prices, household behaviour or immigration (see: European Commission’s Spring 2023 Economic Forecast, special issues). ↑

-

See: e.g. IMF (2020) Modelling Trade Tensions:Different Mechanism in General Equilibrium. ↑

-

According to the Chamber of Commerce’s September survey of exporting companies, more than half of the companies that responded were dissatisfied with the EU’s tariff agreement with the United States. Only one tenth of respondents were satisfied. Uncertainty has continued due to new initiatives from the United States since the agreement was made. Two thirds of companies report that the tariffs in general have a negative impact on their operations. ↑

-

For example fighter jets. ↑

-

See: e.g. Lehmus, Nelimarkka and Vilmi (Bank of Finland Bulletin 5/2025) Will higher defence spending boost euro area growth?. ↑

-

See: e.g. 'Part-time jobs in Helsinki and Finland 2023' (in Finnish) (Kaupunkitieto, 2024). ↑

-

In estimating the potential output in the forecast period, a technical assumption is made in which the participation rate is set at the average level of the previous business cycle. ↑